Last week Ofgem has published its consultation for the next round of price controls for energy networks, known as RIIO-2. RIIO-1 had been strongly criticised for allowing network companies to generate above average levels of returns on businesses that are seen to be less risky than the wider economy. Network companies have been earning returns of around 10% on average, double the average UK share return of 5%, despite being low-risk businesses which should yield relatively lower returns.

RIIO involves setting Revenue using Incentives to deliver Innovation and Outputs in gas and electricity networks. The current price controls for electricity transmission operators are due to end on 31 March 2021, while those for distribution network operators run until 31 March 2023. RIIO-2 is set to be much tougher than its predecessor.

Electricity network costs have been growing in recent years, contributing to increasing consumer bills – network costs account for just over a quarter of bills, making this a politically sensitive topic. The new rules proposed by Ofgem could result in savings of £5 billion on energy bills over five years, or £15-£25 per year for each household, by implementing a massive reduction in the cost of equity used in determining the baseline rate of return for the network companies, from 6-7% in RIIO-1 to 3-5% for RIIO-2. Ofgem is also exploring changes to the way it calculates the cost of debt.

Responding to a changing market environment

Energy markets are undergoing fundamental changes, driven by environmental policies aimed at reducing carbon emissions while maintaining security of supply and affordability for consumers. These changes have been rapid, and further major upheavals to the energy system are still to come, posing significant challenges to Ofgem in developing a regulatory environment that supports these changes without undermining any key policy objectives.

“Looking ahead to the next decade, we will see further changes in how these networks are used. We are likely to see an increasing uptake of electric vehicles and electric or renewable heat. How consumers interact with the networks will also change. Nearly one million homes already have solar panels, generating electricity both for their own use and to sell to others.

Through our Regulatory Sandbox we are supporting trials of peer-to-peer local energy trading platforms. The rollout of smart meters will enable consumers to track more closely how and when they use energy. New services will emerge to help them find the best deals.

Batteries (including those in electric vehicles) could increasingly provide flexible and inexpensive storage to smooth out peaks in demand during the day. The development of new markets and technologies and better use of network infrastructure means that building new pipes and wires may not always be the best response to increasing demand,”

– Dermot Nolan, CEO, Ofgem

When RIIO-1 was launched in 2013, Ofgem wanted network companies to respond to the changing needs of their consumers, delivering outputs that consumers valued, such as improved reliability or better customer service. Networks are now more reliable, and consumers are highly satisfied with the service provided by local network operators, however, as noted above, returns were excessive relative to the risks faced by these businesses.

Ofgem is now proposing a range of reforms to address these concerns.

Economics: establishing fair returns while ensuring financeability

One of the reasons that RIIO-1 ended up enabling network companies to earn such high returns was the difference between Ofgem’s initial assumptions, and what played out in practice. The long, 8-year price control period together with the lack of an adjustment mechanism allowed this situation to persist.

As a result, Ofgem is proposing to set a default price control length of 5 years (returning to the duration that was used prior to RIIO-1), but will challenge the network companies to make a compelling case for some allowances to be set for longer if this could deliver benefits for consumers.

The key adjustments to the determination of regulated returns under consideration are:

- An improved approach to setting the cost of debt;

- Re-basing the cost of equity to 3% – 5% based on current market conditions, with possible indexation;

- Reviewing the treatment of tax by either, (i) continuing with the current approach of calculating a notional tax allowance, (ii) using tax values paid to HM Revenue and Customs, (iii) taking the lower of either (i) or option (ii), or other alternatives proposed by stakeholders;

- Moving away from retail price index (RPI) for the treatment of inflation;

- Development of new mechanisms to ensure fair returns for both companies and investors through either a hard cap/floor, discretionary adjustments, constraining totex and output incentives, a RoRE sharing factor, or anchoring returns.

To ensure a lower baseline allowed return does not affect the financeability of companies, Ofgem is considering three options, (i) adopting a nominal return instead of a ‘real’ return; (ii) doing nothing and putting the onus fully on the companies; and (iii) protecting the companies’ ability to make debt payments.

Significant reductions in the cost of equity

Ofgem estimates that each percentage point increase in the cost of equity will be worth about £0.4 billion for each year of RIIO-2 – equivalent to around £7 – £10 per household each year. Unlike the cost of debt however, the cost of equity is an inherently unobservable quantity which requires estimation using some model of investor expectations.

