In the past few years, we have been repeatedly told by the system operator, now known as NESO (National Energy System Operator) that the GB power grid can be underpinned by a combination of renewables (wind and solar) and imports from other countries. NESO and its predecessor organisations have been a huge cheerleader for interconnectors. The Department for Energy Security and Net Zero (“DESNZ”) is on the same page. The idea is that when wind and solar output are low in Britain, the shortfall can be largely made up with imports.

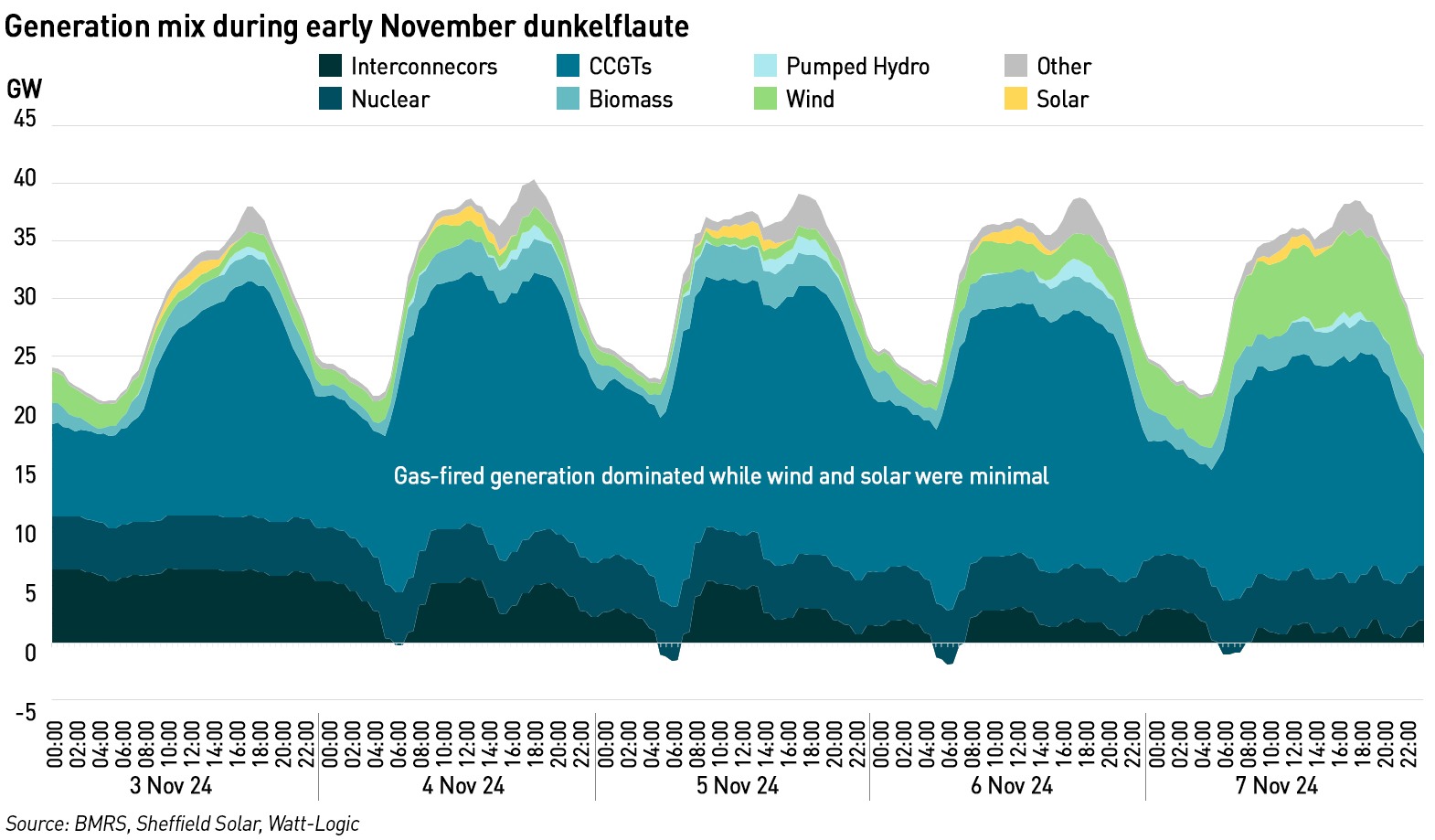

As I have described previously, there are some significant problems with this assumption, primarily the high weather correlation we have with our connected markets which means that they may also experience shortages of weather-based renewable generation at the same time that we do – this was the case in early November when Britain and many of its neighbours experienced dunkelflaute – dull, still weather which is terrible for wind and solar generation.

Another key problem is that exporting electricity in general causes electricity prices in the exporting country to rise. Ofgem has said that once GB becomes a net exporter of electricity, there will be a consumer dis-benefit and as a result it has rejected almost all of the proposed new interconnector projects with Continental Europe in Window 3 of the Cap and Floor regime.

The problems go further than this. The contribution of both renewable generation and interconnectors to meeting demand in GB is often lower than advertised.

