Third party intermediaries or energy brokers are an important source of information for companies in their energy procurement and an important sales channel for suppliers; however the market is un-regulated, lacks transparency, and may be deterring customers at a time when rising prices mean many businesses are facing rapidly growing energy costs. At the same time, the UK’s largest energy broker, Utilitywise, has recently entered administration, indicating that the problems affecting the retail energy market are not limited to challenger suppliers.

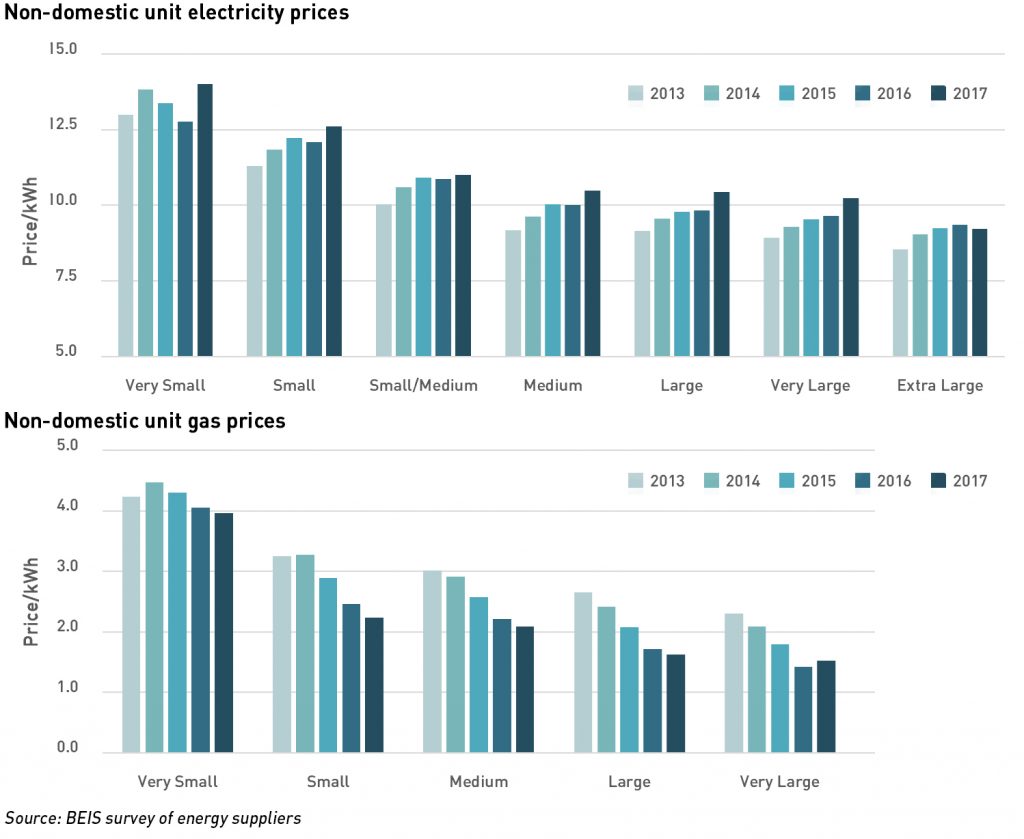

Energy costs continue to be in the news, and while most of the popular press is engaged with retail price tariffs, business users are also seeing their energy spend rise significantly, particularly as the cost of Government policy feeds through into their bills. At the sharp end are small and very small businesses whose unit energy costs are significantly higher than those faced by more energy intensive users.

