Last week, Energy Secretary Ed Miliband announced the Administrative Strike Prices for the upcoming 7th auction round for the Contracts for Difference subsidy scheme. These represent the maximum prices he is willing to pay for each technology type. Or I should say, the maximum he is willing for consumers to pay, since it is us and not him that does they paying. Not only have the contracts been extended from 15 to 20 years, but the new maximum strike prices, the highest in over a decade, are eye-watering.

This should finally end the claim that renewables are cheap, since even at the first order level, that is the subsidy, they are likely to be higher than the cost of generating electricity using gas. Even for solar which is the cheapest of the lot.

We have suspected for some time that AR7 was going to be expensive. The Government delayed the issue of the methodology while it consulted on various changes to the contracts and budget setting, the outcome of which clearly prioritises volume over value. And we know that with the Clean Power 2030 targets just about all of the projects will need to secure contracts meaning there will be little or no price tension in the auction.

And we also know that turbine makers have increased their prices significantly, driven by a combination of factors: tightening warranties after years of claims hurt their balance sheets, passing though higher raw materials and financing costs and increasing profitability after years of losses, and, more recently, the impact of US tariffs, particularly on steel.

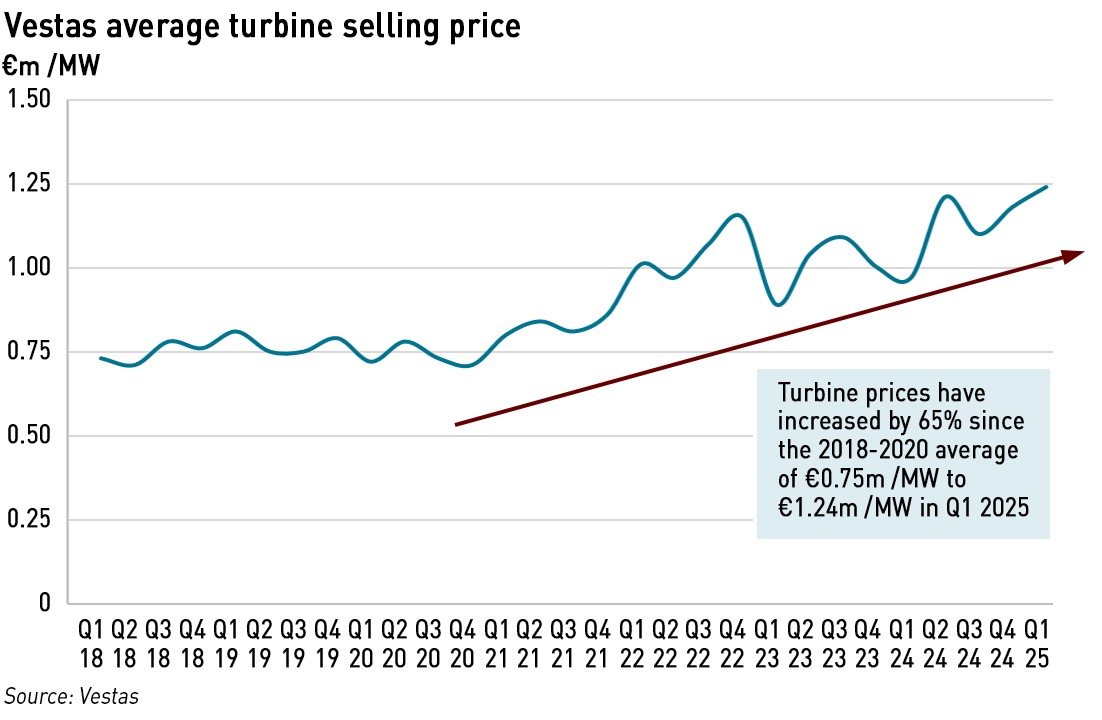

A report by developer Ørsted found that the costs of offshore wind have increased by 50% since 2020. Vestas has increased its average selling price for wind turbines from €0.75m /MW in 2018-2020 to €1.24m /MW in Q1 2025, and increase of 65%. It’s clear from the chart that this is a persistent rising trend, with no quarter since the start of 2021 being close to the average price over the previous three years. It is therefore difficult to justify an assumption that prices are falling or will fall in the near future – the trend shows the exact opposite.

So what are the new Administrative Strike Prices (“ASPs”) and how do they compare with previous years?

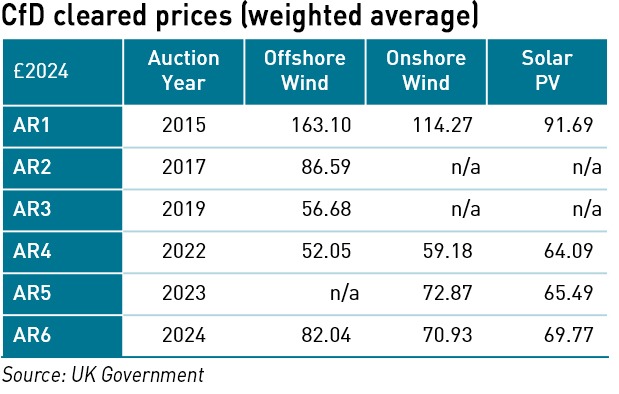

The cleared auction prices for the previous auction rounds were:

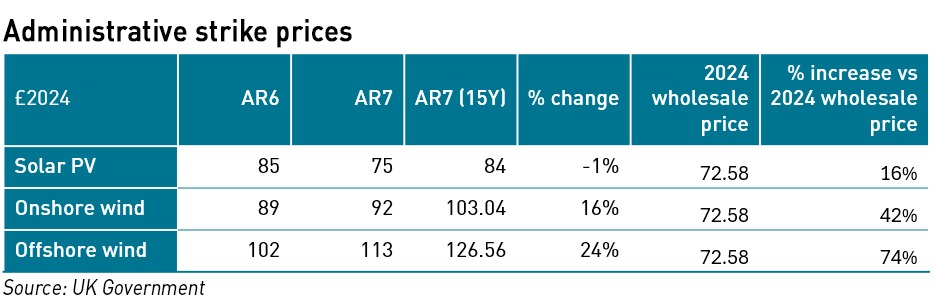

These are quoted in 2024 money (£2024) since this is the new indexation the Government is now using (from £2012 previously). The new ASPs fort AR7 compared with AR6 are below. There is an additional column showing an estimated 12% uplift which is roughly the value of the contract extension, so in order to compare like with like, this adjusted column puts the AR7 ASP onto an equivalent tenor basis:

When compared with the actual wholesale power price in 2024 (average of the N2EX day ahead prices), it can be seen that solar and onshore wind priced slightly below gas-based electricity generation while offshore wind was 13% higher. That apparently was too low for some, as Ørsted later cancelled the flagship Hornsea 4 project. The new ASPs are, except for solar, significantly higher in AR7 than AR6, but all of them are higher than the gas-based wholesale price of electricity last year.

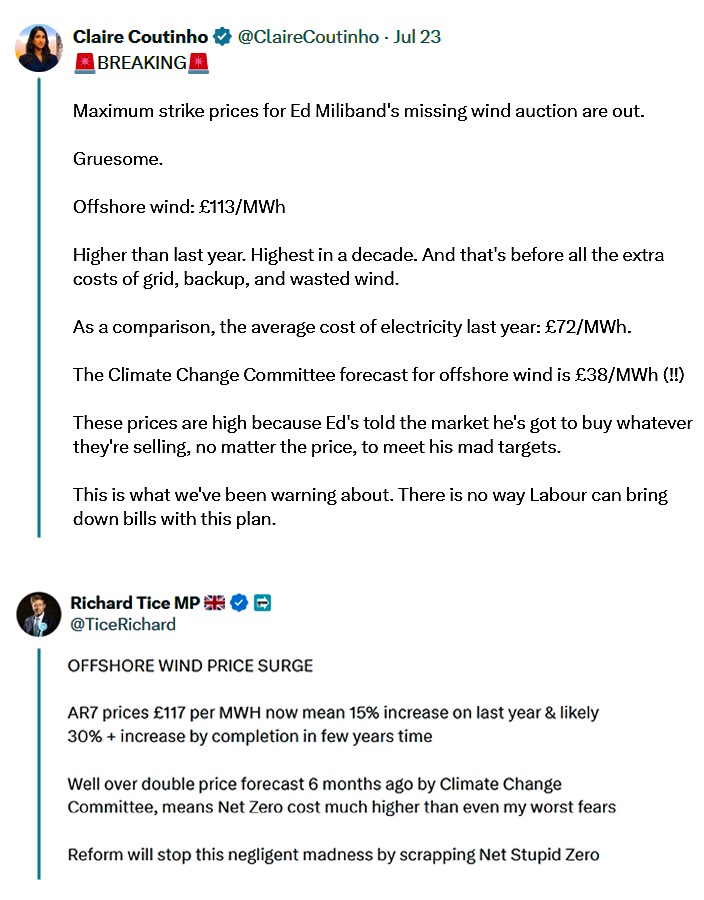

“One of my major battles in the Department was getting them to work out the true cost of renewables. Ed’s scrapped that work. The entire government machine and surrounding ‘independent’ bodies are working off of completely bogus numbers that don’t reflect the true costs. And we will all pay the price,”

– Claire Coutinho, Shadow Energy Secretary

Of course for a proper price comparison it is necessary to add the full system costs to the renewables, that is the costs of backup for when it’s not windy or sunny, the costs of connections which are higher for renewables given their lower energy density (more wires are needed for the same MW), the costs of curtailment where windfarms have been built behind grid constraints so their electricity cannot be used, and the costs of real time balancing, which are increased by the real time intermittency of wind and solar – gusts of wind and clouds create real time output variations.

