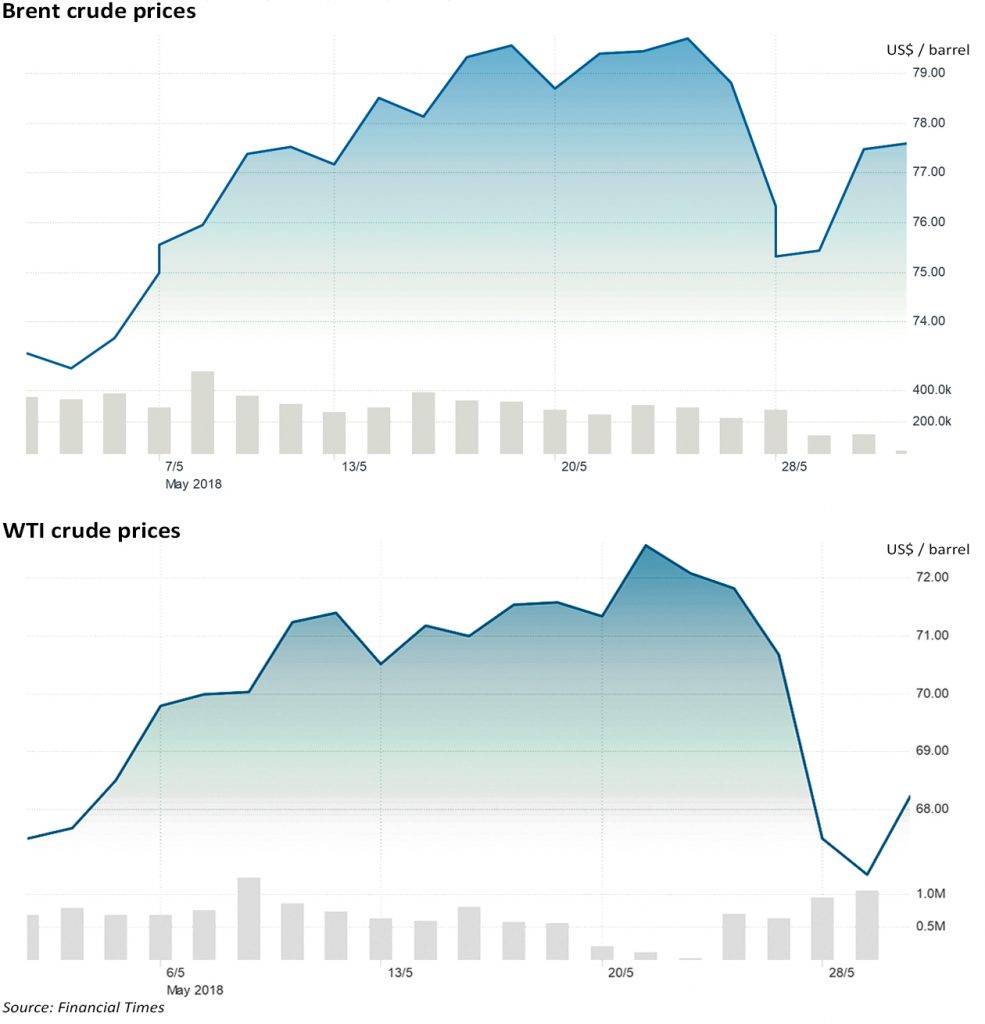

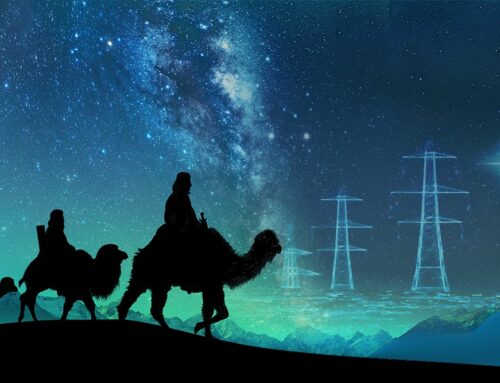

A couple of weeks ago Donald Trump announced the US was withdrawing from the nuclear deal with Iran, and I wrote that this added to the bullish trend in oil prices. Since then oil prices have fallen from their highs and a divergence is emerging between the European and US benchmarks.