Note: customer size defined in terms of annual consumption:

| Consumption (MWh) | Consumption (MWh) | |||

| Electricity Very small Small Small/Medium Medium Large Very large Extra large | 0-20 20-499 500-1,999 2,000-19,999 20,0000-69,999 70,000-150,000 >150,000 | Gas Very small Small Medium Large Very large | <278 278-2,777 2,778-277,777 27,778-277,777 277,778-1,111,112 |

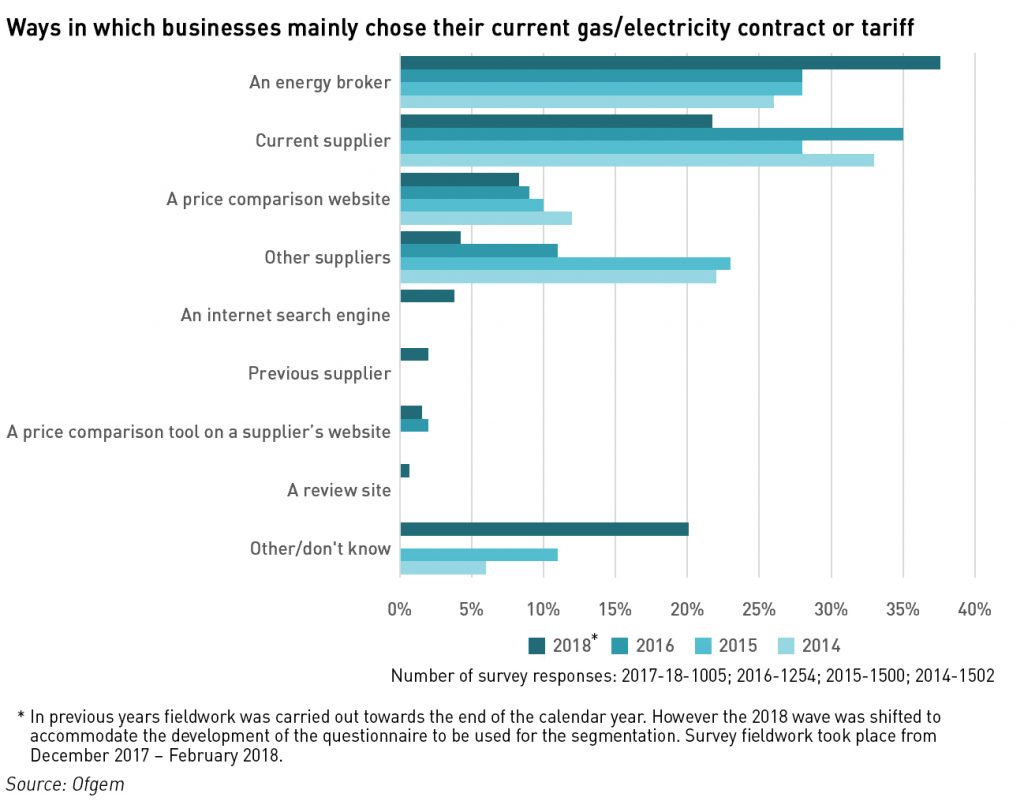

Electricity procurement can be a complex area for businesses, and one that is growing in importance as energy costs rise. Research carried out on behalf of Ofgem indicates that businesses look to suppliers and energy brokers (otherwise known as third-party intermediaries or “TPIs”) when selecting their energy tariffs.

Small businesses engagement in energy markets broadly constant despite growing costs…

In its 2016 review of the energy markets, the Competition and Markets Authority (“CMA”) found that SMEs had “limited awareness of and interest in their ability to switch energy supplier”. This appears to be borne out by the Ofgem reports, which show that roughly one in five small businesses switches supplier each year, however, if engagement is taken to include switching tariffs, the number rises to almost half, and when those that considered switching but did not actually go ahead for various reasons, then around two thirds of small businesses can be said to engage with the energy market.

In its 2016 review of the energy markets, the Competition and Markets Authority (“CMA”) found that SMEs had “limited awareness of and interest in their ability to switch energy supplier”. This appears to be borne out by the Ofgem reports, which show that roughly one in five small businesses switches supplier each year, however, if engagement is taken to include switching tariffs, the number rises to almost half, and when those that considered switching but did not actually go ahead for various reasons, then around two thirds of small businesses can be said to engage with the energy market.

Despite this, the CMA found that adverse effects on competition in the small business segment, with SMEs facing actual and perceived barriers to accessing and assessing information, due to:

(a) lack of price transparency – many microbusiness tariffs are not published, with a substantial proportion being negotiated bilaterally with the supplier;

(b) use of incentives – the existence of incentives together with the wider lack of price transparency may mean SMEs are not offered the best possible deal. The CMA was concerned that customers were not even aware of this issue, and therefore were not benchmarking their prices, for example by consulting multiple TPIs; and

(c) perceived malpractice – complaints by non-domestic customers concerning alleged TPI malpractice may have reduced the level of trust in all TPIs and discouraged engagement more generally.

