In recent weeks, much has been made of the fact that coal has dropped out of the merit order for days at a time. While much of the commentary is around trying to prove that the system can run just fine without dirty thermal power (conveniently ignoring the reliance of the system on coal during the “Beast from the East” cold spell, where without coal, the lights would almost certainly have gone out), where this change is more significant is in terms of the impact on system management.

Particularly in the summer, where demand can be weaker, and solar generation higher, the proportion of demand being met by generation that does not provide inertia to the system increases. This makes maintaining the system at 50 Hz more challenging.

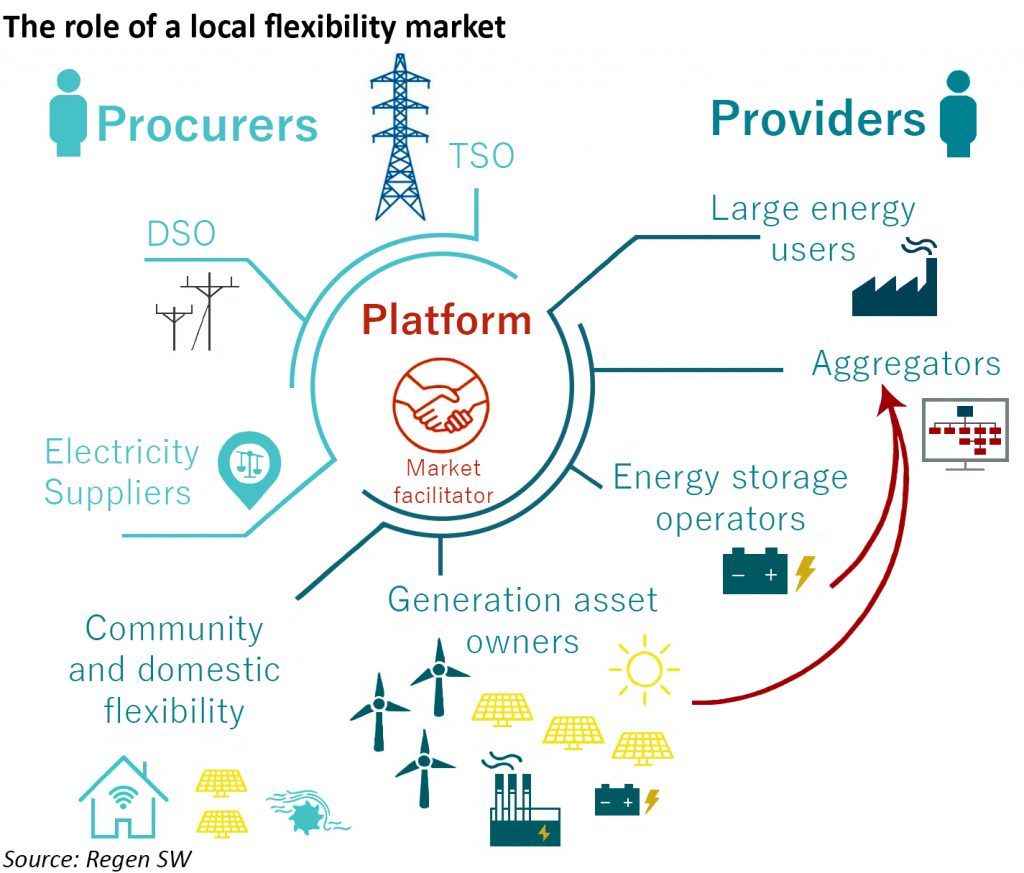

Development of local flexibility markets

National Grid is working on a number of initiatives aimed at addressing this issue. Six energy companies (Flexitricity, Belectric, Centrica, Orsted, Siemens and GE Grid Solutions) and two universities (Manchester and Strathclyde) are working with the system operator in the Enhanced Frequency Control Capability (“EFCC”) project, which has developed a new monitoring and control system to manage the grid. This new system will help maintain system stability during peaks in supply and demand, using a range of technologies:

- Belectric will provide response from its PV plants and storage facilities;

- Centrica will play a dual role, providing response from both large-scale generation at Langage and South Humber Bank combined cycle gas turbines and Lincs and Lynn or Inner Dowsing windfarms;

- Orsted and Siemens will use wind turbines to demonstrate the capability of wind farms to provide fast, initiated frequency response and to measure the associated costs; and

- Flexitricity has recruited industrial and commercial customers for a demand side response trial.

