In my previous post I looked at Ofgem’s network charging reforms. Here I will summarise the conclusion of the Significant Code Review into network access (now known as the “Access SCR”), which was originally part of a wider review into network access and forward-looking charges. In May, Ofgem published its final decision on two areas of the original SCR scope: (i) the distribution connection charging boundary and (ii) the definition and choice of access rights. The original SCR also included a review of forward-looking distribution use of system (“DUoS”) charges and transmission network use of system charges (“TNUoS”), which are now being developed outside of the Access SCR, as outlined in my previous blog.

In respect of the distribution connection charging boundary, Ofgem has decided to:

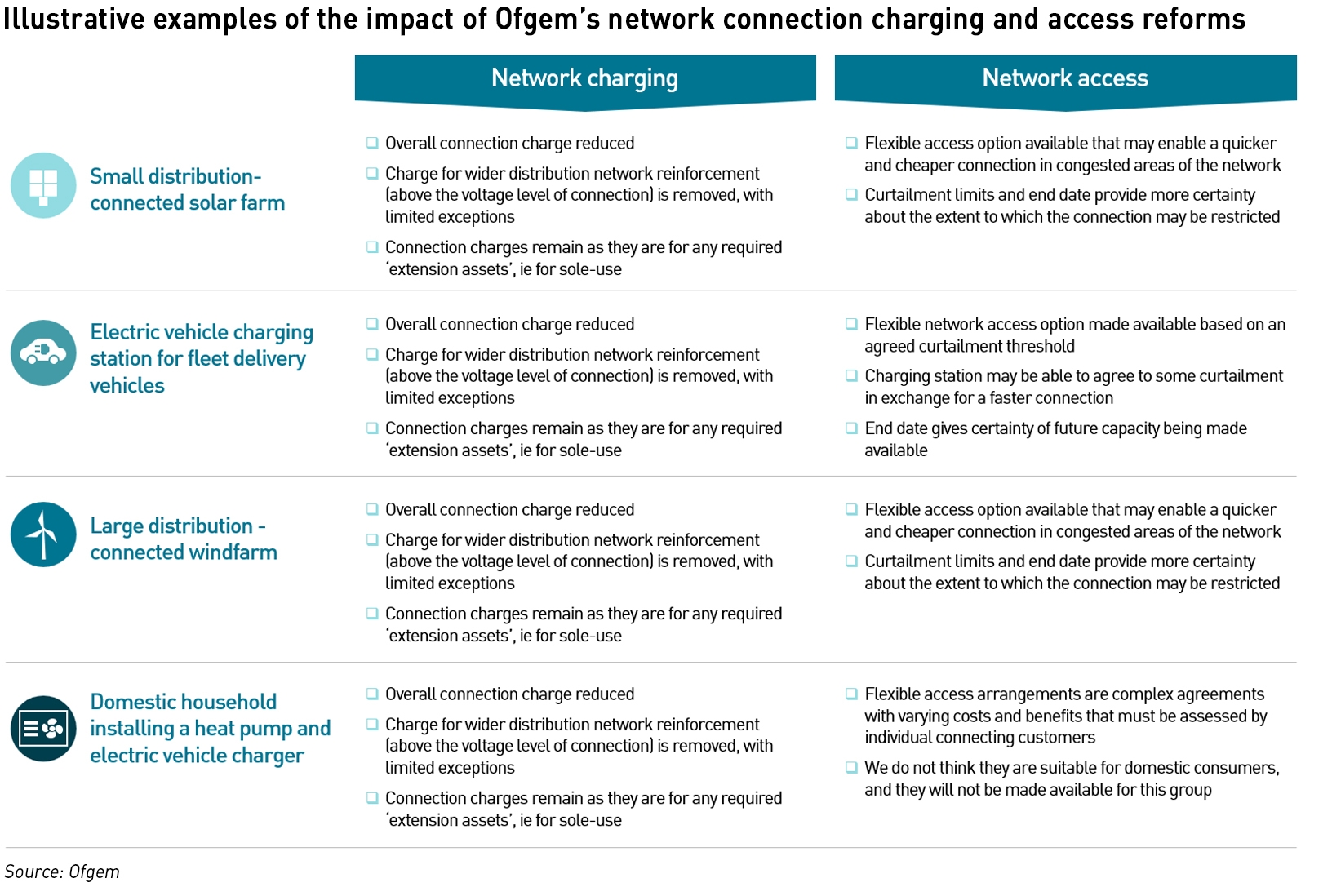

- Reduce the overall connection charge faced by those connecting to the distribution network. This includes removing the contribution to wider network reinforcement for demand connections, and reducing the contribution to wider network reinforcement for generation connections.