The report cited a 2014 survey carried out for Ofgem that found 25% of businesses with one 1-9 employees and 37% of those with 10-49 employees used a broker as their main source of information when choosing their current energy contract. Only 11% of microbusinesses used a broker as the source of their current energy contract, in other words, many microbusinesses that used TPIs for providing information did not use them for actual procurement.

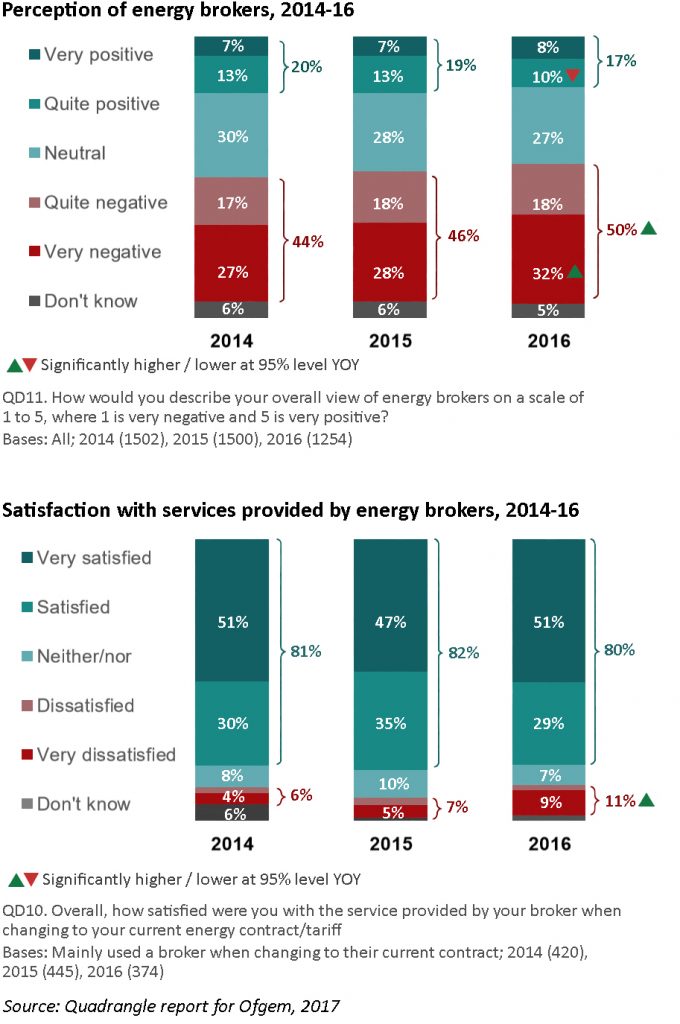

The CMA considered that low TPI penetration among microbusiness customers could be driven in part by TPIs preferring to focus on larger businesses with greater commission potential. However, it also identified apparent distrust of TPIs by small businesses as a potential factor: Ofgem’s 2014 survey found that only 20% of businesses with 1-9 employees had a positive view of energy brokers. The most recent Ofgem survey shows 50% of small businesses having negative or very negative perceptions of brokers in 2016 (versus 46% in 2015 and 44% in 2014).

The CMA cited reports of poor TPI behaviour including making misleading claims, using pressure sales techniques, and even claiming to be acting for official purposes, telling customers they had to register their meter with the TPI.

Concerns were also raised about the commission paid to TPIs which was not well-understood by non-domestic customers, and the CMA noted that TPIs may face incentives to sell certain products, or may not cover all suppliers, meaning that business customers are not offered the most appropriate available rates.