Wind load factors are low and are not rising

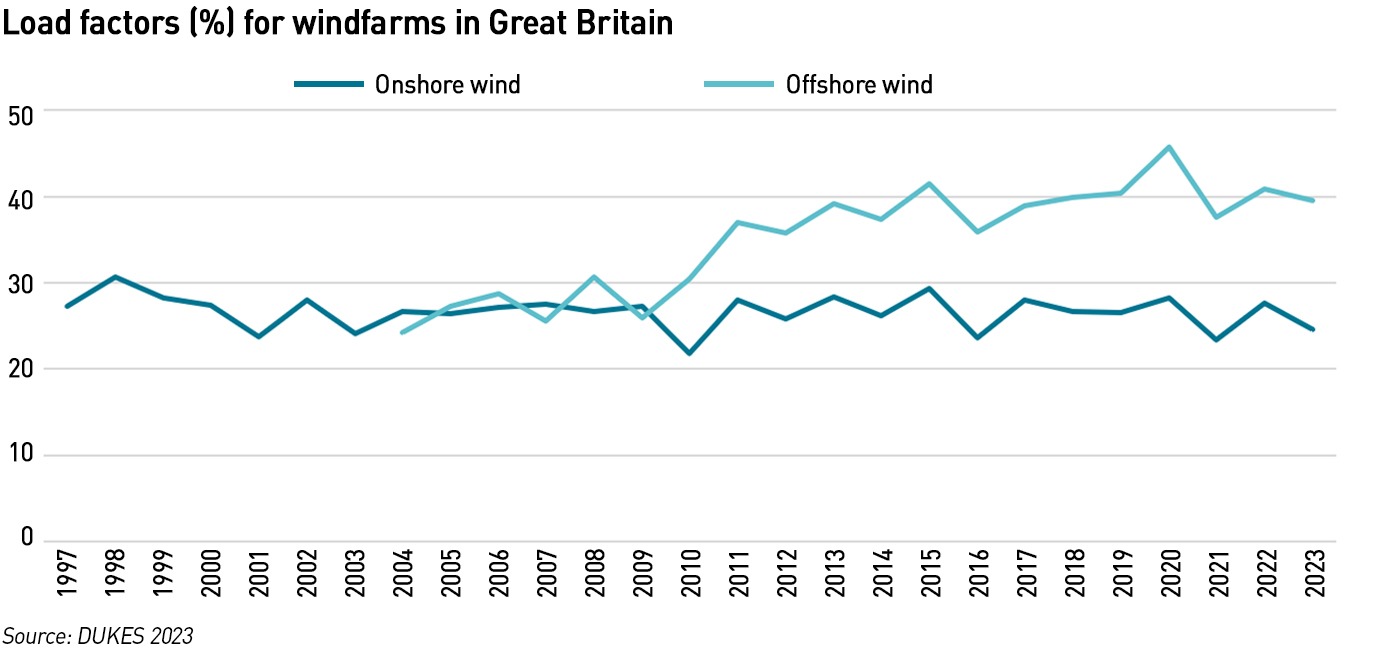

In its Energy Generation Costs 2023 report, DESNZ claims that the load factors for offshore wind will be 61% in 2025 and higher in future years. This is in direct conflict with other Government figures quoted in the Digest of UK Energy (“DUKES”) reports which show that offshore wind has a load factor of around 40%.

However a lot depends on what is understood by “load factor”. Some analysts look at the output of the windfarm at the asset level and define the load factor as the amount of electricity generated per unit of capacity. So if a 10 MW wind turbine produces electricity 35% of the time it would have a load factor of 35% and generate, on average, 3.5 MWh/h. However, what matters to consumers is not how much electricity a wind turbine generates, but how much of that electricity is delivered to them (or to the grid more generally). This is a lower figure because Britain lacks the grid infrastructure to efficiently utilise this electricity, so often wind turbines are forced to curtail – ie reduce – their output. Analysis of the actual contribution of wind to demand illustrates this.

I analysed the contribution of wind to meeting demand from the start of 2024 to the end of November, using data from BMRS. Assuming 6.5 GW of embedded wind (as set out in NESO’s Winter Outlook), and a total amount of installed offshore wind of 30.163 GW (which was the year-end capacity quoted in DUKES 2023 – clearly more has been added during 2024 but using the figure for the end of 2023 would be conservative for the purposes of this calculation), I found that the amount of transmission-connected wind meeting demand in 2024 was just 30% of nameplate capacity.

In September, Net Zero Watch wrote to DESNZ requesting an explanation for the 61% figure used in its Energy Generation Costs 2023 report. A response was finally received in mid-November after the matter was raised in a House of Lords debate, in which the following explanation was offered:

“To enable comparison across technology classes it is standard for LCOE estimates to be calculated assuming that they operate at their technical maximum. This differs from actual annual operation that accounts for all reasons for wind plants to be operating at less than maximum capacity. This will include periods of maintenance and curtailment for example, which varies across years and across projects. Another factor is that the Generation Costs Report considers new turbines where improvements in turbine design and larger turbines (higher hub height) enable increases in load factors. Hence, we expect a higher load factor for the newer models assumed in the Generation Costs Report than for the range of turbines in the existing fleet that you refer to in your letter,”

– Jenny Inwood, Energy Infrastructure and Markets Analysis Team, DESNZ

Oh dear! There is so much wrong with the explanation.

Firstly, suggesting that the technical maximum must be used to allow for technological comparisons is nonsense – what matters, particularly in the context of costs to consumers, is what the technology ACTUALLY produces, not its technical maximum.

Secondly, as Net Zero Watch points out, Levelised Cost is supposed to denote the lifetime cost of the generation divided by the lifetime amount of generation. By using the technical maximum, DESNZ assumes the windfarms always produce at their maximum level which is clearly nonsense and counter to the definition of “levelised cost” in the first place.

Thirdly, the idea that larger wind turbines will be developed producing greater load factors is highly speculative – the trend for larger turbines has stalled in the face of significant warranty issues faced by turbine manufacturers as larger turbines fail to perform. This difficulty is easy to understand – the larger a turbine, the greater the distance between the tips of the blades and the higher the chance they will experience different wind speeds. These different speeds impose significant stresses on the blades causing them and their mountings to fail. Although some larger turbines are being developed in China, Western OEMs are shying away from increasing turbine size, so a conservative approach would be to wait to see signs of this changing and not simply assuming that it will.