- Retain and strengthen existing protections for bill payers to ensure they are protected from cost increases associated with the most expensive types of connections. In these instances, the connecting customer will continue to be required to contribute more to the costs of reinforcement.

Regarding the definition and choice of access rights, Ofgem has decided to:

- Ensure a standardised non-firm access option is available for larger network users.

- Introduce clear curtailment limits and end dates for non-firm access arrangements.

Ofgem believes these measures will reduce barriers to network access, enabling users to make efficient choices about where to locate on the network and how to use their connections, whilst also supporting the continued transition to net zero at least cost. These changes are intended to take effect from 1 April 2023, in line with the start of RIIO-ED2.

Connection boundary to become more “shallow”

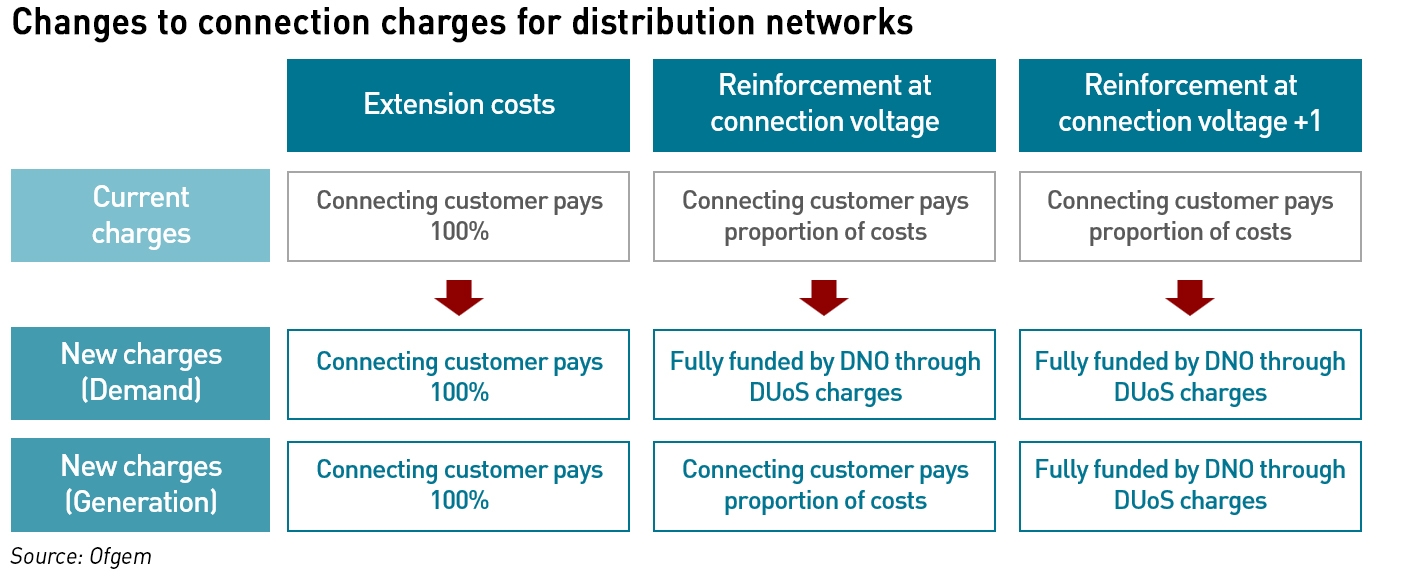

When a user applies to connect to a distribution network, the relevant Distribution Network Operator (“DNO”) will consider what work is needed to enable the connection. This might require the installation of new assets to extend the existing network to the new user (“extension assets”) and/or an upgrade or expansion of the capacity of existing shared network assets (“reinforcement”). The costs of reinforcement are split between the connecting customer (through an upfront connection charge) and the wider consumer base through DUoS charges, with the way in which these costs are split being described in terms of the “depth” of the connection charging boundary.

Under current arrangements, connecting customers face a “shallow-ish” connection boundary, which means the new user pays all of the costs for extension assets and contributes towards the cost of reinforcement, up to one voltage level above their point of connection. Any remaining costs of reinforcement are paid by the DNO’s wider customer base. Connecting customers may receive a locational signal encouraging them to connect where there is spare network capacity.