Ofgem is proposing to continue using the Capital Asset Pricing Model (“CAPM”) as the basis for estimating the cost of equity, with a number of changes to its methodology.

The CAPM computes the cost of equity as the weighted average of a risk-free rate and the expected return on the stock market as a whole. The less risky it is for investors to own the shares in a network company relative to investing in the wider stock market, the greater the weight placed on the risk-free rate and the lower the weight placed on the expected market return. The weighting factor is known as the equity beta, and measures the relative riskiness of a network company from an investor’s point of view.

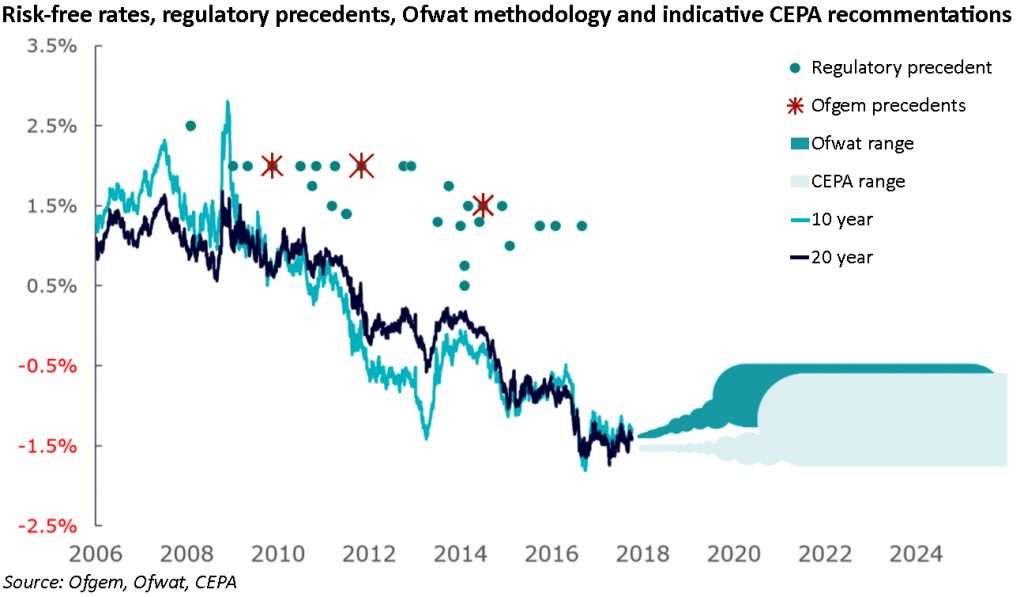

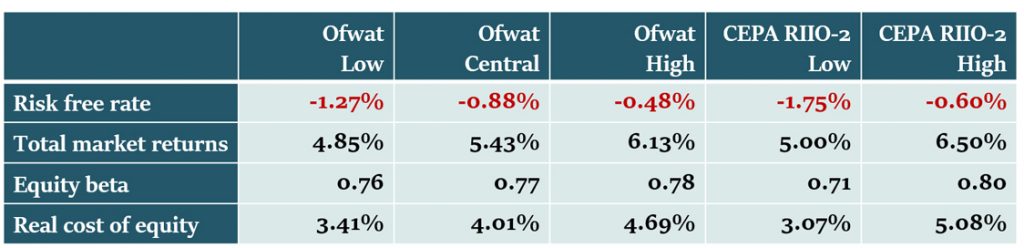

The rates for long-term debt (10-20 years) are currently negative at around -2%. In the past, regulators have assumed a positive figure of about 1-2% to take account of any potential reversion of interest rates as markets recover from the financial crisis. Current market evidence, suggests an indicative range of -1.8% to -0.6% for the RIIO-2 period. Rather than “aiming up” to guard against a future increase in rates, Ofgem is proposing to index the cost of equity to ensure the risk-free rate remains in line with financial market conditions.

[Ofgem commissioned Cambridge Economic Policy Associates (“CEPA”) to review the RIIO-1 price controls and provide recommendations for RIIO-2.]

The total market return is a measure of the return that equity investors expect for the market-average level of risk and is usually approximated by measuring the historical realised returns from investing in the stock market as a whole. Equity returns can be highly volatile from year-to-year, so it has been common practice to use very long-run historical averages of realised returns as the best estimate of investors’ future expectations of the TMR. The long-run historical average of the TMR is approximately 5% – 6% based on the period 1899 to 2016.