Net Zero Watch has pointed some of these errors out to DESNZ and awaits a response.

Interconnector availability is lower than expected and falls with age

The problems I have previously described regarding reliance on interconnectors relate to the availability of electricity for exports to GB, or the desire of exporting countries to continue to export. But there’s another factor in play and that is the reliability of the interconnectors themselves. And they are also interesting to consider.

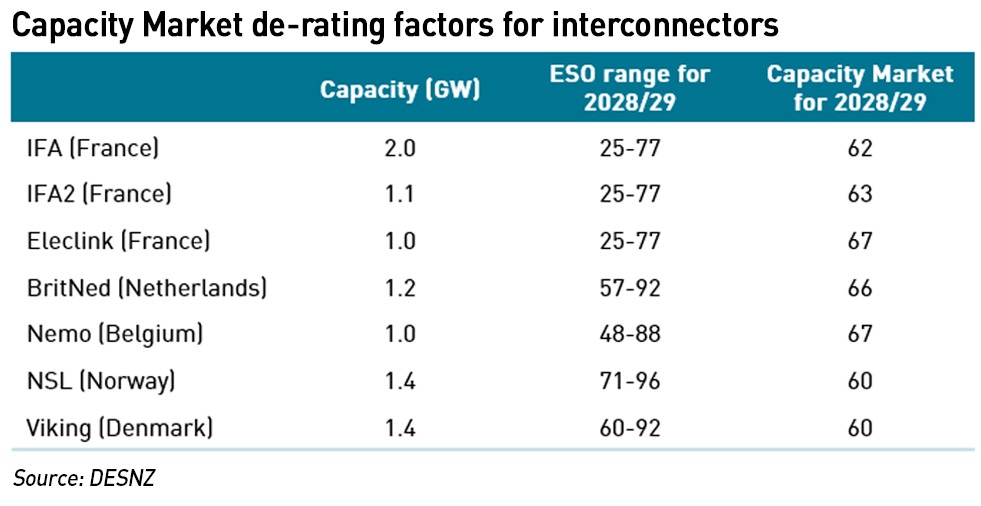

The table below shows the de-rating factors for interconnectors in the next capacity auction. There is the range which ESO (now NESO) suggests, and the values chosen by DESNZ for the auction. The Capacity Market de-rating factors for interconnectors take account of both the physical capacity of the cables and the availability of spare generation in the connected markets for export to GB.

It’s particularly interesting to look at the values for IFA and IFA2 which are virtually identical despite IFA being many decades older than its newer cousin, and being actually available a lot less. It’s reasonable to assume that the spare generation parameters for both are the same since they originate in the exact same place in France, so the difference in de-rating factors should reflect the difference in physical availability, but this does not appear to be the case.

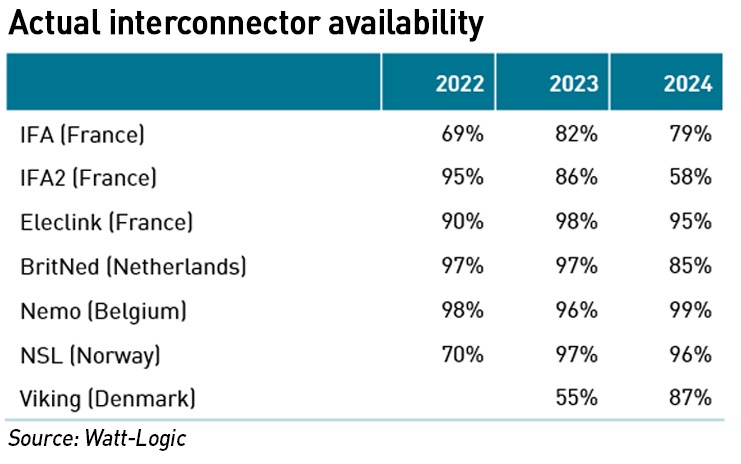

I analysed REMIT availability data for all GB-connected interconnectors (excluding Ireland which I consider to be an additional source of demand on the GB grid) over the past three years. These data are difficult to find since the interconnectors can choose where to report their REMIT notices and can also change as Eleclink has done in the past year. So some of these interconnectors report to Elexon (BMRS) and some to NordPool. ENSTOE also has data but they are not always consistent with the other two which are the ones I relied on for this analysis.

As an aside, I have asked Ofgem to consider requiring all GB-connected interconnectors to report their availability to Elexon, a request I understand Elexon has also made, in order to improve the transparency of market data relating to the GB market. It would also be good if Elexon would report availability data in percentage terms, since extracting the data for my analysis was very time-consuming. I would have liked to go back further but the data gathering simply takes too long. If any of my readers have these data and are willing to share, I would be happy to update this post to include them.

The table shows the percentage of capacity that was available ie not reported as unavailable on REMIT, for each interconnector.

Of course, selected years can be affected by specific improvement works for example, a synchronous condenser is being built at the Sellindge connection point for the French interconnectors, which has led to reduced availability over the past year as various cables must be disconnected while the equipment is tested. And in its first months of operation, the capacity on Viking was restricted by half due to constraints on the Danish grid.

However, it is clear that IFA has much lower availability than IFA2, which is to be expected, given its greater age, so it is difficult to understand why its Capacity Market de-rating factor is just 1% lower than that of the newer IFA2.

Two other things jump out from these data. The first is just how variable some of the interconnectors have been over the past three years. While some of this may be due to projects such as the synchronous condenser at Sellindge which should improve overall availability, it seems that there are always ad hoc “issues” affecting flows.