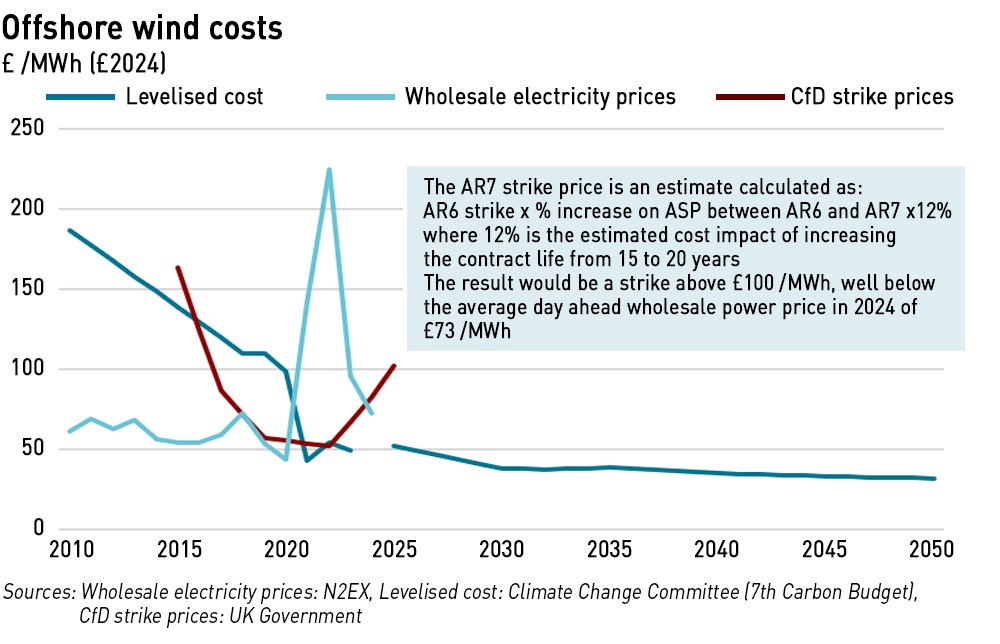

The offshore wind prices are also significantly higher than the levelised cost assumptions made by the Climate Change Committee in its 7th Carbon Budget.

Surely this is proof renewables are not cheap

If these ASPs are any indicator of where the auctions will clear, and we have to believe they are, otherwise why would they have increased, then it is likely that the cleared strike prices will be higher than in AR6, which extends the rising trend since the low of AR4.

If these ASPs are any indicator of where the auctions will clear, and we have to believe they are, otherwise why would they have increased, then it is likely that the cleared strike prices will be higher than in AR6, which extends the rising trend since the low of AR4.

AR4 is widely thought to have been unrealistically low – developers re-bid their maximum volumes in AR6 after AR5 failed for offshore wind attracting no bids at all, and also petitioned the government for additional economics in the form of tax breaks.

But since AR6 prices more or less at or above the gas-based wholesale price of electricity, anything higher will fully undermine any arguments that renewables are cheap. If the first order cost – the subsidy – is above the price of generating electricity with gas (after the addition of carbon costs) then clearly the all-in system costs including backup, connections, curtailment and balancing will be far higher.

The Conservatives and Reform smell blood in the water. How can Ed Miliband possibly sign 20-year contracts with headline strikes above the current wholesale price? How can he continue to claim renewables are cheap? And how can he honour Labour’s promise of a £300 reduction in bills when such a subsidy hike would see bills increase?

However if he does not sign these contracts he will be unable to deliver the renewable capacity increases required for his Clean Power 2030 Plan.

“We estimate that the net costs of Net Zero will be around 0.2% of UK GDP per year on average in our pathway, with investment upfront leading to net savings during the Seventh Carbon Budget period,”

– Climate Change Committee

This may well be make or break for Miliband. Keir Starmer is showing signs of concern over energy costs, and when the £300 savings will emerge since this was such a high profile campaign promise. Yet it seems to have escaped everyone’s notice that the Climate Change Committee has contradicted these claims saying there will likely be no net zero savings until the 7th carbon budget period in 2038-2042, ie not in 2030 as Miliband claims. Starmer may well step in a prevent AR7 clearing at the expected high prices on the basis that it will make the £300 promise impossible to deliver.

This would likely cost Miliband his job. It’s hard to see how he could remain in post if he has to choose between a failed auction or much higher strike prices, and it’s hard to see how Starmer can avoid sacking him if he pushes electricity prices up rather than down.

The omens are not good. Turbine prices are clearly higher, as are financing costs. And industry gossip was suggesting even higher prices, above the offshore wind ASP, which may well exclude some projects that might have bid if the ASP was set higher.

Miliband has staked everything on renewables being cheap. But with subsidy levels increasing and with a good chance of being materially above the cost of gas-based generation for wind if not solar, it will be hard to defend that message. Perhaps a failure to close AR7 at a reasonable price will force Starmer to remove his Energy Secretary, despite his popularity with Labour members, and install a more moderate replacement who will re-set energy policy based on evidence rather than ideology.

We can but hope.

Can we assume the gas price will remain constant?

The gas price is falling. By the end of this year new LNG will have fully replaced Russian gas. By the end of the decade the global market will be long gas

Last July the price was US$ 2 /BTU and this July US$3.2 /BTU. You cannot compare the strike price of wind and solar (capex and operational costs) against the market price of gas (just operational costs). With electric demands likely to double over the next 10 years you have to compare like with like, ie also include the cost of new gas stations. Even a strike 13p/KW hour is well below average electricity prices of about 30p/KWhour that most people are paying.

The $2/MMBtu price was the result of Biden imposing delays on LNG liquefaction and export facilities so there was a surplus of gas and depressed prices. The current UK price of 78p/therm is about $10.50/MMBtu, leaving an ample margin for liquefaction and shipping and regas against the $3.20/MMBtu quote. NG futures prices are quoted out 12 years ahead and peak only slightly above $4/MMBtu, still leaving ample margins against NBP futures. The US domestic market is expected to be in better balance, but with no shortage of export supply which has been increasing the arbitrage margin.

Relying on gas is possibly the most short sited idiocy since those who resisted Churchill’s transition of the Navy to oil.

Europe doesn’t have any gas supply. We’re also at the end of any pipelines that supply Europe. Shipping of LNG is highly unstable, and security pundits warn of war (have you seen LNG explosions?)

In the event we had a Reform govt after 2029 is there anything to stop them copying the attack on North Sea production by bringing in windfall taxes on the profits of windfarms?

Yes, there is a make-whole clause in the contract to compensate for any change in law

It is simply extraordinary how deliberate obfuscation, obduracy and denial can steamroller irrefutable fact for so long and at such cost to the nation.

Surely the Treasury would have had to sign off on this and thus I would say Reeves and by default Starmer stands square behind it. The mission headline is creating a green energy superpower which this defacto does in their eyes but it wont cut bills for sure but none of these assets will be built much before 2030 if at all.

I would also speculate that they will now further rig the price of gas although with us rejoining the EU carbon trading scheme at some point in the future is going to increase the gas cost as well as conveniently generating more revenue for the exchequer.

Coutinho has found her voice and is coming at it from a far more sensible angle compared to maverick Tice but given she couldn’t even get either of her two colleagues to turn up at the last weeks DESNZ select committee meeting to put in some challenges im not hopeful they are going to get very far.

No, it has nothing to do with HMT because the costs are recovered through bills, not taxes

Thats still a burden on the economy and thus has potential to impact consumer spending and the vaunted growth story so I just can’t see HMT not being involved.

I think it does go before Cabinet. But Miliband seems to have largely had his own way on most energy policy issues so far. I struggle to think of any minister who could put up convincing arguments on alternative energy policies: Miliband’s latest Parliamentary statement in support of net zero was tone deaf, but completely supported by Labour MPs. Really only Esther McVey and Lee Anderson and Andrew Bowie (standing in for Claire Coutinho) seriously questioned it.

Isn’t the reason “by the end of the decade the global market will be long gas” that we will have plenty of renewables to displace the gas?

You’re the expert and I’m not, but could we have predicted in 2019 the trajectory of gas prices to 2024? If not, can we now predict the same to 2030?

