On Saturday the LNG carrier Maran Gas Mystras docked at National Grid’s Isle of Grain facility bringing with it the UK’s first cargo of US LNG since a small cargo that arrived at the Canvey Island terminal in 1964. This new shipment, enough to meet around half of the UK’s average daily summer demand, is of shale gas that was loaded at Cheniere’s export terminal at Sabine Pass on the US east coast.

“The delivery adds more diversity to the sources of gas we rely on. This year we have brought in shipments from Algeria, Qatar and South America too. The more sources you can draw on, the better.”

– Simon Culkin, terminal manager at Grain LNG.

The Isle of Grain is Europe’s largest LNG storage facility, and is an increasingly important source of flexibility in the UK market since the closure of Centrica’s Rough gas storage facility last month, although Grain’s eight storage tanks only have a collective capacity of 1 mcm, far smaller than the c3 bcm capacity at Rough. Gas can be discharged from Grain into the UK grid at an hour’s notice.

UK may see occasional cargoes but prices are too low to attract steady supply

So far this year, the Isle of Grain has received only six cargoes – two from Qatar, two from Algeria, and one each from Trinidad & Tobago and Algeria. The terminal also sent a reload to the Dominican Republic in February. According to Platts, the storage tanks at Grain were 42% full last week.

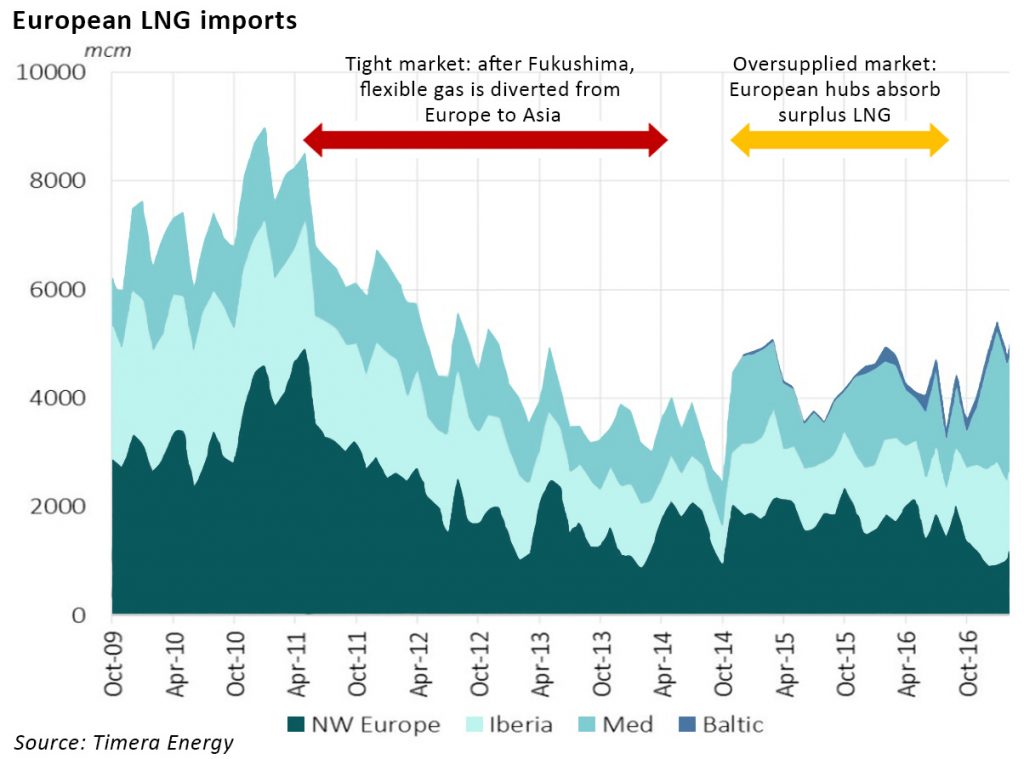

The Maran Gas Mystras, which sources said is chartered by Total, has a capacity of 159,800 cubic metres (cbm) and will be followed this week by the 162,000 cbm Adam LNG. This vessel, believed to be chartered by Trafigura, was originally bound for India via the Cape of Good Hope before changing direction on 30 June. High LNG stocks in India have reduced demand, and strong production from Algeria is currently adding to bearish pressures in the LNG market. Europe, as the only real swing market for gas globally (see the chart below), may attract a second uncommitted US LNG cargo in August.

In addition to the LNG cargoes coming to Grain, there have been other deliveries to the UK recently, and imports from Norway have also been strong, depressing prices at the NBP.