In 2016 a ship’s anchor severed half of the eight cables making up IFA, putting them out of action for over a year. Around the same time a large part of the French nuclear fleet was offline for inspections as a result of the discovery of the steel carbonisation fraud. In 2022 large parts of the French nuclear fleet went offline again as a result of the stress-corrosion problem. In each case, France went from being a net power exporter, to an importer, changing the balance of flows to and from GB. This suggests it would be unreasonable to discount apparent “one-off” disruptions, since these “one-offs” occur with some regularity.

Another thing which jumps out is the narrow range of de-rating factors determined by DESNZ for the Capacity Market. Despite the differing ages of the links and the market differences, and the very wide range supplied by ESO, DESNZ determined all interconnectors should be de-rated at roughly two thirds of their nameplate capacity. This feels more like a rule of thumb than something scientific. Of course, the Capacity Market should indicate availability in times of system stress and not average availability. It is quite likely that system stress would coincide with both ad hoc availability problems and limited spare generation capacity in the connected markets eg a widespread dunkelflaute.

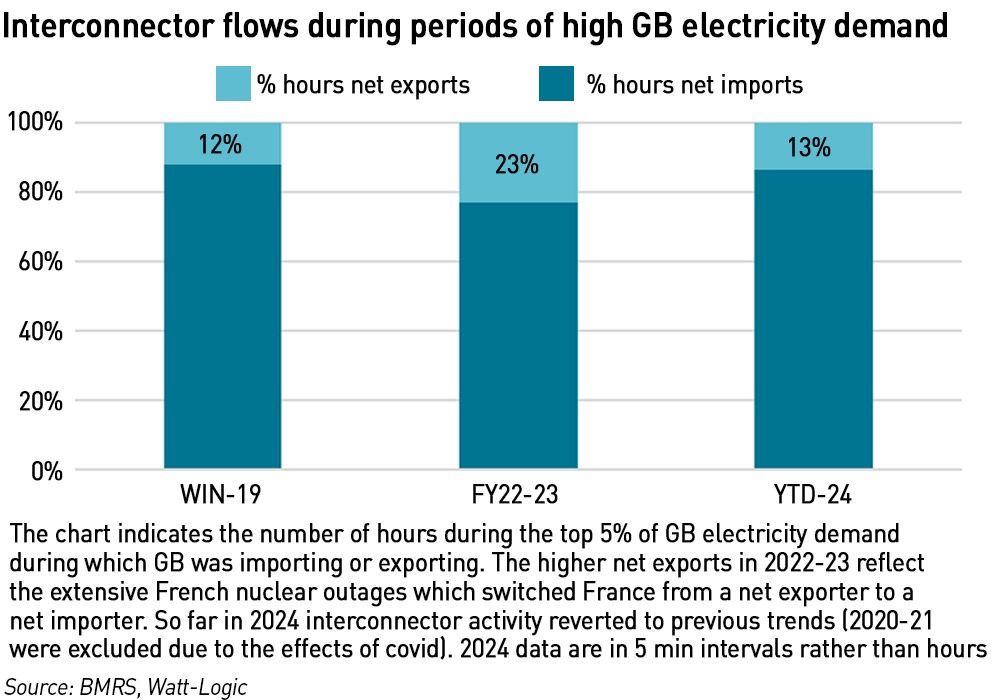

Trying to model spare generation capacity across the European markets is beyond what I have time for, but I have looked at the extent to which GB exports during times of high GB system demand.

When I looked at this in 2019 I found that GB exports during 12% of the hours with the top 5% of demand. In 2022-23 this rose to 23%, reflecting the extensive French nuclear outages which saw France switch from being a net electricity exporter to a net importer. So far in 2024 (using 5-minute data rather than hourly), the frequency of exports during the periods of highest demand has been more consistent with Winter 2019 at 13%. (2020 and 2021 have not been analysed due to the impact of covid on demand.)

In order for interconnectors to genuinely support security of supply it would be better if exports during periods of high demand were minimal, but 13% of the time is almost the equivalent of one day per week (14%) which is not insignificant.

.

So what does all of this mean? Clearly both renewables and interconnectors contribute less than the Government would like us to believe, and in the case of interconnectors, even Ofgem has warned that being an electricity exporter is not good for consumers. Perhaps the countries that currently export to us will realise this as well and reduce their enthusiasm for cross-border trading.

The approach to renewables is arguably worse. Overstating load factors benefits no-one since the contribution to the grid cannot be faked – either windfarms are generating electricity or they are not. If they are not, other generation or imports need to fill the gap. Expecting windfarms to contribute twice as much as they actually are means these other supplies may not be procured in the required quantities, threatening security of supply.

It also means that the cost of windfarms is higher per unit of electricity generated than the Government would have us believe. If they are only running half as much as advertised, the capital cost of the electricity they generate doubles. This translates into poor value for consumers, undermining the “cheap renewables” narrative still further.

It’s ironic that the term for the psychological manipulation of people to make them believe something they would otherwise think is false is known as “gaslighting”, since these failures mean we will continue to rely on actual gas for lighting for many years to come.

Greg Jackson closed down a critic on renewables recently on Question Time suggesting that ‘EV batteries can store enough electricity to power an average home for the best part of a week’ and ‘we have distributed storage that can last us days on end without wind’

https://www.youtube.com/watch?v=TJQU5ATZPt8

Id be interested in your thoughts on that statement. Im not sure the technology is available as yet to make this breathe, but in principle what would you say on this?