The project will assist with the development of new commercial services for rapid frequency response.

“The EFCC project will provide greater visibility of the grid system performance by using real time data. By working together with industry partners we can lead the transition to a new energy future. Not only will this help to deliver greater value to consumers by running the system more efficiently, it will also evolve and future proof the grid,”

– Lilian Macleod, EFCC Project Manager, National Grid

At the same time, distribution network operator Scottish and Southern Electricity Networks (“SSEN”) is to trial a new marketplace for local flexibility hosted by Open Utility through its online trading platform Piclo. Piclo already offers a peer-to-peer trading service, that was launched in 2015 following a trial sponsored by BEIS. The service will enable the company to manage network constraints by buying flexible capacity from providers such as battery operators and demand-side response aggregators.

UK Power Networks was the first DNO to sign up to the service in January. Through the Open Utility platform, the DNOs are exploring ways of lowering barriers to entry for flexibility tendering and creating a flexible and inexpensive way to access the flexibility they increasingly need to reduce the need for network reinforcement.

The trial will start at the end of May, when a limited number of battery operators and demand-response aggregators will be able to register to participate via Open Utility’s website, with trading due to start later in 2018 and continuing for the rest of year. The company is aiming to launch the service commercially in 2019.

“Unlike other industries like short-term rentals and taxi services, the energy sector cannot be transformed by an online marketplace acting alone, but through meaningful partnerships with incumbents working towards a common goal,”

– James Johnston, CEO, Open Utility

Local flexibility markets will not necessarily be scaled-down versions of TSO services

According to analysis by Regen SW, a not-for-profit organisation which promotes renewable energy and energy efficiency in the South West of England, the results of the various local flexibility trials show that the need for flexibility at the local/distribution network level is very different to the needs of the national transmission system.

The transmission system operator (“TSO”) calls on assets to respond to deviations in system frequency through the various frequency response services, or to provide supplementary capacity or energy reserve through the Short-Term Operating Reserve (“STOR”) or the Capacity Market. The location of the assets providing these services is generally not a factor, with location signals coming through the locational component of transmission use of system charges rather than in tenders for ancillary services. The Capacity Market is entirely location independent, with contracts being awarded exclusively based on price.

Things are likely to look very different at the local level, where the primary driver (so far at least) is to avoid network expansion investments. Location will be the key to the services that meet this need, as they will address specific local constraints including at the substation level. These local constraints often persist only for short periods of the year at times of peak demand or generation.

DNOs will consider procuring flexibility services as an alternative to investing in new network capacity, the costs of which would be recovered through distribution use of system charges. Where the requirement is limited in size and or duration, procurement of flexibility services may be more efficient than network reinforcement, however, the amounts are likely to be far smaller than at the TSO level – ancillary services such as Fast Frequency Response have a minimum capacity threshold of 1 MW, but examples from the recent Electricity North West expression of interest for flexibility services have a minimum size for directly contracted resources of just 100 kW.

Local flexibility services likely to favour existing assets

As the needs for individual flexibility provision at the local level are likely to be small, existing assets are most likely to participate since the value of the procured services is unlikely to be enough to support the investment case for a new asset. Overall, the market is estimated to be worth in the range of £10,000-25,000 /MW of flexible capacity per year. Platforms such as the one being developed by Open Utility could play an important part in the emergence of this market, since it will be important to make the procurement of these services as low-cost as possible to make them attractive for market participants.

A range of technologies may find a place in local flexibility markets. The most obvious would be embedded generators, with the ability to flex their output, but even traditionally inflexible assets such as wind and solar could participate through voluntary curtailment if the payments were competitive.