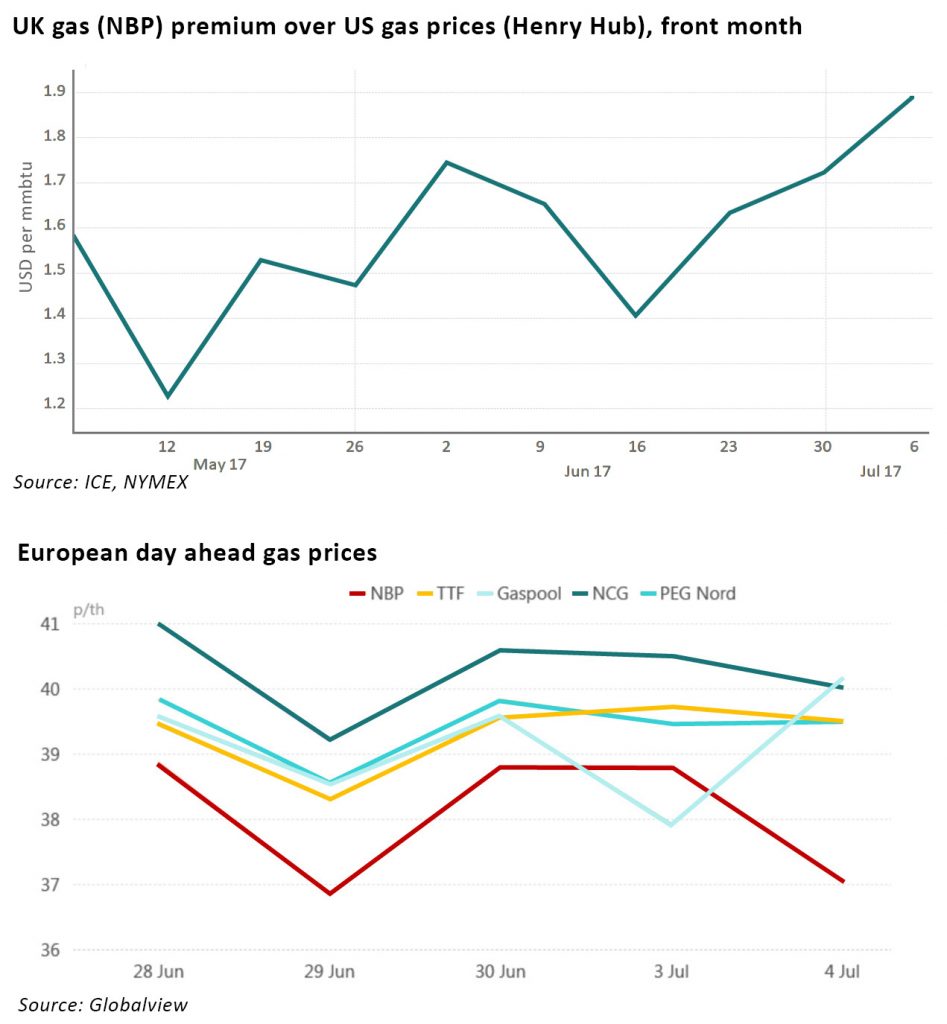

UK gas prices are currently trading at a US$1.90 premium to the US, where prices have fallen further, enabling a small margin to be made from shipping to the UK. The shorter voyage time to the UK versus Asian markets can provide some benefits at the margin.

However, in general low gas prices in the UK are unlikely to attract many cargos as with winter, Asian markets are likely to pay more to secure uncommitted cargoes. According to Ed Cox, an LNG expert at ICIS, the UK is not the destination of choice for most shippers:

“Current price signals do not suggest that Britain will be an attractive buyer of LNG this winter compared to premium markets in Asia, which do not have access to pipeline gas.”

Despite the small premium to US prices, the NBP currently trades at a significant discount to Continental prices, leading to significant exports via the interconnector with Belgium. The pipeline has seen record volumes since the beginning of July, broadly in line with its maximum export capacity of around 60 mcm per day. This trend is expected to continue over the coming weeks.

The UK market is clearly well supplied at the moment, however pressures are not expected in the summer months, and recent warm weather has depressed demand. While the arrival of US shale this week is interesting for historical reasons, it does not represent any major shift in market dynamics. Europe continues to be a sink for surplus cargoes, but Asian demand in the winter is expected to keep LNG away from the UK absent a significant rise in prices at the NBP.

Leave A Comment