Your answers await at this link, hot off the press today.

https://open.substack.com/pub/chrisbond/p/im-sorry-they-havent-a-clue?r=om40y&utm_campaign=post&utm_medium=web

Jackson is of course being highly disingenuous. He is taking the OFGEM value for the purposes of estimating their “cap” bill, which is now down as low as 2,700kWh/year, or ~54kWh/week. He ignores the fact that consumer demand is in fact highly seasonal, being about twice the level in a peak winter month in a colder year compared with the summer. Within that, demand definitely peaks higher still on a cold working day (demand is lower at weekends). Next, he is actually assuming that the only purpose of the car is as a battery, rather than being used: using it will of course add very substantially to demand, probably doubling household consumption (~8,000 miles at 3 miles/kWh). Add in a heat pump and you can more than double that again.

In reality, only a limited portion of battery capacity is going to be made available by EV owners on average, and many households simply won’t afford an EV in the first place. The result is that the maximum storage capacity available will be well under a day’s demand at current levels. Remember that despite the efforts to close down industry and jobs generally, domestic demand is only around a third of the total currently. The result is that it is virtually useless for covering any protracted period of Dunkelflaue, and requires substantial bribes to be paid to EV owners to compensate them for loss of convenience and extra degradation of battery life: many will in any case be driving home from work precisely when demand is highest during the rush hour, and thus be unavailable to contribute. Any use of batteries to top up the grid requires that they be topped up on top of normal demand later. There is no guarantee that a period of insufficient supply is rapidly followed by a period of glut to permit recharging to take place.

A final difficulty is familiar to those in e.g. South Australia, where high volumes of domestic solar generation cause considerable problems for the the grid, risking stability. From the point of view of the grid, EV batteries look much the same as domestic solar. The grid is not designed to be supplied from domestic surpluses, risking local cable and transformer overloads and overvoltages that can damage equipment on the grid and in the home. Moreover, such sources offer no grid inertia essential to maintaining frequency stability: they simply follow the frequency that the grid is operating at in order to maintain synchronisation. They crowd out sources that can provide inertia. Failure to keep frequency under control leads to blackouts.

CF :

In order for evs, heat pumps and ToUTs to work it will first be necessary to upgrade all the country’s local grids.

The engineer Steve Broderick’s report to Parliament on evs said that because local grids cannot handle more than 1-2KW per household continuously only 1 in 7 households could have an ev. The loads for heat pumps, and the much touted cheap energy through ToUTS will be even greater and therefore impossible without local grid upgrade:

https://committees.parliament.uk/writtenevidence/82722/html/

https://www.researchgate.net/publication/342638856_Electric_Vehicle_and_LCT_Loads_on_Constrained_Distribution_Networks_An_Investigation_of_Impacts_and_Options

I do find the whole GB strategy for net zero quite facile and containing some real howlers.

Firstly Net Zero is a Global Goal. Despite popular opinion you CANNOT translate this directly into a series of national Net Zero goals and expect to reach Global Net Zero because it seems to make some kind of logical sense. This is like saying we should have net zero strategies in every neighbourhood and when we gross them all up we have national net zero. A ridiculous approach. Two basic questions from the outset – 1) Where does 80% of the problem lie in the world. & 2) Who has got all of the money?

Two questions that have been generally avoided, partly because we all know the answers but mostly because it focusses action and holds key nations and Governments to account. It forces the hand of collaboration and negotiation and it takes many countries into difficult conversations but it drives enduring meaningful solutions without losing more time and money on flag waving and solution avoidance.

Britain net zero cost total over the next 20 years – £650Bn. That includes generation plant, transmission and distribution to provide upgrades necessary to support EV’s , heat pumps, solar and battery storage and includes the capital costs of replacing domestic gas heating.

Effect of Britain Net Zero on rising global temperatures? – Negligible.

Has mankind thrown itself a challenge that we can’t afford to achieve a goal we know we will miss? . Has this only now happened because we turned a blind eye to previous opportunities to solve the challenge when the investment wasn’t so large over such a short period and the goal was more achievable? Most likely.

So, I’m not arguing we give up, Im arguing we play it smarter and stop firing down a track that will not achieve the aim of the game and will falter in any event but will stop before getting there due to a lack of funds.

Im arguing that we go back and answer the two basic questions. We target the high emitting nations as a collective. We pool our resources and focus our efforts internationally on solving the Global Net Zero challenge starting with the parts of the world that create the most. Might this also be an opportunity to mend bridges, build new partnerships, come together with common enemies and develop international relations into a better place. So much distrust that can be overcome with the offer of a hand to achieve something everyone benefits from.

I don’t even see this as a matter of opinion. I see it is as common sense and history, fact and numbers tell me that without it we will continue to invest in things that disappoint, our credit rating suffers, we become increasingly committed to a destined journey where we don’t achieve our goals and we need to invent trophies and nights out in London to pretend like we have and tell ourselves its not all for nothing. Meanwhile temperatures continue to rise.

Britain Net Zero rolls off tongues daily. Its the accepted sensible, morally correct goal. But when you ask the more searching question as to what impact this achievement will have on the ultimate aim of global temperatures and you ask about the cost and if there is enough money in the next two lifetimes that can be generated to achieve it.. there are fewer prepared to answer it.

The unquestionable following, lack of scrutiny and critical thinking is a concerning aspect of Net Zero. The response to the basic questions is only ever to close down the questioner as a climate denier. As there is no place to go to save face outside of that.

Climate change is real, the data is there. The effects of climate change is real, the data is there. To avoid devastation to established communities and avoid further disruptive mass migration across the planet, action is required (and has been required for some time). The intentions of many are commendable, the problem is well understood. The bulk of the actions however seem misguided, misplaced and not helping with progress globally. I believe that humans being humans we are trying to leverage the tools of politics and economics to game a favourable outcome for a problem that has no regard for either.