In 2014, the Competition Commission found that an appropriate range for the expected TMR was 5.0 – 6.5%, and water regulator Ofwat has considered forward-looking approaches to arrive at a range of 4.9% – 6.1%. CEPA broadly concurs with this assessment, and recommended an indicative range of 5.0 – 6.5% for RIIO-2.

The equity beta measures the relative riskiness of holding shares in network companies, which investors cannot diversify away by holding shares in lots of different firms. CEPA’s analysis indicated that – assuming gearing between 50 and 65% – the equity beta implied for RIIO-1 of c 0.9 may be too high for RIIO-2, and recommended an indicative range of 0.7 – 0.8.

However, a report commissioned by the UK Regulators Network (“UKRN”) uses various econometric techniques to filter out some of the noise from daily share price movements and found that that equity betas in the range 0.3 – 0.5 would be ‘econometrically defensible’ ie the equity beta could be less than half the value assumed for RIIO-1, meaning that network companies significantly less risky as investments than previously assumed.

Based on plausible ranges for the three CAPM parameters set out above, CEPA suggests a plausible range for the cost of equity for RIIO-2 could lie between 3% – 5%.

Minor adjustments only sought for the cost of debt

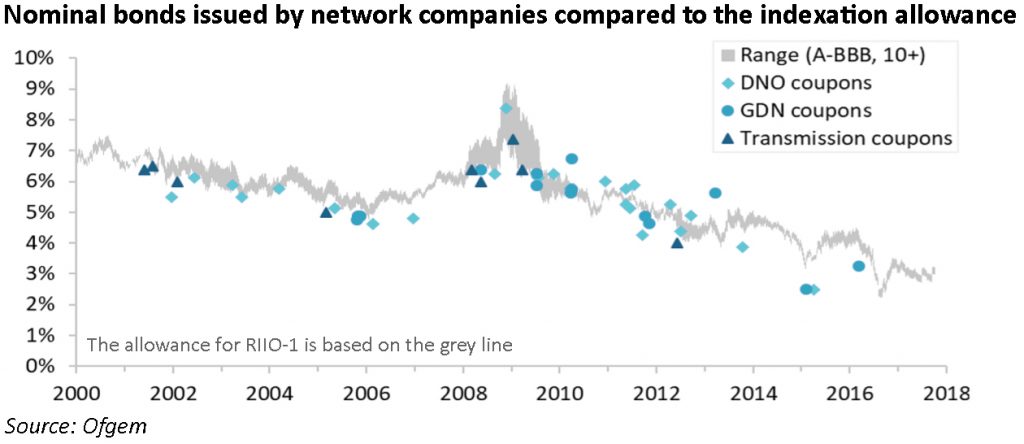

The cost of debt is currently calculated on the basis of a trailing average of market rates over the previous decade. The consultation document says the introduction of indexation for the first RIIO period has “worked well” and Ofgem is would need persuading to make changes to its methodology, but it recognises “In most cases, the actual cost of debt is lower, sometimes significantly, than the benchmark index we use for RIIO-1”.

Although Ofgem is inclined to retain the general overall approach to cost of debt developed for RIIO-1, there are some areas in which some improvements are being considered:

- Re-calibrating the RIIO-1 indexation policy: testing how the RIIO-1 approach would perform against a range of future interest rate scenarios taking into account the efficient debt expected existing and future debt raised by network companies. If the indexation approach used in RIIO-1 produces a systematic over or under estimate of the efficient cost of debt, Ofgem could modify some of the underlying assumptions.

- Implementing a fixed allowance for existing debt plus indexation for new debt only: the Civil Aviation Authority (“CAA”) and Ofwat both propose to set an allowance for debt costs as the sum of two distinct parts: (i) a fixed allowance for the cost of debt issued before the price control period beginning; and (ii) an additional allowance (based on IBoxx’s market indices) for debt issued during the price control period. The principle is that regulators can observe the actual financing costs for historical (but not future) periods, based on debt issued by companies, thereby use of a market index avoids forecasting errors related to future interest rates.

- Creating a pass-through allowance for debt: some companies have argued that they cannot meaningfully control their cost of debt, either in terms of the market prices, or in the timing of efficient investment. By “incentivising” companies with a debt allowance, they argue that consumers could be worse off, relative to having no incentive at all, and, unless all companies raised their debt in exactly the profile assumed by the index, some companies could be over-compensated and others under-compensated without any benefit to consumers.