“We have received inconclusive evidence regarding alleged TPI malpractice in the supply of energy to SMEs and in particular microbusiness customers. It is therefore unclear whether this is a significant concern for microbusiness customers,”

– CMA

The CMA noted that while the Ofgem surveys which showed overall negative perceptions of TPIs among SME customers, the majority (81%) of SME customers which used brokers, were satisfied with them, and also that just 5% of SMEs that used a broker reported being charged for the its services. The CMA also cited a 2011 Cornwall Energy Report that suggested TPIs might not be presenting the best offers to SMEs because suppliers were skewing commission payments towards the deals they wanted to sell. This would suggest the root cause of alleged TPI malpractice may lie with suppliers and their incentive structures rather than the behaviour of TPIs themselves.

…however suppliers see value in selling though TPIs

A March 2018 survey by Cornwall Insight covering opinions of business energy suppliers regarding TPIs found that while suppliers strongly recognise the important role of TPIs in business supply markets – 83% of respondents put TPIs in their top two sales channels – there were areas of dis-satisfaction, particularly in relation to commissions and transparency.

The survey identified a discrepancy between what suppliers think are the most important avenues of growth (for example demand side response services and connected technology), and what TPIs can currently offer to customers. Many TPIs lack the in-house expertise to fully understand and exploit flexibility propositions, which is slowing the take up of these services.

The survey also indicated the caution with which suppliers approach the TPI sector – larger suppliers, tend to cap commissions, and impose strict credit policies and/or prescriptive guidelines. Smaller suppliers often focus on TPIs that share their ethical values. There is a recognition of the reputational risk for suppliers of working with TPIs that do not meet their standards.

TPI commissions were unsurprisingly a hot topic in the survey – no suppliers felt commissions were fair, although some did say they were representative of the market. There were numerous calls for more transparency, openness and fairness in the market.

What are TPIs and why do businesses use them?

Business energy contracts are bespoke, based on the individual needs of the customer, and often have varying price levels, carbon reduction commitments and can include penalties for exceeding set consumption levels. Comparing prices and terms is therefore complicated and makes it challenging for buyers to understand what a fair contract looks like.

For this reason, many companies use TPIs to step between them and suppliers, providing comparisons of market quotations, managing switching between suppliers, advising on consumption levels, and providing administrative services such as bill validation and renewal reminders. Ofgem estimates that there are more than 1,000 TPIs operating in the SME energy market, from large advisory firms to individual advisors.