I prefer to think of this as an economy drive, forget about net zero, but is it possible to improve the economics of each family?

House insulation to Passivhaus standard…….YES……..who needs a heat pump?

Reduced electricity bills and money spent on power…….YES if the installation strategy is formulated properly

Energy security through wars/supply difficulties for every family…….YES, again if distributed generation with renewables instead of centralised generation is done……just look at Ukraine for the effect of the vulnerability of centralized power generation

Cheaper energy for travel…….YES

Reduced pollution around roads…….YES

If I reduce the £2,500 that I am currently spending on gas and electricity, more money to pass onto children/charities or better finances during retirement.

£2,500 per annum is £25,000 over 10 years, £50,000 over 20 years.

If it means the country borrowing less to pay for fuel imports, but it has to have the manufacturing industry in this country……or £50,000 would pay for a Tesla……but no thanks, I have other, better uses of my money.

House insulation/reducing gas and electric are the priorities. If I can take a chunk of expenditure out get a return on the investment, the benefit compounds year on year, but the installation strategy has to be right.

What is this current obsession with heat pumps all about? There are alternatives, and once you get the house insulated to a high standard, if you did get a heat pump, it could have a lower power requirement……..1kw not 5kw electric power input, or forget the huge capital cost of heat pump installation and just go for direct electric (off-peak) with a thermal store/woodchip heating, for what little you need, or you heat the person, not the house, after all a house is a massive heat battery.

You don’t need to depend on others who have more money than you to improve your own family’s finances.

I agree. On a standalone basis a house would need to have equipment installed to enable it to draw power from its EV in order to make use of the electricity it stores. Most do not have this. On a system-wide basis, EV penetration is still low and we are a long way from using V2G at scale

And has the Government factored in the extra demands on the grid that heat pumps would generate, or electric cars and all thisr new house too.

There seems to be a prevailing madness amongst Labour MPs , which is sleep walking us into a cold miserable future.

And if we stock up with cheap Chinese EVs, what will happen if Tawain gets invaded?

We should never have shut our remaining cosl powered station down, and in fact, kept quite a few running.

The question with coal power stations, is should we have converted them to run on wood chip/waste and not had quite so many gas CCGT?

Would woodchip be easier to stockpile than gas for getting through supply difficulties?

Gas went up due to shortages, and how much did the price of woodchip vary. Was the problem that we concentrated all fuel supplies to one, and thus became beholden to that one market. Diversity of fuel does help if you get shortages for specific fuels.

We could have switched to mainly running woodchip, and only used gas when demand was very high. How much would that have controlled the electricity prices. Wouldn’t have helped with gas central heating, but could have meant that electricity prices were more controlled.

Wood pellet biomass causes more emissions than coal, even from the stack, let alone from the supply chain. It is better to stick with coal.

Very good analysis. I just wish there was someone who could differentiate between the different renewable power sources in government and NESO and DESNZ, who could show their economic modelling more clearly. The key renewables that need backing-up, due to variability (wind and solar), that are available only some of the time, need to cost only as much as the gas (fuel only) used in CCGT if they are installed centrally, but not if it is being installed by the end-user, where different metrics apply, where a financial benefit is achieved if the price of the generated electricity is less than the cost of the electricity from the supplier.

With the increasing detriment of curtailment payments, the wind capacity now being installed really needs to have storage costs taken into account and technology installed concommitently to deal with the intermittency. You can see that on some days, doubling the wind power would help significantly with reducing the amount of methane burnt, but are they installing cost effective wind turbines, that are only displacing the cost of gas, or are we getting far more costs added due to inaccurate or incompetent financial modelling and financial contractual arrangements?

Renewable electricity does not have to cost more than gas/coal centralised electricity generation, but it has to be recognised that there are differences in the economics when installation is centralised or done by the end-user.

If we are paying curtailment payments, why isn’t that money being forced into investment into installation of storage technologies. I would put a legal obligation onto all companies that receive curtailment payments that the money has to be spent on installation of storage technology. If they are not, it is a stupid waste of money on companies that are not creating a power generation system that works for the UK population.

An end user that installs solar PV or wind never receives curtailment payments. Why should it be different for centralised power? It just makes the economics worse for the end-user for centralised power generation.

If enough end-users install solar PV with battery storage, minimising demand on centralised power generators, then there should be plenty of time over the summer for maintenance to be done on any CCGT generators or interconnectors.

Centralised gas fired CCGT capacity can be reduced if sufficient people install their own battery storage to be recharged over night, shifting demand from the day-time peak. Renewables do allow for fewer CCGT facilities/capacity, but only if the end-users have enough battery capacity installed. What is the difference in peak-trough power generation in winter during dunkelflaute? If you can shift 10GW of peak power demand from daytime to overnight………10GW less CCGT capacity is required!!!!

Perhaps a few blackouts might encourage this to happen?

This idea of displacing the cost of gas is pretty short-termist. For 2 decades, gas prices were low and stable. Then suddenly they shot up for a couple of years. The question is, if we analysed this century as a whole, are consumer better or worse off with renewables? The answer, which can be clearly seen from charts of wholesale vs retail price data, is worse off. Because intermittent renewables are expensive: higher balancing costs, higher network costs, need for backup generation, curtailment costs because grid investment failed to keep pace, and of course, subsidy costs

Surely it is the fundamental economic answer, where renewables, to be cost effective, where we need back-up facilities burning gas, or battery storage, economically to have no detrimental effect the renewables have to be priced at a generation price that represents the avoided fuel cost, i.e. the price of gas or coal if installed centrally or the price of electricity if added by the end-user. We can then afford to keep all the back-up of 50GW of whatever source, and the renewables running whenever they are available, of whatever source they are. This means all the CAPEX and OPEX costs for the renewables needs to be equal to the cost of the fuel going into the CCGT.