The indexation element will be key. In a world of rising interest rates, the long-term lag used in calculating cost of debt could deviate significantly from the rates available to companies for borrowing. Calibrating an additional allowance to Iboxx indices also has its drawbacks, since these cannot be hedged.

Indeed, the topic of hedging raises further questions since it is common practice in the industry for regulated utilities to separate financing from risk management through an extensive use of swaps.

Ofgem will need to take care that in setting its cost of debt rules, it does not inadvertently create incentives for the network companies to finance themselves in the short-term debt markets…as the differential between the yield curve and long-term historic average widens, companies would (on a pure cost basis) find financing in the overnight debt markets a way of boosting their returns.

Maintaining financeability against a backdrop of lower returns….

Ofgem has a duty to consider the network companies’ ability to finance their activities. Since network companies are obliged under their licences to take steps to maintain an investment grade credit rating, Ofgem has historically assessed financeability by following the methodologies published by rating agencies, as applied to a notionally geared, efficient network company, and proposes to continue with this in RIIO-2.

The changes to the cost of equity described above, combined with a lower cost of debt using the market tracking index, are likely to lead to a much lower baseline allowed return for RIIO-2, which may make it more challenging to meet the standard financeability metrics. Ofgem has conducted an initial impact assessment and found that company performance on financeability metrics may indeed deteriorate.

Ofgem has identified three high-level policy options for addressing financeability issues:

Adopting a nominal return instead of a ‘real’ return calculation

One impact of reducing the cost of equity is that a larger proportion of the total return is received over the longer term whereas debt interest costs occur within the current year. Paying the cost of capital on a nominal basis each year would eliminate the timing mismatch issue and ease the financeability concerns. It would increase charges for consumers in the short-term, but charges would reduce later in the life of the asset resulting in approximate net present value neutrality between the two approaches.

This option would be a significant change to the regulatory framework, and could reduce demand from investors with inflation-linked liabilities (eg pension funds) who target inflation-proof investment opportunities.

Putting the onus on the companies to address financeability through de-gearing or other measures

This option is based on the principle that it is the companies’ own responsibility to address notional or actual financeability constraints, creating a requirement for them to address any potential financeability in their business plans, and securing additional equity injections as necessary to reduce actual gearing to notional levels.

Ofgem could adopt a similar approach to Ofwat, which permits operators to address financeability issues by accelerating depreciation and modifying rates of capitalisation, however, early discussions with the rating agencies suggests that they will discount these approaches.

Introducing a revenue floor that provides assurance of interest payments on debt on a notionally geared basis

This involves limiting the downside risk of the price control package to give greater assurance that debt costs will be met by introducing a licence condition that sets a floor below which company revenue would not be allowed to fall. The floor could be set at a level that would allow a notionally geared company to more easily service interest payments equal to the cost of debt allowance.

Ofgem believes that this approach could allow it to lower charges in both the short and longer term. A positive impact on credit ratings could reduce the rate of interest lenders would require, with lower default risk also acting to reduce rates. The trade-off would be that consumers would need to fund a revenue floor for a company in an (extremely unlikely) downside situation while recovering this additional revenue once the company’s trading position improves.

…while delivering value for consumers

Consumers benefit if network companies are able to reduce their costs and deliver better service. RIIO aims to achieve this by incentivising companies to ‘beat’ cost allowances and output targets – if companies can deliver “more for less” they can earn higher returns and consumers gain from better service and a share of any underspend in the form of lower charges. This is not always borne out in practice, as assumed investment may not materialise or may be delayed.

Ofgem recognised that the measures it has used so far to mitigate the risks of over-relying on forecasts have not been sufficient to restrict overall returns to acceptable levels. For RIIO-2, Ofgem intends to update and enhance its existing tools:

- Indexing costs where feasible;

- Linking costs to the delivery of outputs;

- Using uncertainty mechanisms to automatically adjust costs and volumes with changes in the external environment;

- Where there is doubt over cost allowances will not be set until there is more certainty;

- Tough output targets and cost allowances will be set;

- Use of efficiency incentives to allocate over and underspend between companies and consumers to better reflect the balance of risks.

