The question of how electricity storage should be treated by regulators is once again in the news, with National Grid and UK Power Networks making submissions to the UK Government setting out their reasons for wanting to be able to own and operate electricity storage assets themselves. They argue that as storage can be used as an alternative to transmission and distribution, they are best placed to optimise their use in the transmission and distribution systems:

“By tapping into energy stored in grid-scale energy storage, networks could potentially reduce the need for expensive network enhancements as new technologies like electric vehicles become more widespread,”

– Suleman Alli, director of strategy at UK Power Networks.

However the move is being opposed by utilities who argue that allowing network operators to own storage would lead to market distortions and inefficiencies:

“It’s far better if regulated assets and regulated parties – the DNOs and National Grid – go out to tender, because if they go out to tender then somebody can provide a range of services with that asset and therefore it’s going to lower the marginal cost and create a level playing field,”

– Paul Massara , CEP of North Star Solar.

Current regulatory treatment of storage

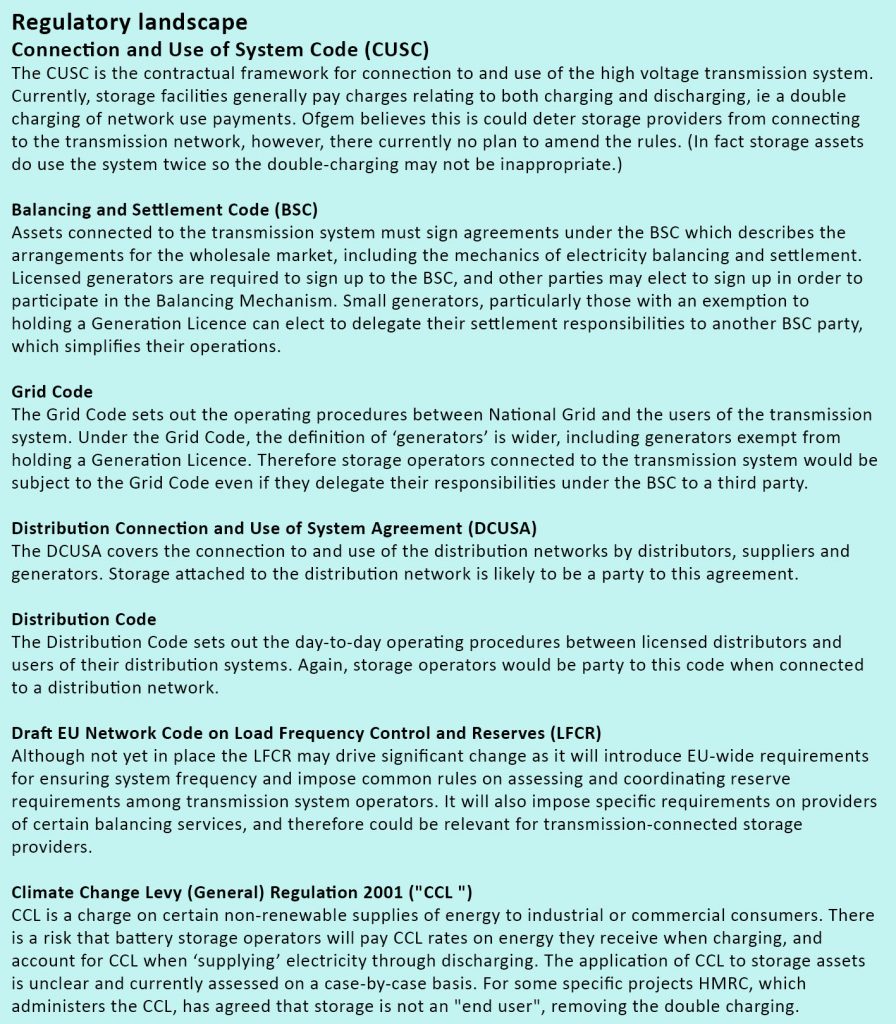

The principal legislation governing the UK electricity market, the Electricity Act 1989, makes no specific reference to electricity storage, however storage has traditionally been treated as a sub-set of generation on the basis that it can discharge or provide electricity. This means that unless an exemption applies, storage providers generally require a generation licence to operate. It also means that transmission and distribution network operators are restricted from owning storage assets. Generation licence holders are required to comply with the Grid Code, however small generators are exempt from this requirement, and most storage operators are small enough to qualify for this exemption.