The renewables are costing more at the moment because of where they are being installed – centralised, 100s of miles from where they are needed – causing grid upgrades, and curtailment charges, and subsidies. This isn’t a problem with renewables, but the installation strategy that is being followed. I can believe that costs are being added into the system currently, but this is because there appears to be no overview and no regard to the economic way to do it.

When they were subsidising solar PV 15 years ago at the start, I refused to join the bandwagon because economically it was inappropriate for the country. But now solar PV installed by the end user is economically viable with no subsidies, so too is onshore wind, next to a factory or end user, farmer, etc.

Kathryn you are absolutely right about centralised renewables – the worst economics of renewable installation possible. Unfortunately we have politicians hell-bent on showing how much they have achieved, but missing the point that it’s the end-users that should be doing the installations when it is economic to do so. Perhaps that would remove the political aspects of the whole debate, and avoid the problem of centralised renewable power generators gaming the system for maximum profit, increasing the costs for the UK population and businesses.

It isn’t just about displacing the cost of gas. If you can get a system with end-user resilience built in at no extra cost, it’s win-win-win for the environment, economically and for resilience…….greater than the sum of its parts!!!!

Location isn’t the only challenged with renewables – the low energy density is also a problem since it means more wires are needed to connect them. You also have to deal with backup since the capex and opex costs of renewables do not represent their full costs to consumer – you need to include the cost to make them firm.

Exactly, which is why the renewables should be installed by the end-user where they’re needed and can get an economic benefit, and the centralised generation is then there as the back-up, burning gas, nuclear, or renewables with storage (only when economically feasible). Workers in factories have never moaned about wind turbines, chimneys etc, where their livelihoods depend on it. It’s only with the massive expansion of wind adjacent to residential areas and covering the landscape in turbines where there is the resistance.

Unfortunately, as far as I can see, the governments, of all shades, have been acting as a cartel/sole supplier for their own benefit, where profit from the generators is needed to bolster the tax receipts, building in costs into the system, because it means that they can get more tax out…….off-shore wind on Crown Property……nice little earner, but that income goes on the electricity bills. We are paying more for electricity so that the government can get more income to pay for the borrowing.

As the government makes it more expensive, the economic answer is to install end-user power generation and battery storage to counter the poor economics. We have to game the system for our own benefit, if that is what everyone else is doing………governments and centralised power generators, and yes, the end result is poorer economics for the poorer people………if a government isn’t capable of thinking of their best interests.

Interesting stuff, Kathryn.

It’s a concern of mine that the breakdown of generation at any moment refers to interconnector input to the grid as “Imports”. While this is, of course, perfectly accurate, it unfortunately obscures for the general public that most of the biomass generated relies on imported wood chips and a significant proportion of the gas used for electricity generation is imported by pipeline or as LNG.

It would be interesting to know the full extent of our day to day reliance on imported energy and what this tells us about energy security.

That can equally apply to gas as most of the gas we burn in our power stations is now imported. However, I am referencing direct elecricity imports, not wider energy imports, although your point is a good one.

Hi Kathryn

“That can equally apply to gas as most of the gas we burn in our power stations is now imported.”

Does it therefore follow that most of the gas we burn in our homes, offices, schools, warehouses factories etc is home produced? 😉

No, these days we are a net importer of gas

Security of supply depends on several different factors. Even domestic supply can be disrupted as many years with extended miners’ strikes will attest. The best security is attained by having competing sources and preferably politically reliable ones, delivering via methods that are secure. Norway has been reasonably reliable as a gas supplier by pipeline, although occasionally they suffer production problems, or choose to supply continental customers in place of the UK. It has been rather less reliable as an electricity supplier, since it found that having so many interconnectors to foreign countries tended to import the problems at the other end of the lines in the form of higher prices for Norwegians. They have found ways to reduce supply to the UK when their own position is threatened: they do not have limitless hydro generation or storage.

Interconnector supply depends on instantaneous availability. With gas there is storage flexibility: pipelines can be pressured more to store some gas, and there is some actual storage. LNG cargoes can be floated to act as extra storage, and vessels can be speeded up to help meet a cold weather demand spike. LNG is now a very international trade, with a good diversity of potential sources: we have had no difficulty replacing the limited quantities we were buying from Russia, even if in 2022 we were paying for LNG from Peru via the Panama canal in order to run extra CCGT to export to France. We’ve even had the odd cargo all the way from Australia. Potential oil supply is even more diverse, but internationally traded coal is now less so, but also has more limited markets which help make it lower cost. However, coal is clearly more diverse than wood chips, as well as being cheaper.

Wind and solar supply chains now increasingly depend on China for crucial elements: this is not diversification of supply, or making supply domestic. It is the reverse – it creates dependence.

Hello Kathryn,

Re: your “Assuming 6.5 GW of onshore wind (as set out in NESO’s Winter Outlook), and a total amount of installed offshore wind of 30.163 GW (which was the year-end capacity quoted in DUKES 2023”

I’ve just been referring to DUKES_6.2 “Capacity of, generation from renewable sources and shares of total generation” where by end 2023:

Wind installed capacity (MW) = 30,163 total comprising

15,418 MW Onshore, and

14,745 MW Offshore.

I’m not familiar with that 6.5 GW NESO number, looks low: and it looks like you’re using the total Wind capacity as your Offshore number.