One way to guard against these risks would be to remove incentives on outperformance and instead set companies a fixed rate of return. Ofgem does not believe this would benefit consumers as without incentives to find efficiencies, it will be harder to drive down costs over time or provide the right environment to support the energy system transition. Ofgem has identified five options that could guard against higher than expected returns, while retaining an incentive-based framework:

- A hard cap/floor – this would restrict returns from rising above or falling below pre-determined levels. Although this would reduce the risk of excess returns, it could also undermine the effectiveness of incentives as company returns approach the margins. Once a company reached the cap there would be no further incentive to improve.

- Discretionary adjustments – using discretionary adjustment mechanisms within or at the end of the price control period, to account for variations between forecasts and actual expenditure/output performance. The conditions for adjustments would be specified in advance and could include when returns exceed pre-set levels and the company has not provided evidence that they achieved this through genuine efficiency improvements.

- Constraining totex and output incentives – measures to reduce the returns gained through totex outperformance would be paired with measures to limit the financial rewards from incentive payments, so consumers receive a greater share in any gains. While this may weaken incentives on companies to inflate their business plan, it may also weaken rewards for significant cost efficiencies. Ofgem is considering either zero-sum incentives, or providing a fixed incentive pot for which companies would compete to receive a share.

- A RoRE sharing factor – setting the levels at which consumers share in efficiency gains depending on the quality of business plans submitted by companies. Poor quality or uncompetitive plans would see consumers getting a larger share of the company’s return while a high quality plan would mean the company’s return would be adjusted upwards where the baseline return falls below the baseline cost of equity.

- Anchoring returns – regulating revenues so that the RAV-weighted average return across a sector would be capped (an anchor point). When the sector as a whole performs within this band, the returns earned by individual companies would reflect performance against their own targets and allowances, however if the sector average exceeds the band, all companies in the sector would be required to refund consumers in proportion to their RAVs or regulated equity, so the RAV-weighted sector average remains at the limit of the range.

Controlling costs for consumers does not mean bills will fall

In a statement, Ofgem said of its plans:

“In total we estimate this would result in savings of over £5 billion for household consumers (or about £15 – £25 per year on the dual fuel household bill) who pay for the network through their energy bills.

Ofgem is able to drive forward a tougher regulatory framework for the next price control thanks to a stable, predictable and low risk regulatory regime which ensures consumers benefit from high levels of investment and innovation at the lowest cost. This regime has already delivered significant benefits.”

Citizens Advice, which in July 2017 released a report claiming that energy network companies had made £7.5 billion in “unjustified” profits responded positively to Ofgem’s proposals, but said the consultation process would demonstrate whether Ofgem is able to deliver a better deal for consumers:

“Today’s announcement is a major step forward. These proposals should prevent a repeat of the billions in excess profits energy network companies are making under the current price controls. This means better value for consumers and potentially lower bills. The outcome of this consultation will be the acid test for Ofgem. It’s crucial that the regulator holds its nerve and sees through these changes. Curbing the ability of energy network companies to make excessive profits, limiting the price control to five years, and ensuring a greater voice for consumers are all measures that should take us closer to a towards an energy market that genuinely works for consumers,”

– Gillian Guy, CEO at Citizens Advice

David Smith, CEO of Energy Networks Association, which disagreed with the Citizen’s Advice report last year said:

“Energy networks are the nerve-centre of a smarter, cleaner energy market, responsible for delivering a range of exciting new services for our homes, businesses and communities. Balanced regulation is fundamental to delivering these and the price control system should evolve to suit the changing needs of consumers. RIIO-2 must deliver that whilst being founded on the principles of transparency and stability to provide predictability for investors, innovators and consumers alike.”

The first RIIO price control was certainly too generous to the network companies, and with its proposals, Ofgem is attempting to address those issues, but there is reason to be cautious. Another period of excess returns for network companies would be very damaging for the regulator, but care must be taken to avoid incentivising risky behaviours or dis-incentivising investment through inappropriate treatment of the cost of capital.

Despite headlines about potential savings – the costs of the energy transition are only increasing, and often these “savings” are relative meaning that costs would increase less under one approach than under another approach. Consumers should not read this and think bills will fall.

Stakeholders have until 2 May to respond to the proposals. Ofgem will finalise the framework for setting the next price controls in summer 2018. The companies will submit business plans by autumn 2019. Ofgem’s final view on price control allowances will be published by the end of 2020.

Leave A Comment