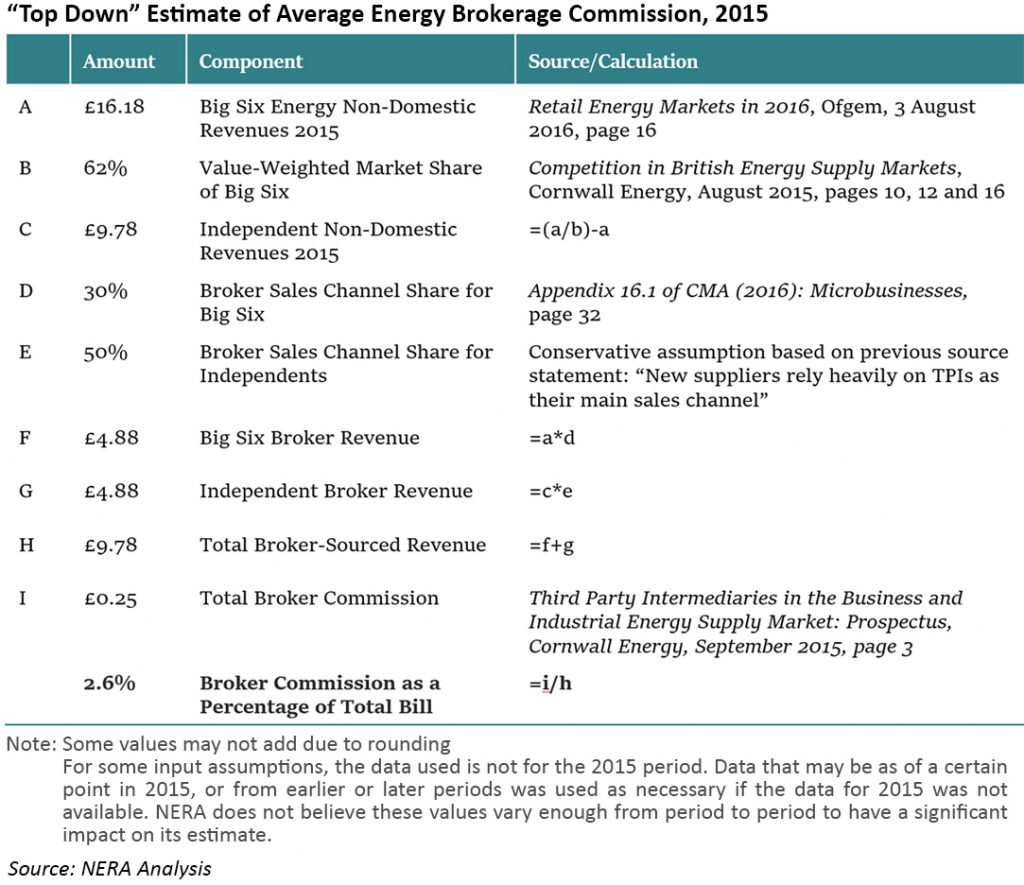

The standard charging model used by TPIs is a supplier-pays model, ie energy suppliers, rather than customers, pay commission to TPIs, usually in proportion to the amount of energy the customer uses (eg a fixed commission per kWh or a percentage of the bill). In some cases, commissions are paid upfront based on estimated consumption levels by end customers. Estimates of the size of the market vary, but some commentators have argued that the market is worth £250 million in commissions per year.

For a corporate buyer, the key benefits of using a TPI are:

- Expertise: energy contracts can be complex, long (some supplier terms & conditions can be over 50 pages long) and somewhat impenetrable to corporate buyers who are not energy experts. TPIs negotiate energy contracts on a daily basis, and have a high level of familiarity with all the contractual details, enabling them to highlight the key commercial terms such as volume tolerance, termination clauses, etc.

- Efficiency: while it is possible for companies to deal directly with suppliers, understanding alternative tariffs and terms of business can be time consuming – engaging with a TPI means that corporate buyers can focus on running their businesses, rather than having to engage with the details of energy market operation. The TPI will verify invoices, ensuring that both the meter readings and contract rate are correct, and should be the first point of contact in the event something goes wrong with the supply contract, dealing with the supplier on behalf of the customer, saving time and effort for the customer.

- Optimisation: As well as offering the right energy tariffs for their clients, TPIs can provide wider services, advising on how companies can reduce energy demand, increase energy efficiency, and reduce their carbon footprints. They can also advise on the timing of new contracts to take advantage of favourable market conditions or avoid an adverse short-term trading environment.

However, there are also drawbacks:

- Commissions: commission levels vary greatly by supplier, and there is a lack of transparency over commission levels. Not all TPIs have the same market access or buying power, adding to the variability in end prices to buyers.

- Regulation: there are currently few regulatory protections for corporate energy buyers, unlike their domestic counterparts, so customers need to perform their own due diligence on their potential TPI to ensure they are dealing with trustworthy and reliable counterparties. Many TPIs have set targets to achieve with certain suppliers which may make them more or less likely to promote different offers.

- Control: by using an intermediary when dealing with the energy supplier, companies cede a certain degree of control over their operations, and there is a risk of mis-communication between the parties.

- Hard-sell: as with many sale-based business models, companies can be on the receiving end of persistent salespeople. There are no guarantees that individual brokers won’t take their clients’ contact details with them when they move company, or sell those details to third parties. Corporate buyers can find themselves being contacted multiple times a year by various parties all trying to have a discussion about their energy procurement needs.

Getting it wrong: Utilitywise is unable to recover after re-stating its accounts due to changing revenue recognition approach

Typically, TPIs are paid commissions by energy suppliers in recognition of the customers they introduce. These commissions are generally based on the actual consumption levels of these customers, with the value being determined at the end of the contact. In some cases, suppliers make prepayments to TPIs based on assumed consumption levels – this was the case for Utilitywise, which found itself in difficulties when customers consumed less than the amounts used to determine the upfront commission payments. Individual salespeople employed by Utilitywise were paid on the same basis, creating an incentive to sign clients up to long-term contracts with high levels of assumed consumption.