Please would you explain what the Administrative Strike Prices are. For example are they the minimum price the producers will get for the wind energy produced or are they the price they will get for every MWh they generate irrespective of the pool price or is it something else

They are the maximum prices at which the auction can clear, providing a cap on the actual strike price

I need to rephrase the question. Will a company who say bids £90 MWh receive £90 for all energy produced or during peak demand when the spot price is say £120 MWH will they receive more?

What they receive is determined by the difference between the Day Ahead Market prices (defined as to how it is calculated in the contract and known as Intermittent Market Reference Price – IMRP) for each hour and their strike price. Where IMRP is negative they will get no compensation at all, and thus have an incentive to self-curtail. Where the price is below their strike price they will be topped up to the strike price, and where it is above they pay back the difference. The LCCC that administers the scheme tot up the payments daily for each CFD, and you can download and examine them for every CFD in operation since they started in June 2016. There is a delay of a few days while metered output data are collected, and minor historical adjustments when metered outputs are revised subsequently (as the contracts adjust for some transmission losses that can only be calculated once more meter readings are collected).

CFD holders are in fact free to sell on any basis they choose, but if they sell either directly via the Day Ahead market or on terms that use those prices then the net subsidy payment will ensure they effectively get the CFD strike price without any risk. Most choose to do so, although company holding structures may show abnormal pricing for the actual company holding the CFD, with contracts with holding companies within the business: what matters are the contract prices for sales outside the group to third parties. The result is the only time they care about market prices is if they are negative – or if their CFD bid was at too low a strike price, and they have yet to actually commence their CFD as they recoup higher revenue on average by selling at market prices instead. For AR7 the option to delay the commencement of the CFD has been largely removed, with the LCCC now able to decide when the wind farm is effectively complete and commercially operational.

Thank you both for taking the time to provide these explanations. I now understand how both the bidding and day to day charging works

Different wind projects make different bids during the auction.. But the Low Carbon Company and government decides how much budget for estimated subsidies that consumers will have to make available, look at the bids and calculates what the “strike price” needs to be to stay within the budget constraints. Then everyone who bid lower or the same as the “strike price” will get a contract for the “strike price” which is the same for all companies bidding the same thing e.g. offshore wind to be installed in a particular year. That is irrespective of what these project initially bid.

So lets assume the auction “strike price” for the CfD AR7 offshore wind ends up as £91/MWh, announced in December 2025. £91/MWh is what the company bidding £90/MWh will now get. If it had bid £92/MWh it would miss the cut and not get a contract at all.

The £91/MWh is uplifted each year by CPI inflation. Lets assume the uplifted sum is £98/MW by 2028 and all the offshore wind farms bidding in the auction go live in that year.

This bidder will initially be paid the wholesale price for a particular period by the NESO. Lets say on two separate hours in 2028 the average price for wind supplied is £70 and £120. In the £70 hour the wind farm will be given another £28/MWh by the government Low Carbon Company (which recovers the money from consumer electricity bills through the energy suppliers), so ends up with £98/MWh. But in the £120 hour the wind farm will have to repay £22/MWh to the Low Carbon Company and consumers so still ends up with £98.

In other words, the CfD strike price uplifted by CPI inflation of £98/MWh is actually a fixed price contract, though a variable amount of money comes from the NESO and then the Low Carbon Company and the wind farm make payments either way to ensure the fixed price is always received by the wind farm.

There are a couple of twists I haven’t included, so as not to make the explanation more complicated than it already is. But if you take the trouble to understand the above, then that will tell you what happens nearly all the time.

NESO are only involved in the Balancing Mechanism and ancillary services, and in the case of wind farms that is almost exclusively for curtailment payments. Normal sales by wind farms are made either on framework contracts with large consumers or retailers, or via the Day Ahead market either via the auctions that set IMRP where Nordpool and EPEX Spot stand as the counterparty to cleared bids and offers, or via direct third party spot sales often facilitated by brokers. The purchasers are typically retailers or gas generators who use cheap wind offers to meet previous sales made on a forward basis to retailers as hedges demanded by the OFGEM cap. Sometimes they may include traders exporting via interconnectors.

Framework contracts allow wind farms to nominate their expected production close to real time e.g. day ahead, rather than committing to provide a fixed supply, buying in from elsewhere if they are unable to generate sufficiently (which are the normal terms for forward sales by nuclear, gas and biomass). In exchange, the price basis for those with CFDs is usually IMRP based (wind farms on ROCs may opt for a different basis). That allows both purchasers and sellers to adjust positions without risk of losses against market alternatives: e.g. a factory on shutdown can resell power it doesn’t need at the price it is paying for it under the framework contract.

Good information. Thank you.

Thank you both for taking the time to provide these explanations. I now understand how both the bidding and day to day charging works

There is a plan for long duration storage with 8 pumped storage schemes in Scotland and 1 in Wales providing some 5 GW of capacity to the 2.8 GW we have at present. Compare the operational costs of Dinorwig at 1.8 p/KW hour with the operational costs of gas.

The main operational cost for pumped storage is the round trip loss, which averages just under 25% of the cost of electricity purchased for pumping. Of course, margins between purchases and sales have to pay for the costs of financing each scheme and for the rather lower costs of maintenance, and the operations and management teams.

Kathryn is picking worst case on worst case to try to make a case against wind and solar. But most of the decisions are arbitrary – they may convince the anti-green brigade, but not anyone looking at the big picture. The main issues are:-

1). The fact turbine prices went up in an era when steel and copper prices were increasing is not a guarantee they will continue to go up now such commodity prices have reduced. A much more likely outcome is that turbine prices will revert to the mean in constant currency.

2) Kathryn picks 2024 wholesale prices because she knows these are the lowest around. However, the average prices for the 12 months July 2024 through the end of June 2024 are considerably higher. They average £83/MWh from https://electricinsights.co.uk/#/dashboard?period=1-year&start=2024-07-01&&_k=yl9mbo. Allow maybe 2% for 7 months inflation (from an “average 2024” price, and the wholesale price is still over £80/MWh.

3) Kathryn is claiming “proof” by assuming that solar and onshore and offshore wind AR7 CfD strike prices are going to hit the bid cap (“administrative price cap”) ceiling. Of course there is no such certainty, and the most likely outcome is a 20% discount on the bid cap ceiling. One good “political” reason for this is that governments like to have a good tale to tell on how much the competitive CfD auction process for each successive CfD auction has saved on the bid cap price. And there is zero desire to have yet another failed auction. The net of all this is that the bid cap prices are likely to be set higher than lower.

4) It is hardly valid to claim renewables are more expensive just because the contract terms have been extended to 20 years instead of 15 years, with an estimated saving of 12%.

The reason is that there is no means of calculating the wind farm revenue for years 16 through 20 in the absence of a CfD contract. The reason CfD contracts are efficient in reducing wind and solar costs is mainly the revenue certainty they provide.

5) Kathryn’s argument for a 12% uplift on AR7 prices contains the seeds of its own destruction. Let us assume it is true and see what happens. If N is the new AR7 price and W is the wholesale price or power in years 16 through 20, then she is claiming that the revenue under the old CfD 15 year contract of (N / 0.88) x 15 + W x 5 is less than N x 20, which multiplies out to 17N + 5W < 20N.

This leads to the condition that 5W < 3N, In other words, ignoring the effect of revenue certainty, for the new contract to be worthwhile in real terms, the wholesale price in years 16 to 20 must be less than 60% of the strike price for the CfD contract.

And, of course, it doesn't even take account of the fact that the increased revenue in years 16 through 20 has to be discounted by a factor to take account of the fact revenue in 15 years is worth considerably less than revenue earned now, even though all revenue is uplifted by CPI inflation each year. If you factor that in, you get a significantly lower wholesale price for 15 years in the future.

This would surely be good news – it means the 2030 Clean Power plan would succeed in meaningfully bringing down wholesale prices, or at least not increasing it. That is the likely the opposite of what Kathryn is hoping would happen. But it follows inexorably from her assumption that it is a fair comparison to uplift AR7 CFD prices by 12%.

Of course the obvious way out of this dilemma is that Kathryn is wrong, and that it is invalid to pretend that the estimated cost reductions in AR7 strike prices are due to anything more than the increase in the duration of revenue certainty.

I rest my case.

We should all revisit this in December, when the results of the AR7 CfD auction are known.

In the meantime, just remember that there is a lot of cherry picking going on in the article above, plus assumptions that seem to lead to their own destruction once you work the numbers through.

One big picture aspect is that the big prices obtained in AR7 will not reflect the true cost to the consumer because of the need to fund storage and enhanced network stability kit to maintain frequency a high levels of usage of intermittent energy sources. These storage requirements are massive as they have to cope with northern Europe wind droughts. There have been three since winter 2010.

• Big Freeze (Dec 5, 2010 start)

• 2016–17 calm (Dec 5, 2016 start)

• 2021 calm (Sep 1, 2021 start)

The Big Freeze of winter 2010/11 is considered to be a worst-case scenario. My own research of Dukes data shows that the winter 2010/11 had far less wind that 2016/17. The average power factors for 42 days commencing 5 December are circa 0.063 and 0.107 respectively. This compares with the long term average offshore wind factor of circa 0.4

The simulations show that less than 280 GWh of UK battery storage is required to meet most short duration time shifting situations, and it is no longer expensive. In addition you need despatchable backup for the longer duration gaps in wind and solar.