Ofgem felt these arrangements were unsatisfactory for the following reasons:

Ineffective signals and ‘free rider’ effect: there is no consistent or fair signal to all users of the network, for example the cost signal for network reinforcement only exists for the specific customer whose connection triggers that reinforcement, making them liable for the collective impact of previous connections. As reinforcements typically create a step-change increase in local network capacity, there is an incentive to ‘free ride’, where prospective new customers decide to wait until reinforcement has been triggered by another customer before requesting a connection.

Incremental reinforcement: current arrangements encourage DNOs to take an incremental and reactive approach to reinforcement rather than investing in anticipation of wider network needs, because much of the funding for connection-led reinforcement is recovered through upfront connection charges. The risk of not fully recovering these costs gives DNOs a strong incentive to wait until connection requests are received, rather than acting in advance.

Barrier to net zero: in the context of rapid de-carbonisation, Ofgem is concerned that the current reinforcement cost signals may be too strong for some users and risks creating barriers to investment. One respondent to a previous consultation described current arrangements as a “location lottery” based on connection site availability, arguing that a more strategic approach to reinforcement was required to unlock capacity required to enable investment for net zero

Boundary distortions between transmission and distribution: differences between connection charging arrangements for distribution networks and the transmission system may be creating distortions and/or impacting competition between generators connecting to the different networks. Ofgem would like to align the connection charging arrangements as far as possible to address these issues.

Ofgem has decided to remove the contribution to reinforcement for demand connections so they only pay for extension assets, and reduce the amount paid by generation connections towards reinforcement costs so they pay for extension assets and make a contribution towards reinforcement at the voltage level of the new connection. Storage assets will be treated as generation for the purposes of connection charging. Existing protections for bill payers will be strengthened to ensure they are better protected from the cost increases associated with the most expensive connections. Any reinforcement to Grid Supply Points at the connection to the transmission system will continue to be charged to the connecting customer through the upfront connection charge – there is no change to this arrangement.

Ofgem is of the view that in the absence of DUoS reform, removing all contributions to reinforcement from generation connections would mean generators would not face any price signals about the impact they have on network costs, because at present, generators receive mainly DUoS credits, even in areas where they are driving costs. Ofgem also believes that generation has a greater choice of location than demand and can choose to connect at places where the cost impact would be lower.

While it may seem counter-intuitive to transfer the costs of new connections from the connecting entity to all network users, this needs to be viewed in the context of the energy transition which will see many more network connections such as low carbon generation, and those required for the electrification of heating and transport. Since current arrangements do not allocate reinforcement costs in a reasonable way, and it would be difficult to devise a charging regime that avoided the free-rider effects described above, this does in fact make sense.

Part of the cost impact will be mitigated by introducing a “high cost cap” for expensive demand connections to mirror existing arrangements for generators. This measure means that where the reinforcement costs triggered by an individual connection are very high, these costs are met in full by the connecting customer, above the level of the cap which is currently set at £200 /kW. The new demand cap will be set at £1,720 /kVA.

A standardised approach to interruptible access rights

Network access rights define the way in which users connect to the network, the import and export capacity available to them and for how long, and whether their access can be curtailed. This is typically defined in the user’s connection agreement. Traditionally, users of distribution networks have had few options when it comes to access rights with most having standard connection arrangements where the access is “firm”, ie not subject to curtailments.

More recently, DNOs have been offering flexible connections as an alternative to paying and/or waiting for the network reinforcement that may be required for a standard connection. In exchange for quicker/cheaper access, users with flexible connections have non-firm or curtailable access to the distribution network, but there is no standard definition of curtailment or commonly defined limit on the extent to which access can be curtailed.

Ofgem is of the view that standardisation would reduce the risks faced by network users and increase interest in interruptible access rights leading to more efficient use of existing network capacity. It has therefore decided to introduce the following reforms to distribution network access rights:

- Non-firm (curtailable) access arrangements: non-firm arrangements will be available to users where there is a requirement for reinforcement and a specific network need for curtailment to manage local network constraints. Small users will not have access to these arrangements. Curtailment will be defined in terms of customer outcomes such as a time or energy limit or combination of the two.

- Curtailment limits for non-firm connections: the distribution network operator will set curtailment limits and included these in the connection offer to the connecting customer, who will have to abide by those limits. If the network operator needs to curtail above this limit, then they must procure this service from the market.