This had three consequences for Utilitywise: firstly the excess payments of £4.8 million had to be refunded to the suppliers, causing a cash outflow from the business; secondly, its auditors became uncomfortable with its revenue recognition policies, since previously recognised revenues were now being repaid – this led to a change in recognition policies and a re-statement of prior year accounts; and thirdly, under the new revenue recognition policy, Utilitywise was in breach of the financial covenants of is corporate loans.

All of this took time to work through, delaying publication of the company’s 2017 accounts beyond the statutory deadline of 31 January 2018 (Utilitywise has a July year-end). Ultimately, Utilitywise was unable to recover from this, and entered administration last month.

In this context it is unsurprising that suppliers are generally negative about commissions, as noted in the Cornwall Insight research above – prepaying against demand that does not materialise is not an attractive prospect, and this significant re-statement and refund from one of the market leaders may well have implications for other TPIs.

The Utilitywise experience also suggests wider questions about the TPI model. A year ago, the company’s website, claimed that it employed “over 1,000 experts in electricity, gas and water procurement, monitoring and management”, however according to its accounts, customer growth in the year to July 2017 was only 4,000, ie 4 new customers per salesperson over the year. Revenues for the year were £67.8 million, which was broadly the same as the previous year.

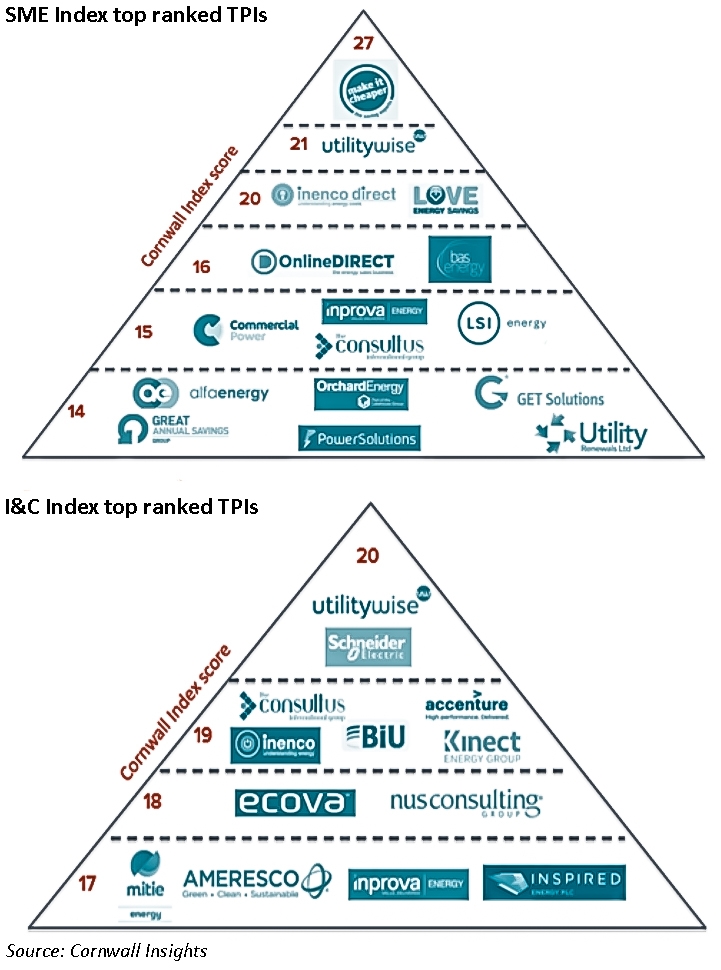

Make It Cheaper, market leader in the SME sector according to Cornwall Insight, had 118 salespeople and 175 customers in the year to 31 March 2017, generating turnover of £16.3 million, and a net profit of just under 17% of revenues. This compares with an operating loss at Utilitywise, even before taking into account over £20 million of exceptional items.