Batteries first.

In the December 2024 PowerChina auction for 16 GWh of BESS capacity, the average bid price was (the equivalent of) $66/kWh. So 280 GWh would be $18.5bn, or £14bn. This is one third of the current capital cost of the new Hinkley Point C nuclear plant, for enough storage for 87 hours of its output. Yes this is real money, but hardly unaffordable.

In terms of the long duration gaps, the NESO has recently contracted all the existing UK CCGT/OCGT gas plants in a T-4 capacity contract (meaning for 2029) for £60-kW year. However, the simulations seem to be predicting another 5 GW would be needed for the 2030 Clean Power grid. The capacity contracts for such new plants could likely be at the same rate, but would need to be for 15 years to be worthwhile. So the total 32 GW of gas plants would be costing around £2bn per year – also real money but not a show stopper.

This solution would cope with lulls in wind power of any duration, including those you listed. After a certain time, the gas plants would be migrated to green hydrogen fuel, produced by electrolysis from surplus wind and solar power, and stored in depleted oil and gas wells of a suitable depth to store 300 atmospheres of hydrogen (so the pressure of the surrounding rock must exceed this at the depth of the storage).

Are you sure about the lull of 5 December 2010 for 42 days? According to https://electricinsights.co.uk/#/dashboard?period=1-month&start=2010-12-04&&_k=y31hsi the average wind generation for the first month was more than half of the average for the whole of the 12 months starting that day. Then the next couple of weeks were above the annual average. It doesn’t look like a worst case to me. There was 5.2 GW of wind installed, of which 1.3 GW was offshore wind, according to the Google AI. So the 1.2 GW average output in the first month is a capacity factor of 22%, rising thereafter to around 40% for the next two weeks.

The December 5th 2016 wind lull seems to have been for just a day – most of the rest of December was above average.

I’m not saying you don’t get such periods, just that December 2010 and December 2021 weren’t one of them. The September 1st 2021 lull for 3 weeks is surely a better example though.

William Thank you for your reply; I wish to respond to your comment about the scale of the wind drought in 2010. I used daily load factor data from Dukes extracted using Chat GPT. The analysis is describe in the link below which also provides a link to the complete ChatGPT dialogue. I accept that Chat GPT could have made a pigs ear of the calculation of the load factors. https://docs.google.com/document/d/1nvEfwOm_3GmL_G_fs3P3-210kLRy4d6kCIPBtSEo3CU/edit?usp=sharing

In terms of numbers I list the average load factors which I manually calculated

Average Load Factor Winter 2010 Winter 2016

November 0.240 0.328

December to January 0.093 0.125

42 day drought 5/12 0.063 0.104

February 0.253 0.287

o

Alan,

It was me, Peter Davies made the comment, but it didn’t post first time, and I may have forgotten to amend the Name field by the third time I was trying it. The web site is supposed to retain the last name posted, but that doesn’t seem to work!

This rwads as though the reply is actually from Peter Davies on a hijacked ID. I recognise numbers he has previously cited. As I have previously pointed out to him Zenobe are investing in three major battery parks in Scotland at a cost of over £300/MWh. If they could do it for $66/MWh they would have cancelled those projects, so I doubt the basis of his claim which is unlikely to be full cost, and might just be an artifact of bankrupt stock clearance following disappointing demand from the EV sector. Lithium prices appear to be rebounding, having moved up from 8.50/kg to over $10/kg in a month.

We wait to see what happens in the next capacity market auction, but my assessment is that the volume to be procured will turn out to be too low, and the requirement for any new generation to be capable of net zero compliance via CCS or hydrogen will mean that no new capacity will be procured, while the lust of soon to be retired plant grows, and will create a crunch and require much higher prices to rectify.

I don’t think anyone is proposing to store hydrogen at 300bar in geological formations. Every project I have studied uses or plans much lower pressures for a variety of reasons. Stublach is planning on an operating range between 30 and 80 bar, whereas their methane storage goes to 100bar in the same salt formation. This matters because it multiplies the volume of storage that must be supplied. Let’s leave aside that hydrogen projects are dropping like flies because they are hopelessly uneconomic, and no-one trusts government to maintain adequate subsidies at consumer expense.

IDAU said “This reads as though the reply is actually from Peter Davies on a hijacked ID. I recognize numbers he has previously cited.”

Absolutely correct – except the ID wasn’t hijacked. I think the server is getting confused. It is supposed to be filling in my ID, not William Birch’s. Is there someone of that name who posts here?

It took me more than one attempt to post, as the firewalls didn’t like something about my configuration. Likely on the second or third attempt I wasn’t that careful about making sure I overwrote the wrong name and email. Sorry about that.

Switching browsers seems to fix the problem.

IDAU said “As I have previously pointed out to him Zenobe are investing in three major battery parks in Scotland at a cost of over £300/MWh. If they could do it for $66/MWh they would have cancelled those projects, so I doubt the basis of his claim which is unlikely to be full cost”

The PowerChina bids were real and for complete BESS systems, but in China. My assumption is we will see similar costs here by 2030 – 5 years out. It does take time for such pricing to percolate through.

IDAU said ” don’t think anyone is proposing to store hydrogen at 300bar in geological formations.”

You are probably right. The UK Rough gas storage used to operate at 250 atmospheres, but they are reluctant to take it so high now. However there are depleted gas wells expected to become hydrogen stores, potentially at over 200 atmospheres. See https://www.sciencedirect.com/science/article/pii/S001623612203856X?via%3Dihub

However, the exact pressure isn’t that important, even though you need higher volume at lower pressure. The UK offshore is swimming with depleted gas wells, and the cost of retrofitting them to store hydrogen isn’t that high. Most of them have residual methane cushion gas which could potentially cause a problem with hydrogen uses requiring pure hydrogen. However, for CCGT/OCGT grid backup the exact mix of hydrogen and methane is not likely to be a big issue.

IDAU said “hydrogen projects are dropping like flies.”

Some are dropping out (e.g. a couple from Fortescue recently). But, as you will be aware, there are a huge number of flies in the world and likewise a large number of hydrogen projects which are not dropping out. Yes government subsidies are required to pass through the Valley of Death to mass market economies of scale, but it is going to happen before too long. New technologies always need subsidies to get them to economy of scale.

I don’t think you should count the US hydrogen projects dropping out. This is just due to Trump political pressure rather than any change of basic economics.

I think you’ll find you are the one cherry-picking data to support your own narrative.

1) Turbine prices increases are not only driven by raw materials costs, they are driven by financing costs, tigher warranties and a desire for higher profitability. OEMs have said so clearly and it is widely believed that these price increases will be maintained.

2) I used 2024 because it is the most recent full year. If anything, prices are expected to fall (and the forward curve is downward sloping). By the end of this year all Russian gas will have been replaced by new LNG and by the end of the decade the global market will be long gas.

3) Since AR7 is explicitly volume maximising tather than cost reducing, the discounts to the ASPs are likely to be smaller. The lack of price tension in this auction would tend to suggest prices will be closer to the ASP than in the past. In any case, why increase the ASP if you don’t think the strikes will increase?

4) I did not say 20-year CfDs make wind more expensive. I said that to compare apples to apples with AR6 (15 years), we need to adjust for duration. That is methodologically correct.

5) Your financial logic is flawed. What you’re actually showing is that the value of the extra five years depends on post-CfD wholesale prices being low, which contradicts the “wind is cheap” narrative. Investors want 20-year contracts precisely because they don’t trust the merchant tail to be strong enough. That doesn’t support your point, it supports mine.

Of course we will wait until the results are out, but I think you have completely missed the point. Turbine cost increases have already shown duration and the fundamentals around OEM profitability indicate they are here to stay. We KNOW this auction lacks price tension, so past discounts of the strive vs ASP are unlikely to hold, and higher ASPs in themselves strongly suggest higher cleared prices

KP said ” Turbine prices increases are not only driven by raw materials costs, they are driven by financing costs, tigher warranties and a desire for higher profitability.”

Financing costs will be a lot less for a turbine than for a wind farm, because the turbine maker will presumably be making all the components for one turbine at roughly the same time, assembling it, delivering it then getting paid for it – all within a window of months. So interest would not be a major factor in the cost as it is likely to apply for only a few months.

But for the wind farm as a whole a lot of preparators costs are required up front – such as contracts to make the foundations, likely in a batch up front. Foundations are then installed well before the turbines are delivered. And even once a turbine is delivered, the wind farm may go through testing for quite a while. This could involve a few years of interest payments.

KP said ” I used 2024 because it is the most recent full year. ”

There is nothing magic about calendar years. The most recent 12 calendar months is surely a much better guide.

KP said “If anything, prices are expected to fall (and the forward curve is downward sloping).