Ofgem is currently consulting on different business models to facilitate electricity storage, looking at whether storage should be seem as a service where system operators contract the storage service form third party owners, or storage as an outsourced operation where network operators own the storage asset and third parties contact for management of the asset and provision of ancillary services.

This paper from law firm Bird & Bird outlines the complex set of industry codes that could govern electricity storage depending on the eventual model selected by Ofgem. (The list also serves as a reminder of the regulatory complexity of the electricity system, and the challenges faced by new entrants, particularly those with new technologies, having to navigate this complicated and often contradictory regime – see box.)

Finding the right model to optimise the potential of electricity storage

This paper by the UCL and Birmingham Energy Institutes argues that system operators are best placed to maximise the utility of storage in balancing the system, and that the deployment of storage could reduce or delay the need for network reinforcement. The authors believe that business models can be constructed that enable storage ownership by system operators without introducing anti-competitive market behaviour.

“If storage is not controlled by the system operator, it is likely that the imperfect information about electricity demands that is available to the storage owner means that they will be unable to sell storage services to fully realise the value that the storage technology could provide to the system, and this will over the long-term make storage less competitive and impede investments.”

However, other economic models such as co-location with renewable generation, could provide system benefits and there is a risk that system operators would take too narrow a view of the value of storage assets and not fully exploit their potential contributions. Although if they did seek to exploit other income streams, they would benefit unfairly from the regulated return they earn on the primary, regulated function of the asset.

Ofgem has previously argued against system operators owning storage on the basis that it could be anti-competitive, a view shared by the Policy Exchange, which points out that as network operators are monopoly businesses within their area of operation, direct ownership of storage by network operators would mean they effectively buy a network management service from themselves, rather than through any form of competitive process, with the cost passed on to consumers.

“I think if you want competitive markets to develop, you need to keep regulated monopolies out of them.”

– Andy Burgess, Ofgem.

Other commentators have pointed out that National Grid already contracts for various services that support grid stability and argue there is no fundamental difference between storage as a service and other types of gird services. Distribution System Operators could be offered similar abilities to contract for storage services without the need for direct ownership.

A challenge with the storage as a service model, however, is the inherent conflict of interest whereby system operators earn revenues from building and maintaining network infrastructure and the existence of storage threatens this by making network investments less necessary. This means system operators could lack the fundamental incentive to contract for storage services in the first place, making it difficult for storage owners to access the market, or fully exploit the economic potential of their assets.

Re-thinking regulatory structures to accommodate the evolving energy system

Earlier this year, Ofgem and BEIS decided not to require the system operation function of National Grid to fully separate to create an ISO, however stronger separation of the SO and non-SO functions was mandated. In this context, it would seem counter-intuitive to allow National Grid and DSOs to own electricity storage – to do so would effectively redefine storage as a transmission asset rather than a generation asset.

In fact neither definition reflects the full potential of electricity storage in providing capacity and flexibility to the system. To maximise this potential, the Electricity Act should be amended to create a more bespoke and appropriate definition for storage assets, but taking care not to impose in-necessary regulatory obligations.

In fact neither definition reflects the full potential of electricity storage in providing capacity and flexibility to the system. To maximise this potential, the Electricity Act should be amended to create a more bespoke and appropriate definition for storage assets, but taking care not to impose in-necessary regulatory obligations.

In-reasonable double-charging should be removed, however, storage assets should not be exempted from double-charging for use of transmission and distribution systems since they do indeed use these systems twice when charging and discharging.

Finally, care needs to be taken to ensure that system operators make full use of storage as an alternative to network expansion or reinforcement investments. This could be solved by separating system operation from system ownership – the SO could issue tenders for the required network capacity, and select the most cost-effective solution across storage or transmission infrastructure.

Perhaps an the decision on an independent system operator needs to be revisited after all.

Of course, if we didn’t have any expensive intermittent renewable energy on the grid, we wouldn’t need to add even more expensive storage.