- End dates for non-firm arrangements: non-firm arrangements will have explicit end dates, after which the connection will need to be made firm or non-curtailable. Exceptions apply where the customer has not requested a firm connection or if the high cost cap is triggered and the customer does not want to contribute to reinforcement costs above the cap.

Non-firm connections should only be offered where there is an actual benefit to the network. Where a user has an interruptible agreement, but a greater level of curtailment is required than allowed in the agreement, the DNO must procure this additional amount from the market, although there will be a cap in the price that users can charge for this additional curtailment.

If a customer’s supply is interrupted under the definition of a customer interruption, that interruption will continue to be covered under the Guaranteed Standards of Performance and should not be treated as curtailment. Similarly, curtailment as a result of constraints on the transmission system will not be treated as curtailment on the distribution network as transmission constraints are outside the control of the DNOs.

Implications for network operators

Ofgem believes these changes will encourage network operators to take a more strategic approach to network planning and reinforcement, including investing ahead of need where it is efficient to do so, and considering alternatives to reinforcement to meet the capacity needs of customers. However, this issue of anticipatory investments is fraught with difficulty – following the perception that RIIO-1 was too generous to network operators, Ofgem has tightened up the price controls for RIIO-2 and significantly reduced the incentives component of the scheme. The result is that the RIIO-2 far more prescriptive than RIIO-1 which would limit the scope for anticipatory investments.

To mitigate this risk, Ofgem will allow various re-openers known as uncertainty mechanisms, which are intended to allow DNOs to secure adjustments to their price controls in response to market developments during the life of RIIO-2, but there are risks that the hurdles will be too high and/or Ofgem’s processes too slow to make these effective. The latter is a genuine concern given Ofgem’s increasingly wide remit and generally slow response times.

Ofgem intends to publish further information on its uncertainty mechanisms for dealing with load related expenditure in June as part of its Draft Determinations for RIIO-ED2.

.

With these changes, the cost of connecting to distribution networks will be reduced, with a wider range of connection options being available which will enable users to reduce costs further in exchange for reduced levels of access, while allowing DNOs to use existing infrastructure more flexibly. While this will increase DUoS costs paid by all network users including households, all of these costs typically feed through to end users one way or another anyway, so if the changes reduce the overall cost of building and operating the networks, they will have a financial benefit to end users. If the reforms do not reduce overall costs, they will for the most part simply change the way in which end users pay these costs as they will now arise through DUoS rather than through the wholesale electricity price.

However, there are significant risks around the issue of anticipatory investments, and while Ofgem says it wants DNOs to be more proactive, the structure of RIIO-2 does little to support this aim. If Ofgem’s uncertainty mechanisms prove to be too slow or unwieldy then DNOs will naturally continue to avoid anticipatory investments even if this increases costs to consumers in the longer term. Given Ofgem’s track record, there are few reasons for optimism on this point.

A couple of interesting posts, thanks.

I still don’t get the electricity grid as a business system though. Why isn’t the electricity grid paid for in the same way as mobile cellular systems are? Mobile phone netowrks costs a lot of capital but as consumers we pay for them mostly on a usage basis. Both monthly and PAYG charge by usage (by and large) and don’t have a fixed connection fee. In the future could the grid be paid for purely by usage charges rather than a mixed connection charge and usage-basis charge? Why is the electricity grid different, could it be because it’s a monopoly?

Almost all phone companies are now operating with a significant minimum fixed charge. It is very hard to find a SIM only deal that costs under £60 a year if you are a low volume user (still just possible). That’s with a £5 a month minimum topup with the credit for unused minutes expiring monthly. Charges per minute, text and MB for non expiring credit PAYG have soared in most cases by a factor of 10 or more.. The main business model now is leasing high end phones on hefty monthly premiums.

At the end of the day this is about recabling the streets and installing beefier transformers to cope with demand for EVs and electrified heating, with more embedded intermittent generation as an additional factor in some areas. In reality they need to work backwards from the end picture in order to work out whether this really is an acceptable way forward in the first place, and then how to allocate the cost fairly if that is so. It’s a £300bn bill according to the GWPF research. These proposals seem to be inclined to deny that reality, and favour green interests at the expense of the rest of us. Par for the OFGEM course.

With DNOs being expected to somehow magically identify the exact right investments to make at the exact right time to minimise costs for consumers…