This isn’t being reflected in average wholesale prices for full year 2024 vs the 12 months July 2024 through June 2025. Wholesale prices are still mainly set by natural gas prices. The more the EU squeezes Russian pipeline gas out of EU countries, the higher TTF European gas prices are likely to go.

KP said “3) Since AR7 is explicitly volume maximising rather than cost reducing, the discounts to the ASPs are likely to be smaller. ”

This is surely just a matter of opinion. If the government does some sort of risk analysis of success (which they didn’t on AR5), then you would expect a similar ASP discount to normal ie. a minimum of 20%.

One of us is going to qualify for bragging rights on this in December 2025 or whenever the result is announced.

KP said “I did not say 20-year CfDs make wind more expensive. I said that to compare apples to apples with AR6 (15 years), we need to adjust for duration.

You have never adjusted CfD prices downwards for duration just because ROCs were 20 years and CfDs only 15 years. So for consistency of methodology you shouldn’t do it for a change in duration in CfD contracts either.

In practice, there have been a number of tweaks to CfD contracts along the way to AR7 – all designed to ultimately reduce costs for consumers. These include:-

– No ability to bid negative

– No payment when prices go negative

– No ability to sell wind farm output at merchant prices and defer the CfD contract start, if merchant prices happen to be higher than the CfD strike price.

– Projects will now be allowed to bid even if they don’t have all the necessary regulatory permissions yet. Previously they could not.

And the legal ruling that existing wind farms can’s sue if another wind farm “steals some of their wind”.

Surely the key thing is the costs consumers pay – that is what it is all about. And there isn’t much doubt will lower consumer costs for at least 15 years. Personally I have doubts the reduction will be as much as 12%, because of the logic in my comment above.

KP said “Your financial logic is flawed. What you’re actually showing is that the value of the extra five years depends on post-CfD wholesale prices being low, which contradicts the “wind is cheap” narrative. ”

I have some sympathy for you on this. However, if wholesale prices really are going to be that low in 15 years time, then consumers bills will be that much lower than now – because the wind costs won’t change between then and now. So the government of the time will be able to sell that they have brought bills down.

KP said “Turbine cost increases have already shown duration.”

Over the medium term, larger turbines have always brought down total project costs, because the balance of system costs is then proportionately lower. The trend to larger turbines has continued steadily. AR3 projects initially expected to install with no bigger than 12 MW turbines, but now we are at 16 MW. Again, it is consumer bills which matter, not turbine prices, and it is consumer bills which is your major complaint in this article.

KP said “We KNOW this auction lacks price tension, so past discounts of the [strike price?] vs ASP are unlikely to hold”

The auction is also highly competitive. Compare the zero volume in AR5 and low volume in AR6 with the huge increase in seabed licenses a few years ago. These projects must be coming up to bid time now. All these projects are not only going to want to bid, but also to recover the costs spent so far. So they are more likely to go for reasonable profitability and hope the strike price ends up considerably higher than their bid because of other, higher, bids, than to bid high and risk being shut out.

At a guess I would assume even if Miliband sets budgets for 11 GW of offshore wind at a reasonable price, far more than that (150 to 200%) will be bidding. That is surely a consequence of being allowed to bid before accumulating all the necessary regulatory permissions.

With the high financing costs of wind farms, we have to ask if it were better to get smaller turbines manufactured and the installed individually, such that dead time between purchase and full operation is reduced. Isn’t one of the major problems with wind farms is that we are paying for years of financing, when there is nothing there to produce power?……..What is the financing cost of all that income that the treasury has generated through leases on crown property, that ends up on our electricity bills………paying for land that this country owns, paying the finance cost of that land as well, then put it through the National Grid wringer to get even more costs added into the system, with every step (added cost) having profit margin added every step of the way. Power generator, National Grid, Utility company.

It’s as if the government don’t understand how compounding of costs occurs in supply chains, such that everyone, every vested interest gets their ………10% or 20% or 30%, and the price of goods doubles.

Why do people want to fly direct between regional airports, direct to their destination……..cost and time. Does any government do efficiency?……….Doesn’t look like it!

I guess if we don’t have a system where each farmer is automatically allowed to site one wind turbine within a certain size range, with a minimum distance constraint from local housing, it’s not surprising that planning and consent takes a fortune to do, plus the spacing of turbines to stop wind shadow effects.

Just think, from all the seabed leases, the government is enabling several companies in the supply chain to take profit from the cost of those leases.

A farmer wouldn’t have to pay for their own land, just the turbine and its installation costs.

Of course, if a farmer rents their land to a utility company, it’s no different to seabed leases. Can’t we get some costs out of the system, instead of building more in?……..more costs at each step, and compounding of profit, it’s how things get relatively more expensive, not cheaper.

The elephant in the room is that, howsoever and whysoever the CFD price cap is escalating, it is nonetheless for a technology which features 65% downtime and requires 100% duplication and back-up from reliable sources. Nobody would build this voluntariily any more than they would buy a car that ran less than half the time and requiring a taxi on tickover at the bottom of the drive.

The elephant in the room is that, howsoever and whysoever the CFD price cap is escalating, it is nonetheless for a technology which features 65% random downtime and requires 100% duplication and back-up from reliable sources. Nobody would build this voluntariily any more than they would buy a car that ran less than half the time and required a taxi on tickover at the bottom of the drive.

None of this is true.

The capacity factor of new UK offshore wind is likely to average around 55%, so the “downtime” is less than 45%. That means it will be generating a least a reasonable fraction of its nameplate capacity much of the time. The Dogger Bank windfarms going live soon will likely have a capacity factor averaging 60%, according to the Global Wind Atlas at https://globalwindatlas.info/en/.

Further, you don’t need 100% capacity backup for a few reasons.

1) You only need as much despatchable generation as is required to match the inflexible load peak hour demand.

2) Some loads, such as EAFs (electric arc furnaces) don’t need any backup power at all – they can simply schedule a batch for a time when there will be ample wind and solar to complete the batch.

3) Because there will be up to 50 GW/280 GWh of grid batteries, you can start backup generation in advance of peak hour and before the output is required to meet actual demand, to ensure the batteries are fully charged for peak hour. When wind and solar output is low for an extended period, peak hour demand is then satisfied from the combination of batteries and despatchable generation.

Likely, with sufficient batteries, only 40 GW of despatchable CCGT generation would be needed to meet a 50 GW inflexible demand peak.

RG said “Nobody would build this voluntarily any more than they would buy a car that ran less than half the time and required a taxi on tick over at the bottom of the drive.”

If renewables + batteries + despatchable CCGT are the cheapest solution (including likely future carbon costs for fossil fuel generation) to reliably meet UK variable demand, then that is surely the way to go.

Strange the DESNZ do not agree with you. Their capacity factor assumptions have historically been described by them as being over optimistic in order to prevent any accidental overspend of CFD budgets. For AR6, the assumptions were 62% for offshore wind, 56% for floating wind and 45% for onshore wind. The assumptions have been heavily pruned for AR7, at 49% for offshore, 48% for floating and 36% for onshore.

Dogger Bank A now has 3 operational BMUs. I see no evidence that they are outperforming other nearby wind farms. Perhaps they will in stormy weather, as they are supposed to keep generating in winds of up to 30m/sec, compared with 25-27m/sec for earlier ones. KNMI data suggest such wind speeds only occur a tiny percentage of the time

https://www.knmi.nl/research/observations-data-technology/projects/knw-atlas

There are several factors that may account for the change. Wind theft is now an increasing issue, and likely contributed to the decision to cancel Hornsea 4. Global stilling is also a risk factor. Q1 wind output was almost 10TWh lower than in 2024. There have been repeated messages that we are running out of space in the North Sea and that we will be forced to opt for much more costly floating wind in other areas. Certainly the Crown Estate has gone out of its way, including chipping in a hidden subsidy by offering to take a stake in floating wind, and ensuring the ASP is at a much higher level. Perhaps DESNZ no longer care about subsidy budgets.

There is alot of Hopium about the degree to which demand can be flexed. Last winter the peak contribution from DFS was less than 200MW. If you expect EAFs to operate only on windy days you lack a basic understanding of economics. We would end up saving their entire demand because they would locate elsewhere.

IDAU said “Strange the DESNZ do not agree with you. Their capacity factor assumptions have historically been described by them as being over optimistic in order to prevent any accidental overspend of CFD budgets.”

At one point the CfD budget took a bloodbath when the DESNZ predecessor grossly underestimated the capacity factor of a large offshore wind farm.

I go by the capacity factors on the Global Wind Atlas.

IDAU “For AR6, the assumptions were 62% for offshore wind, 56% for floating wind and 45% for onshore wind. The assumptions have been heavily pruned for AR7, at 49% for offshore, 48% for floating and 36% for onshore.”

I would have thought floating offshore wind should always be bigger than bottom fixed offshore wind. Or there is no point in incurring extra expense at the moment for floating. And 45% is far too high for UK onshore wind in any location other than Remote Island Wind on the Shetlands maybe.