As can be seen from the charts, both Brent crude and WTI fell last week following an announcement of a possible OPEC production increase, to plug the gap left by declining Venezuelan production, however Brent has since recovered some of its losses.

Saudi Arabia’s oil minister, Khalid al-Falih met privately with Russia’s oil minister, Alexander Novak, in St. Petersburg during the St. Petersburg International Economic Forum to discuss the possibility of increasing oil production. According to al-Falih, there may be an agreement to gradually bring more oil to the market from OPEC and non-OPEC countries currently participating in the OPEC/Non-OPEC production cut deal – this could be up to 1 million barrels per day and could begin in the second half of 2018. A decision may be made at OPEC’s meeting in Vienna on 22 June.

“It is the intent of all producers to ensure that the oil market remains healthy, and if that means adjusting our policy in June, we are certainly prepared to do it,”

– Khalid Al-Falih

However on Wednesday, the Russian central bank said falling oil prices would pose a risk to the country’s financial sector, which might indicate cooling support for increases in production.

“A significant factor for the Russian market remains the risk of a decline in oil prices, for instance in case of a further substantial increase in oil output by the United States,”

– Russian central bank

Investor concerns that US sanctions against Iran will cut oil supplies are affecting Brent more than WTI, which has continued to fall this week, and as a result the spread between the two main crude benchmarks is now at its widest for more than 3 years. WTI prices are being weighed down by increasing US production combined with concerns over limited refinery and outbound pipeline capacity.

US production has grown by 27% in the last two years to around 10.73 million barrels /day, driven by the dramatic development of shale oil production. Oilfield services firm Baker Hughes released data last week showing the rig count in North America had reached its highest level of the year, with the current global rig count now above the average for 2017.

However, according to Ashley Kelty, an oil and gas research analyst at Cantor Fitzgerald, the US does not have sufficient infrastructure capacity to maintain current output. West Texas pipelines, Oklahoma storage facilities and Gulf Coast export terminals all have capacity constraints that limit the ability of US production to meet global demand.

Data from the American Petroleum Institute showed that US crude inventories rose unexpectedly last week, increasing by 1 million barrels against analyst expectations of a 525,000-barrel decline, further dampening WTI prices.

What next for oil prices?

A survey of 36 economists and analysts carried out by Reuters on Thursday suggested Brent crude will stay above US$70 / barrel this year as strong demand and possible supply disruptions in Iran and Venezuela will put pressure on global inventories, despite a possible Russia/OPEC production increase. The consensus of US$71.68 / barrel is around US$4 higher than the forecast one month ago, and just above the average price so far in 2018. The survey forecast WTI prices will average US$66.47 / barrel this year, around 7% lower than the forecast for Brent.

The fundamental price drivers mentioned in my previous post remain the same, with much hinging on the next OPEC meeting, and the question of whether there will be any production increase and if so how much. The speed with which prices fell after the announcement of a possible increase in supplies seems to have sparked concerns in Russia, which may mean any increases are more modest than previously thought. However, with another 3 weeks to go before OPEC meets, there is plenty of time for the picture to change again.

Often when markets are encouraged to panic, demand soars for forward hedge volumes (marked by rising open interest in futures markets), which pushes price up. Once the hedge buying is over, there is nothing to support the price, and so it falls sharply. In some cases, hedge buyers find their positions are costing too much in margin calls, and they become forced liquidators of their positions, aggravating the fall in price. I’ve seen this kind of behaviour many times in the markets over the years. I suspect we may have these dynamics at present (although I have no intimate current knowledge – only what I see in price charts).

I saw some commentary last week about hedge funds closing out bullish long positions. There’s more in the FT today. I’d be inclined to agree with the comment about this being profit-taking rather than a shift in the fundamentals.