The Utilitywise collapse also highlights the downsides for suppliers to not having direct relationships with their own end customers. Although brokers do not “own” customer contracts, they have the direct relationship with a customer and broker sales staff often take those relationships with them when they move jobs. Utilitywise did not disclose its clients, but it is thought that Total Gas & Power was the most exposed supplier to the company. Total does not supply domestic customers in Britain, but is one of the largest suppliers in the non-household market, and now faces the risk that contracts secured through Utilitywise could be sold on to other suppliers after they expire.

Calls for greater regulation of energy intermediaries

From June 2017, suppliers were required to comply with the Price Transparency Remedy, which requires suppliers to disclose the prices of all their available contracts to certain micro-business customers. According to Cornwall Insight, suppliers are placing different interpretations on this licence condition, resulting in differences in the quality of information published, with information not necessarily being provided in a user-friendly format.

This may encourage businesses to use TPIs as they might feel they lack the time, knowledge and expertise to find the most suitable contract themselves – in 2016, more than a quarter of businesses (27%) believed that it was too complex or time consuming to find a new tariff or supplier.

The past 5 years have seen more than 30 mergers and acquisitions in the TPI sector – more than the average for corporate activity across the market as a whole. According to research by Cornwall Insight, there may be ten times as many energy brokers as there are suppliers, possibly due to the unregulated nature of the energy broking sector.

“The problem I have is that it is not transparent, it is unregulated and they do not have to disclose the fee to customers. So it is very difficult for customers to get an idea of value,”

– Andrew Richardson, CEO, energy benchmarking and switching platform Troocost

There have been growing calls for regulation of TPIs to protect energy users from unethical practices. According to Paul Margetts, Head of Audit and Compliance at Total Gas & Power:

“From the work we do, we see there are a lot of good TPIs who are committed to giving customers the best possible service, however, we also see a few instances of bad practice out there. We do our best to work with TPIs to try and manage that but we wouldn’t work with a TPI if we felt the risk was too high.

“However, it’s difficult for retailers to take a stand on their own and it really needs some action by Ofgem across the whole industry to ensure a consistent level of attention to customer protection and customer service. That’s the way we can make the biggest leap forward in terms of ensuring customers and retailers get the right level of service and information.”

Margetts, among others, has been calling for a code of practice for TPIs, and although Ofgem announced plans to launch their Code of Practice in 2014, it decided in 2017 not to go ahead with the Code for the non-domestic sector as there was “inconclusive evidence” of TPI malpractice concerning micro-businesses.

This lack of leadership by Ofgem has prompted a number of interested parties to issue their own Codes. The TPI Code of Practice was developed by E.On, and re-launched in 2017. Other TPI Codes are managed by The Electric Board and the Utilities Intermediaries Association. While these attempts at self-regulation are positive in some ways, energy buyers might be better served by a single, transparent code, overseen by the energy regulator.

The Utilitywise failure strengthens the arguments for more regulation, and Ofgem is reported to be preparing to launch to issue a call for evidence ahead of a strategic review of the market for microbusinesses – a move that could ultimately see the introduction of a price cap for the smallest firms.

“We will be conducting a strategic review of the microbusiness retail market to understand market challenges and consumer experience. We expect to publish an opening statement over the coming months,”

– Ofgem

Growing complexity means the need for TPIs is unlikely to go away

The energy sector is getting more complex, particularly for business consumers. Tariffs have embedded optionality, consumption caps and carbon commitments, while the market itself is evolving from a highly centralised system where consumers are largely passive, to one where consumers actively manage their usage through load shifting, and have the opportunity to install on-site generation and batteries.

Previously only large users would look at active energy management, but with the growth in domestic solar-plus-storage possibilities, come opportunities for smaller businesses to participate. Electrification of transport means business with fleets of cars or small vans may not only see electricity consumption rising further but will increasingly acquire the means to participate in demand-side-response services, earning income on their charging assets.

This may result in the roles of energy brokers and energy aggregators becoming blurred, but means the market for intermediaries in whatever form is likely to grow as businesses, particularly smaller businesses lack the internal resources to manage and optimise their energy profiles. Against this backdrop, the calls for proper regulation of the segment will only grow louder.

Leave A Comment