Which ever of the bipolar cycles DESNZ is in, the AR6 projects are not operational yet, so DESNZ has no evidence from AR6 on which to based AR7 capacity factors. So you can’t really trust DESNZ figures which clearly have a large political content.

That is why it makes sense to use the Global Wind Atlas figures.

IDAU said “Dogger Bank A now has 3 operational BMUs.”

Last time I looked at Dogger Bank A it clearly wasn’t properly operational and there were no lessons to be learned from it until the BMUs are fully populated with turbines. The BMRS capacity figures aren’t adjusted frequently enough to tell you the actual capacity of turbines installed until then, so it would be impossible to calculate CFs.

IDAU said “ey are supposed to keep generating in winds of up to 30m/sec, compared with 25-27m/sec for earlier ones. KNMI data suggest such wind speeds only occur a tiny percentage of the time”

I agree. Besides, it is irrelevant. Because if winds are strong enough in one local area to cause turbines to be shut down, everywhere else there is going to be a huge glut of wind nationally.

IDAU said “Wind theft is now an increasing issue, and likely contributed to the decision to cancel Hornsea 4. ” I doubt it. The effect is pretty small in most cases – a few percent. And typically only kicks in for specific wind directions (which could still be the strongest vector on the wind rose, of course)

IDAU said “Global stilling is also a risk factor. Q1 wind output was almost 10TWh lower than in 2024.”

That is surely just the natural variability of weather. If the average is going to change significantly, this will happen over decades, not 12 months. And likely it would just result in the latitude of the strongest winds changing a little. The mechanism for the stronger offshore winds is usually associated with momentum of rising air at the equator, then descending further north and south carrying most of the same speed as at the equator, which results in wind blowing faster than the earth’s rotation, but in the same direction as the earth’s rotation.

IDAU said “There have been repeated messages that we are running out of space in the North Sea.”

I assume you mean space where the depth allows bottom fixed offshore wind to be installed.

By far the best wind is north of Scotland, ideally north west of Scotland, according to the Global Wind Atlas.

IDAU said ” If you expect EAFs to operate only on windy days you lack a basic understanding of economics. ”

Since most days are windy for long enough I doubt that I misunderstand the economics. A simple model for such processes is that output materials costs are 1/3 capital costs, 1/3 power costs, and 1/3 input materials costs. If you can halve power prices by operating only 70% of the time (because solar will help out too and correlates negatively with UK wind), then you should be quids in.

IDAU said “Last winter the peak contribution from DFS was less than 200MW.”

Sure, but the whole demand response and V2G shooting match hasn’t really got going yet. If you look at the Octopus web site info on V2G for instance, you can only enrol if you have either a Nissan Leaf variant (but not mine) and a V2G charger that isn’t made any more, or a new V2G charger that has only been tested with one not very popular brand and model of BEV (not Tesla). Octopus promise to test the new charger with many other BEVs, but it is taking them quite a while.

Most of the domestic use for demand response will be for BEV smart charging or for heat pumps with either batteries (what I am planning) or thermal storage (not really commercially available yet).

In other words domestic demand response will be huge when it comes, but will take a while. Industrial demand response is likely to take off sooner. In the US, pool heaters are a big thing, of course, but not here!

IDAU said “We would end up saving their [EAFs] entire demand because they would locate elsewhere.”

This is highly unlikely. Almost every country regards steel making capability as a strategic facility, such as making steels for nuclear subs or warships, for instance, or turbines for engines for military planes.

It is clear now that Miliband knows exactly what he is doing. He is clearly wishing to sabotage our industrial capability. What I don’t understand is why

Isn’t the whole idea to get away from burning gas not that it is cheaper?

Great work as ever. I think if these figures were spoken about in the msm and Starmer was challenged on the cost to consumers, the impact on jobs and the economy with the follow on impact to services every time he was interviewed this would surely collapse the false claims and Net Zero policy. It’s being interesting watching president Trump slam wind turbines in front of Ursula von der Leyden and no real challenge to that, at least I haven’t seen any.

Von der Leyden can just ignore Trump and just carry on with an EU strategy for reducing fossil fuels using wind power etc.

Anyway, the only reason Trump doesn’t like wind power is NIMBYism – he claims the offshore wind farm off the coast spoils the view from the Trump golf course in Scotland near Aberdeen.

I think you’ll find Trump has expressed several other reasons for being against wind, with the cost of subsidies (which he is cancelling in the US) and the costs of intermittency being at the top of the list. He also sides with the Save the Whales campaigners for the New England offshore area, and is opposed to the high costs of those projects for consumers. Most residential consumers pay less, and most industrial customers do.

https://www.chooseenergy.com/electricity-rates-by-state/

Many projects are being cancelled: Equinor just took a $1bn write down on US wind. It’s instructive to look at the recent US offshore wind prices which had been at or above the AR7 ASP.

You are confusing Trump’s reason for disliking offshore wind with his rationalisations intended to convince others.

There are plenty of articles on the web debunking Trump’s arguments against wind power.

Suffice it to say that red state Texas is huge on onshore wind power, and just as big on solar nowadays, expected to overtake California soon. Not to mention battery storage.

Whales are not at risk from offshore wind farms. The key thing is to ensure that curtains of air bubbles are used to reduce the escaping noise from pile driving foundations.

US offshore wind supply chains are very immature as yet, which is why US offshore wind is costly.

The US president is pretty powerful, though a complete moron who will cost US electricity consumers a lot of money by reverting to fossil fuels. The US won’t be making any progress with offshore wind until he is gone. That won’t stop the rest of us though.

DESNZ/Ofgem can always make renewables cheaper than gas by increasing the carbon tax. The infamous DESNZ ‘Electricity Generation Costs 2023’ document has a carbon tax of £60/MWhr. DESNZ/Ofgem never take into account of course the costs of the necessary national grid upgrades to deliver the renewable electricity from the North Sea or the necessary local grid upgrade from the current 1-2 KW/household (continuously) limit to enable the full electrification of transport and heating. As there is no plan for grid-scale electricity storage it will be necessary to either run a full parallel hydrocarbon system for grid stability and backup or use DSR (aka rolling blackouts) to enable demand to match supply. But the DESNZ/Ofgem argument for renewables has moved on from one of cost, which they know is undefendable, to one of security saying that British wind and sunshine is more secure than gas imported from unreliable petra states, ignoring that North Sea gas is still 50% of our supplies and we then get 30% from Norway and 10% from the USA. Plus of course we still have our own gas if we fracked. On security they also ignore that it is not secure to rely upon China, a state described by our security services as “hostile” for our energy infrastructure (wind turbines, solar panels etc) and the metals and minerals for electrification. Neither is it safe to put all our energy eggs into one energy basket, electrification, making our national and local grids the worlds biggest hacking targets. Or safe from a Carrngton event. Neither is is safe to deindustrialise so we cannot make steel and our own munitions. Nor to spread our energy infrastructure out over half the North Sea and consequently unprotectable from cheap, effective above and below water drones.

PS : And our solar estates are entirely unprotected and could all be taken out overnight by co-ordinated gangs armed with hammers.

I see the wind lovers are trying to knock down Kathryn’s logic and are suggesting that bidders may offer below the cap. Time will tell, but many accepted low bids from the last auction have not materialised, no doubt so they can get more this time. Unfortunately we have another 3 years of auctions before a general election, so plenty of time to pressure Miliband to increase the subsidy even more if he thinks he’s losing his 2030 target.

I think you will find all generating plant (combustion, nuclear) will have increased by a similar if not larger cost [1] (its called Bank of England assisted inflation by keeping interest rates unnecessarily high and inducing austerity). As combustion with fossils is folly considering the state of climate warming except for the last 5% of infill and much of that could be renewable methane/hydrogen, renewables are the way forward. Nuclear will always be too late, too expensive, too dangerous.

[1] (2025 update: we are seeing much higher equipment prices, by as much as 10%, as OEMs are reaching capacity output.) https://gasturbineworld.com/gas-turbine-costs-kw/

As one of those criticising Kathryn’s logic, I am just going to point out to you that the AR6 CfD auction offshore wind strike price was 19% below the cap. See table (F) of the results at https://assets.publishing.service.gov.uk/media/66d6ad7c6eb664e57141db4b/Contracts_for_Difference_Allocation_Round_6_results.pdf.

In fact, I believe that there was only one case of the strike price being at the bid cap price, and that was for solar.

There has been a lot of disruption to offshore wind supply chains caused first by the coronavirus epidemic, and more recently by the war in Ukraine. Like the Borg in Star Trek, offshore wind supply chains can adapt, but it does take time. The government stupidly trying to squeeze offshore wind costs in the AR5 auction didn’t help supply chains either, and it was crass stupidity to set the offshore wind cap below the caps for both solar and onshore wind.

What is really needed is at least a medium quantity of wind capacity (4+ GW) to be contracted now, to pave the way for a much larger quantity in AR8, at a significantly lower price.

If I was Miliband I would push the target date from 2030 to 2031, rather than pay huge subsidies for a single auction when the price is likely to come down to the mean within a couple of years anyway.

