The question of electricity market competitiveness is never far away, particularly when any of the Big 6 suppliers raise their prices. The level of concern about potential anti-competitive behaviour by the big suppliers who dominate the GB market prompted an investigation by the Competition and Markets Authority, which reported in June last year.

The headline findings of the CMA were that in general the Big 6 do not behave in an anti-competitive way, although issues were identified among customer groups defined as being “inactive” and those on prepayment meters. (It should be noted that some commentators disagree with these conclusions believing that intense lobbying from the Big 6 caused the CMA to water down its conclusions.)

CMA finds poor transparency in financial reporting undermines competition

Less well reported were other findings of the CMA around the overall market structure creating barriers to competition. In my recent posts I have been looking at retail billing and the costs that drive electricity bills. I was interested to discover that the CMA had addressed this question specifically in their report and found that lack of transparency in financial reporting was undermining trust and potentially undermining regulatory decision-making. In particular:

“…the impact of government and regulatory policies over energy prices and bills has not been effectively communicated…”

I believe the CMA comments in this regard are relevant and have copied the relevant section below, since the CMA report itself is long.

Recovering costs of government policy through bills undermines competition

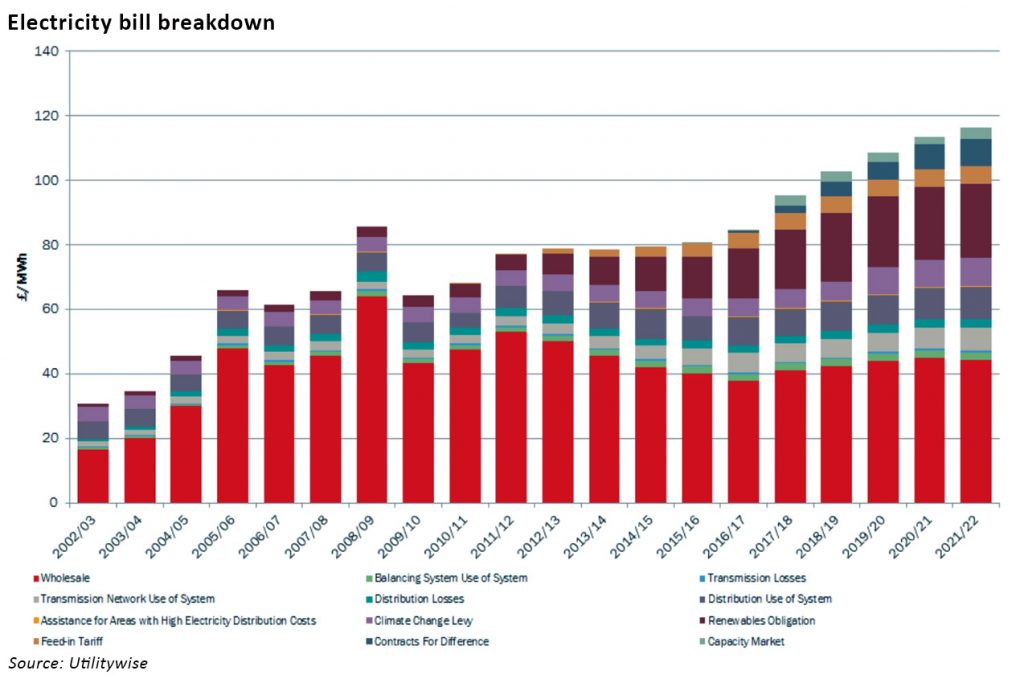

It is widely claimed that the costs associated with environmental and social costs are growing and set to grow further in coming years as the costs of EMR and smart metering begin to impact customer bills. Decarbonisation policies are also leading to increases in transmission costs as the electricity network needs to be substantially re-engineered to meet the challenges of renewable and distributed generation.

As a result, the proportion of their costs that suppliers are able to control directly is falling. This will eventually have a significant anti-competitive effect as the benefits of switching to another supplier will become ever smaller.

Ofgem requires the Big 6 suppliers to produce Consolidated Segmental Statements to provide the markets with information about their costs and profits. Ofgem also publishes a Supplier Cost Index, developed in response to the CMA’s findings, to provide some illustration of the costs faced by suppliers and their evolution, however, as noted in my previous posts, it is very difficult to draw meaningful conclusions due to the limited granularity of the data. It would be helpful if Ofgem were to publish the underlying data used in calculating the index, as well as the methodology.

Much of the focus on this reporting relates to the extent to which the vertical integration of the big suppliers allows them to distort their reported profits through obscure transfer pricing between generation and supply business units, and the significant contribution of operating costs on bills.

The inclusion of policy-related costs, should not divert attention from these questions to the extent that policy-related costs remain a small component of overall costs, but when those costs start to form a material part of the overall expenditure, the picture becomes increasingly complex and removes incentives both for the regulator to investigate questions around transfer pricing, and on suppliers to seek efficiency gains.

Alternative approaches: recover the costs of policy through general taxation

An alternative to recovering the costs of government policy relating to decarbonisation, smart meters, energy efficiency and other measures would be to increase general taxation. This approach has the benefit of removing a significant distorting factor from electricity bills, but has the drawback that it does not incentivise reduced consumption.

Although overall electricity consumption has been increasing in recent years, domestic consumption has been falling, and there is evidence of increased use of efficiency measures, with over 80% of homes now having double glazing, 75% of homes with wall cavities having cavity insulation, and 98% of homes having loft insulation. This suggests that further gains may be difficult to achieve as the low-hanging fruit has largely been picked.

Ultimately the government needs to choose whether to prioritise having a genuinely competitive electricity market and find other means of incentivising reduced consumption, or whether it will stick with the current system which threatens to make competition obsolete as policy-related costs begin to dominate bills.

Either way, far more transparency is needed so that consumers and taxpayers can understand the composition of electricity bills and for regulators to tackle genuinely anti-competitive practices in the industry where they occur.

Framework for financial reporting

|

|---|

Leave A Comment