Large energy users also have significant potential to participate in the market – industrial sites could be among the largest or most volatile individual loads connected to a constrained substation, meaning the behaviour of this site could be both one of the causes of and the solution to the operational constraints arising at that substation. The challenge is whether the rewards for this service would be enough to compensate for the disruption to their operations.

Participation in flexibility markets forms a key part of the business model for energy storage operators, so they would aim to include local flexibility services in their stacked revenue models. As competition for transmission-level services grows, local markets may play a role in supplementing the income for storage sites.

A segment of the market that is currently un-tapped, but that could play a significant role in the future is the domestic market. In 2017 there was 121 MW of community-owned capacity across England, Wales and Northern Ireland, and the scope for flexible capacity will grow as the markets for electric vehicles and domestic storage develop.

Aggregators are likely to intermediate between householders and DNOs, accessing smart appliances to provide demand response, possibly as part of emerging markets for energy services. Of all the potential participants in local energy markets, this is the most remote – currently there are no aggregators serving the domestic segment, and there are questions around metering that will need to be addressed if domestic premises are to export back to their local networks.

Widening access to the Balancing Mechanism

Meanwhile in April, aggregator, Flexitricity announced the launch a new energy trading service called Flexitricity+ which will give industrial and commercial energy users access to the Balancing Mechanism, an important and valuable segment of the electricity market.

The Balancing Mechanism (“BM”) is used by National Grid to match supply and demand in close to real time. Market participants submit bids and offers indicating the levels at which they are willing to adjust their generation or consumption at different times, and National Grid will accept those bids or offers which will enable it to balance the system most efficiently. Around 3,000 balancing actions are taken by the system operator each day, in a market that is worth around £350 million per year. Prices in the BM can reach up to £2,500 /MWh.

Current industry rules mean that electricity consumers can only participate in the BM via their supplier however, according to Flexitricity, as many of the large suppliers also have their own generation assets participating in the BM they have little incentive to offer their customers’ flexibility to the system operator. This has prompted Flexitricity to itself become a licensed supplier, and it will allow its customers to access the BM if they use the company as their supplier.

The company will carry out trades on behalf of customers according to constraints and instructions set out in advance, in exchange for a share of the proceeds. The new service, which is due to launch in October, will initially be targeted at businesses and public sector organisations.

“This is the first time anything like this has been done in the balancing mechanism and we think it will be transformational. We are unlocking value for our customers as well as for bill-payers across the country by making our electricity system more efficient,”

– Ron Ramage, CEO, Flexitricity

In fact, Flexitricity isn’t the first to offer this service: Smartest Energy already uses its supply licence to offer access to the BM to its customers.

Elexon is planning to introduce changes to the Balancing and Settlement Code central services in 2019 to open the BM to independent aggregators. The code administrator has also published a white paper setting how the services could be adapted to enable customers to buy electricity from multiple suppliers, which would also widen access to the BM.

Granular real time supply and demand data needed for efficient system management

The next few years are likely to see more trials such as these as system operators try to accommodate the market changes they face, however it is difficult to see how they can be efficient without comprehensive information systems developing at the same time.

Effective system management in an increasingly variable system will require both transmission and distribution system operators to have real time supply and demand information on their networks, as well as accurate information about the available capacity and flexibility of assets and sources of demand connected to it.

There are significant limitations to the depth of data currently available to system operators, and while initiatives to expand half-hourly metering are helpful, they do not go far enough to address the need.

As well as developing trading platforms for flexibility services, market participants should develop strategies for delivering the necessary data capture – starting to address these needs in the 10-20 year replacement cycle for those electricity meters that are not already scheduled to be replaced by smart or advanced meters. There is also a need to consider behind-the-meter capacity and its impact on the networks. New trading platforms are just the start.

This PhD thesis:

http://orca.cf.ac.uk/35740/

shows you are right that it takes a lot of communication to operate a smart grid. Whether it all works in practice is as yet somewhat unproven.

Here’s one way it might easily fail:

https://www.reuters.com/article/us-germany-cyber-russia/german-intelligence-sees-russia-behind-hack-of-energy-firms-media-report-idUSKBN1JG2X2