The AR6 clearing price turned out to be too low for at least Hornsea 4. I think you are setting a very low bar in calling for just 4GW this time. OEUK have been calling for more than twice as much, and give a rather Delphic comment on the strike prices and prospects for grid connection here

https://oeuk.org.uk/oeuk-responds-to-ar7-strike-prices/

I think Miliband is being unrealistic if he expects manufacturing and installation capacity to be ramped up to meet a self inflicted peak. It would certainly lead to much higher prices, not only to outbid other countries for capacity, but also to provide insurance against a subsequent demand bust post peak.

There are dangers that the offshore ASPs are too low. Being committed to keep operating for 20 years is a contractual risk. At the back end, maintenance costs start to increase and may no longer be justified on the basis of the remaining asset life of other parts of the system. If the price is high enough that risk can be covered, but early years profitability needs to be good enough to create a reserve. It may be that the economic price for a 20 year contract is the same as for a 15 year one, or higher. Also we have bottomed out on the commodity cycle for many key metals, and for some basic availability is uncertain: see Chinese restrictions on rare earth exports. These will only increase in price. Manufacturing in Europe/UK is not getting any cheaper, and CBAM could impose a large import penalty on supplies from China. I admire your optimism, but I do not share it.

IDAU said “The AR6 clearing price turned out to be too low for at least Hornsea 4. I think you are setting a very low bar in calling for just 4GW this time.”

4 GW was in the context that the offshore wind bids were all bumping up against the ASP. Better to ramp more slowly and cheaply rather than fast and more expensive, in times of turmoil if that is the case.

My money is on 7-11 GW of offshore wind at a 20% strike price discount on the ASP. We shall see.

I think Miliband is being unrealistic if he expects manufacturing and installation capacity to be ramped up to meet a self inflicted peak.

There’s no indication European offshore wind installs will stop once the UK 2030 Clean Power target is reached. The Google AI (not fact checked) said:-

“The EU is aiming for a significant expansion of offshore wind capacity, targeting 86-89 GW by 2030, 259-261 GW by 2040, and 356-366 GW by 2050.”

IDAU said “There are dangers that the offshore ASPs are too low. Being committed to keep operating for 20 years is a contractual risk. At the back end, maintenance costs start to increase and may no longer be justified on the basis of the remaining asset life of other parts of the system.”

And yet the Danish government has just been giving out lifetime extensions to some of the early Danish offshore wind farms who requested them. The 165MW Nysted (live 2003) gets another 10 years (to 35 years) and 40MW Middelgrunden (2001) another 25 years (to 50 years?), following the 23MW Samsø extension by 10 years to 35 years. See https://www.windpowermonthly.com/article/1923600/denmark-grants-lifetime-extensions-its-two-oldest-offshore-wind-farms.

The two with 35 years are more or less in line with the FID for Dogger Bank C which says “up to 35 years”.

IDAU said “Also we have bottomed out on the commodity cycle for many key metals, and for some basic availability is uncertain: see Chinese restrictions on rare earth exports.”

Niron Magnetics already has a pilot plant for iron nitride permanent magnets and is expecting to complete a volume production plant by the end of this year. Its iron nitride permanent magnets are cheaper and have superior strength compared to rare earth magnets, at normal operating temperatures. It has been supplying samples for some time. Permanent magnets are the main use for rare earths, but it looks like this use will soon be on the way out. See https://www.nironmagnetics.com/.

And that is just one reason to be optimistic.

Most of the bulk metals used have come down in price recently. Copper can usually be substituted by cheaper and lighter (but higher volume) aluminium as a conductor with a given resistance, except for domestic wiring (due to DIY connection issues). Lithium ion batteries look like they will be replaced within a few years by sodium ion batteries for stationary use (e.g. grid batteries) where weight is not an issue.

It is going against the long term trends to suppose that the green technologies will get more expensive, rather than cheaper.

It seems to me that many of you contributing to this blog GREATLY underestimate the extent and cost of additional infrastructure (balancing and back-up) that will be required to support even a small penetration from wind and solar which currently contribute less than 6% of UK primary energy use. (the latest DUKES figures for 2024 are due any minute but they won’t have changed much from 2023).

I should add… that 6% wind and solar hasn’t actually achieved anything. All we’ve done is exported our emissions to places like China because high energy (and other) costs are driving our manufacturing broad.

Hang on! Of course, we have successfully wrecked thousands of square miles of precious landscapes, if that can be described as an achievement. You should be proud!!.

I think the big picture people are really looking at is of having the “green” approved low carbon – with its disproportionate added costs of extra electricity transmission and energy backup (gas powered or energy storage) added to their bills.

The cheapest form of energy storage is high temperature thermal – coming in at under £5/KWh (£5m/GWh); this technology (adaptable from the steel industry) could be directly swapped into gas turbine based generators so, for example a 1GW gas powered plant (coming in at about £1b) would require (nominally) 100 hours of storage (for £0.5B) . So any stranded assets (by dash from gas) would still have value.

And improvements using closed cycle inert gas (argon or nitrogen) could only improve the performance and cost of the gas turbine component.

Hydrogen fuelled turbines still need to be developed (https://www.sciencedirect.com/science/article/pii/S0360319924023681 – “A techno-economic analysis of future hydrogen reconversion”. And, as Kathyrn has pointed out elsewhere, gas turbines, and associated steam turbines, have maintenance issues if used intermittently and sparingly

The government seems to have redefined LDES (long duration energy storage) to be for 4 hours! – certainly they are not worried about the vagaries of weather around the British Isles (which can result in days of windpower at < 10%) – and potential future blackouts.

As regards short term energy storage (batteries) at £200/KWh so a 1 MW Wind turbine (costing £1m) would cost an extra £200k – for an hours worth of storage – which would help smooth supply – and perhaps could be integrated into offshore wind power islands?

Interestingly I looked back at the government performance over the years. The best UK build was 8 years, I believe – with the "greens" saying it would never be built in time– yet wind-power still seems to lack the storage or backup – without relying on expensive batteries or gas fired generation.

I must admit that I think that energy storage could benefit investors in gas fired generation – by providing security of investment – but would require guarantees of regular consumption or appropriate constraint payments for any stored energy used.

So I believe Kathryn's arguments are very likely correct but I think that the issues of wind intermittency and security of supply are relevant to me (and the belief that there is a "green" idea of wind power and batteries being the (only?) desired solution – without too much thought about affordability

Household energy bills are dominated by the cost of gas, which is still 3 times the cost before Russia invaded Ukraine. During winter peaks, the Grid will normaly use the 2.8 GW of storage from the four 50 year old pumped storage hydro (PSH) schemes that paid for themselves after about 10 years and now have operating costs of 1.8p/KWH. After that the only option is gas turbines. For long-duration storage, various studies have shown that PSH is the least cost option. Nine schemes have planning permission but await a cap and floor scheme to attract investors. In addition there are some 20 locations where abandoned quarries and closed open cast coal mines below hills could provide new schemes of 7GW capacity in depressed areas providing technical and semi-technical jobs. At the same time batteries, and particularly vanadium and sodium iron batteries are becoming cheaper. In the long term, this will prove a less expensive option than importing LNG.

We are in danger of forgetting that the point of all this expensive upheaval is to reach zero emissions from electricity production.

To achieve this almost no gas can be run as backup. To have a plan that requires 30-40 GW of gas backup and to rarely use it is economic and engineering nonsense.

To match gaps in wind and solar by substancial (50% or more) demand flexibility (rationing) makes engineering sense but is economic, cultural and political madness.

To fill these gaps with only 280 GWh of battery backup is wishfull thinking. Some simple sums matching max and min wind and solar output with max and min customer requirements shows that the day to day storage requirement is at least 1500 GWh. If interseasonal storage is required it is many times greater. The cost of that is at GDP levels.

We are not looking for the cheapest solution but one that achieves zero emissions at optimal cost. The cheapest solution is irrelevant – 100% gas is the cheapest. Using gas as backup will also reduce a solutions cost but will not produce zero emissions.

RM said “To achieve this almost no gas can be run as backup. To have a plan that requires 30-40 GW of gas backup and to rarely use it is economic and engineering nonsense.”

The NESO modelling shows 5% supply from backup gas for the 2030 Clean Power grid.

Since you need such backup for weather-dependent wind and solar, it is hardly nonsense to provide it. The question is of economics.

We now know the cost. The recent NESO T-4 capacity contract (i.e. for 2029) was for £60/kW-year, so 33 GW of gas backup capacity would cost £2.1bn per year – not insignificant, but hardly a showstopper either.

RM said “To match gaps in wind and solar by substantial (50% or more) demand flexibility (rationing) makes engineering sense but is economic, cultural and political madness.”

BEV charging, with 100% of BEVs on the UK roads, will eventually add 40% to 2019 UK electricity demand. Heat pumps to replace gas boilers might add another 70%.

But a BEV with 300 mile range and a typical 30 mile daily round trip commute has 7 days of flexibility in when it can be smart charged, though some vehicles must be charge more regularly or immediately if on a long journey.

Heat pumps can be supplemented with a domestic battery, to avoid drawing power at the normal evening peak times caused by the existing, inflexible loads. Something like 10-12 kWh of battery storage would be enough to run heat pumps off the cheapest power available within any 24 hour period.

50% demand response across all loads would be a tough ask, but it may well end up 30% of the new loads are very suitable for demand response, without anyone really finding any huge downsides.

RM said “To fill these gaps with only 280 GWh of battery backup is wishful thinking. ”

No one is proposing a single tier storage solution of just 280 GWh of batteries. But what you would probably find from the modelling is that 280 GWh of batteries and an appropriate quantity of demand response would fill in 70 to 80% of the gaps (by GWh) in supply from wind and solar. That would leave only 20-30% of gaps by GWh to be filled by long-duration backup e.g. natural gas fueled CCGT in the 2030 Clean Power solution and green hydrogen fueled CCGT in a successor net zero UK grid.

RM said “The day to day storage requirement is at least 1500 GWh. If inter-seasonal storage is required it is many times greater.”

300 GWh of batteries fills most of the short duration gaps. 1500 GWh/24 hour in a day is 60 GW average demand not satisfied. But the aim of batteries is not to fill all gaps in demand – just most of them.

Interseason storage, such as green hydrogen storage, would indeed need to be in the range of 30-60 TWh, which is around 20 x the storage volume of the UK “Rough” natural gas storage when it was at its maximum volume in the past. UK has a lot of depleted oil and gas wells, and this is not an infeasibly large volume.

Our current PSH has a storage capacity of under 30Gwh. If I’ve read it right The Royal Society in their Sept 2023 report estimated that we would need at least 60Twh to support a doubling of current electricity demand (to around 40% of UK primary energy consumption) with a heavy reliance on wind and solar. That’s current PSH times 2000!

SD said “a doubling of current electricity demand (to around 40% of UK primary energy consumption)”

It doesn’t work like that. Now that UK power generation has dropped from top to 4th emitting sector, two of the biggest emitting sectors are road transport and building space and heating.

However, electrifying both of these improves their efficiency by around a factor of x3, as follows.

For road transport, most petrol vehicles are at best 25-30% efficient, while a BEV is around 85-90% efficient. Diesels can get above 40% efficient. Converting road transport from petrol and diesel to pure battery electric will reduce the primary energy needed for road transport by 60-65%

Similarly, a heat pump used for building heating has a COP (coefficient of performance = efficiency) of x3 or x4 – in other words it is 300 to 400% efficient. You put in 1 unit of electricity to drive it, and it moves 3 or 4 units of heat from a source at ambient temperature (for an air source heat pump) into a building, at a temperature of 50 to 55 degrees C. For once, you are on the right side of the laws of thermodynamics.

Similarly, electrified industrial processes tend to be far more efficient in total energy use than those driven from fossil fuels (where most of the primary energy applied tends to disappear up the chimney).

A summary of all this is that, if UK electrifies enough uses of energy to double grid use, then electricity will become 80 to 90% of the primary energy used by the UK.

SD said “The Royal Society in their Sept 2023 report estimated that we would need at least 60TWh [of long duration storage] to support a doubling of current electricity demand”.

Something like that. The NESO simulations are showing gas backup will be around 5% of supply in the 2030 Clean Power grid. Current UK electricity demand is around 300 TWh/year, so 5% would be 15 TWh. Double the size of the grid and that crudely makes it 30 TWh. Assume a further doubling for infrequent but very long gaps in wind and solar output, in very exceptional years, and you get 60 TWh of long duration (often described as “seasonal”) storage. So one assumption might be that the energy is mainly stored in summer, but mainly has to be used in winter.

60 TWh isn’t impossible. The Norwegian hydro system stores 88 TWh in lakes behind dams, for instance. In the case of the UK the front runner long duration storage would be green hydrogen, produced by electrolysis using surplus wind and solar power. It could be stored in depleted oil and gas wells, then used in backup CCGT plants with burners modified to be suitable for hydrogen.

Although the power to gas to power round trip is no more efficient than 45%, if only 5% of supply is from long-duration backup, then the losses are 5%/0.45 – 5% = 6.2%.

You would need a volume of hydrogen storage of around 20x the current UK Rough natural gas storage for such a backup use, but UK has many depleted oil and gas wells. “It Doesn’t Add Up” has pointed out that projects tend to use a lower hydrogen pressure for such storage than they do natural gas pressure, so that assumes 150 atmospheres pressure rather then 300 atmospheres. In its heyday, Rough was operated at 250 atmospheres.

It is all feasible though, both technically and economically. You might need around 280-300 GWh of grid batteries to get backup CCGT use down to 5% of supply.

I think you have a new record for the ratio between the length of your reply and the comment to which you are replying. You really should establish your own blog where you could develop your thoughts at any length you thought might attract readership: you could link to your articles and stand a better chance of engagement.

I’ll admit your habit of ever longer spam posts dragging in ever more peripheral items has led me to judge that few if any will read them, and therefore there is no point in debating your often highly spurious claims when your previous claim has already been shown to have dubious foundations.

I am grateful to Dave for taking the time and trouble to comment based on real professional knowledge on the prospect for subsea hydrogen storage from a technical angle. It is time you acknowledged that there are people with far more expertise than you.

There isn’t much to be gained by a conversation consisting of you saying “green energy costs money” [with no or fallacious evidence supporting the statement] “no it doesn’t” “yes it does” “no it doesn’t” “yes it does”.

The fact is that it takes more words to rebut a fallacious statement than it does to make it in the first place.

I agree not everyone who subscribes here is going to be interested in changing their mind based on detailed evidence, rather than just going with the echo chamber flow. But some will, and that is enough.

I quite agree, I’ve been very interested in the comments from everyone, from all the different perspectives. Filling gaps in my knowledge and being thought provoking as well.

With Carbon Capture and Storage, against Hydrogen Storage, one has to wonder how one is more feasible than the other. Surely dealing with the explosive nature of hydrogen and the inert nature of CO2, and the leakiness of H2 compared with CO2, that if we expect CO2 to be able to be stored, there must be some conditions under which H2 can also be stored that might be more demanding….. choose your well carefully, from all aspects of seabed to reservoir geology, and the challenges of materials selection, but if it can work, don’t we overcome some of the economic challenges? And like space exploration, the possible technology spin-offs and possible new business opportunities could be enormous.

With Hydrogen, it might not eventually be used for everything, but what if it finds a niche that supports many jobs and careers? What if, like drilling test wells for oil, the old wells need to be tested for hydrogen storage and well permeability? Not an assumption that it’s impossible. What if the seabed around the wellhead needs a bit of re-engineering with a cap, or new sealants around the metal/plastic/alloy bore need to be tested and developed. Or not a single pipe system but something more complex such as a lined pipe, with different materials on the inside and outside, or even a triple layered pipe with three different materials, a metal layer sandwiched between two plastic layers. Or what if there is a new material such as Niron being used for something unrelated that actually has better hydrogen stability, lower permeability/reactivity, non-brittling than any previously know material?

It’s the technical challenges that make it all so interesting.

Peter, even under your scenario of doubled electricity demand to match doubled wind output the frequency and extent of periods of over-supply and under-supply will be greatly increased meaning much more requirement for storage. I’m running with the Royal Society analysis for the moment.

Peter, sorry my last post may not have made a lot of sense. However I was interested in some of the points raised in your response to my original post.

I understand your reasoning which leads you to say 90% of UK energy could be catered for with just a doubling of current electricity generation. However, I question whether your improvement in efficiency ratios in heating and transport can be achieved by a switch to electricity generated largely by wind/solar bearing in mind the inefficiency of generation reliant on so much additional infrastructure plus the energy losses incurred in the storage and conversion processes.

And even if 60Twh of storage is feasible I suggest it will be a) many decades before it is in place and b) incredibly expensive. Meanwhile the gap between maximum wind output and low demand at 3am on a windy winter’s morning will greatly increase, as will the reverse gap when the wind doesn’t blow and the sun doesn’t shine at 6pm on a frosty evening.

SSE have managed to get the Scottish government to race through planning permission for their giant 4.1GW Berwick Bank project that would connect to Dunbar (near Torness nuclear) and Blyth (in competition with or for export via North Sea Link, and South of the B6 major constraint boundary). It will be the 800lb gorilla in the AR7 auction which SSE announced they hope to use to secure a CFD, so I guess they are happy to proceed on the basis of the ASPs announced. It is rather hard to get any useful information on what they think it might cost, and the FID is in the future so they don’t entirely know themselves. But in 50+m water depth you have to suspect it would be closer to East Anglia Project Two’s £4bn/GW than Inchcape (mainly supplied ex China) £3.2bn/GW. They won’t benefit from the Crown Estate equity injection being offered for floating wind, and the Clean Industry Bonus is worth a derisory £27m/GW.

A couple of comments.