Best regards.

Sorry, I should edit this to make it more clear – I was trying to extract transmission-connected wind rather then the onshore/offshore split since the contribution to demand is measured at the TS level. Just under half of the onshore wind is embedded therefore needs to be excluded from the TS data.

I prefer to include embedded generation, and add it back to demand: it gives a truer picture of the overall position. Likewise, I include pumped storage pumping as a “domestic” export: I would do likewise for batteries, but I have yet to find an information source on battery charging. At the moment they hide partly in embedded sources, and partly in the “Other” category at BMRS. I have suggested to Elexon that really we need to be able to see what our 4GW/5.7GWh of batteries are doing. Indeed, the battery industry constantly complains that they are not being dispatched by NESO when they could be.

I wanted to compare like with like. BMRS shows transmission-connected generation and demand. I’m not sure where total final demand figures can be found at a granularity that is interesting to analyse.

Kathryn as you know Putin (and Xi) just love the idea that we rely on undersea inter-connectors and undersea gas pipes for our power. And we only need to look back to WW2 to see why we need our farms to produce food. The last thing we should be doing is destroying the land for the benefit of unreliable diffuse energy technologies. Nuclear power and drilling for our own shale oil & gas are what we urgently need in this increasingly unstable and dangerous new world order.

PLUTO did keep the D-Day troops supplied with fuel even in war.

https://en.wikipedia.org/wiki/Operation_Pluto

IDAU:

Underwater drones did not exist in WW2. They do now.

Good to see you having time to produce another insightful article.

On wind installed capacity the NESO data set supporting this winters outlook report quotes onshore as 13.797GW offshore 16.165GW. The 6.5GW is a reference to embedded wind i believe.

Also looking at Energy Trends table 5.4 and using installed capacity from ET table 6.1 gives a LF of 35% for offshore over first 9mths of 2024. However, Ive separately looked at actual generation on some of the more recent sites on elexon and they are into the mid 40’s. So a modest improvement in LF ie a c5% may come through as the likes of DoggerBank are commissioned.

Anyhow in terms of derated capacity NESO assumption is wind on or offshore has a derated capacity of 14.4% vs 91% for CCGTs!

Interesting that prices get pulled up when countries export although given the inadequacies of our transmission system aren’t going to come close to being fixed before the end of the decade im not sure that will be a regular occurrence anytime soon.

On the i/c’s IFA1 suffered a fire late 21 that knocked out one leg and was part repaired in late 22 and fully restored in 23 so that presumably lowered its availability. That said im still weary of the political factor with the i/c’s becoming a risk.

Yes, I meant embedded wind and have corrected the blog to show this. My analysis was to show the load factors of transmission-connected wind.

The amount of ad hoc issues with interconnectors appears to be quite large – there is always a fire, ship’s anchor, grid issue or other fault impacting availability, so in the end it’s not worth correcting for them. Ad hoc interruptions appear to be part of the deal when relying on interconnectors

Probably one of the worst interconnectors, although not an international one, has been Western Link HVDC, which has had a spate of cable problems. That the Russian cable destroyer Yantar was recently caught nearby probably doesn’t inspire confidence either.

Great article. I’m in Australia so its interesting to see that the UK is also experiencing what you have called the “gaslighting” problem, wherein governments appear to be attempting to misrepresenting the true costs of the energy transition. This is not to say that the energy transition is not necessary. Indeed, it would seem that the transition is required so as to counter an existential threat. However, it is totally unacceptable and counter-productive to misrepresent the truth. Keep up the good work!

MS :

There is no “existential threat” from increasing levels of CO2 caused by the burning of hydrocarbon fuels. Not only have Happer & Wijngaarden shown that using the IPCC’s own radiative model that doubling CO2 causes just a temperature rise of 0.7 degrees C but recently Shula & Ott have shown both theoretically and experimentally that the radiative model itself is invalid and there is no greenhouse effect at the Earth’s surface because of thermalisation. There is no climate emergency as shown by the IPCC Working Group 1 (“The Science”) Table 12 in Chapter which shows no signal for climate change (storms, precipitation, droughts) other than some mild warming (0.14 degrees per decade according to UAH satellite data). Furthermore there is no CO2 explanation, let alone anthropogenic CO2 explanation as to how the Earth warmed to come out of the last ice age which ended just 11,000 year ago. Nor for previous warmer periods than today since this most recent ice age as shown, for example, by the discovery of 7000 year old tree stumps in BC/Canada as the glaciers retreat.

We’re just about getting to the same temperature peak as occurred in the medieval warm period, but when there was no CO2 increase previously, somehow it is assumed that this time it’s due to changes in CO2 levels. Dangerous assumptions are being made, but I worry about the CO2 levels only, which is getting higher than we have ever experienced as an animal/race, and that is a measurable change. Climate change doesn’t worry me one bit, it’s all within previous historical limits, even the 1.5 degrees or 2 degrees, it’s the actual CO2 level changing that worries me.

I cannot see how increasing CO2 levels from 3 molecules to 4 molecules per 10,000 to is going to make any difference to humans. With oxygen at 20% and CO2 at 0.04% (400 ppm) there is 500 times more oxygen than CO2. There’s even 23 times more argon than CO2. Although there have been found to be no symptoms in healthy young people at 20,000 ppm a limit of 4000 ppm has been fixed for general use. Over the last 500m years since the start of the Cambrian explosion CO2 has been up 10 times or more today’s value. BTW, the fact that Icelandic Norsemen colonised Greenland for several centuries in the Middle Ages prior to the Little Ice Age means that temperatures must been 5 degrees C higher than today. Also note that retreating glaciers in BC/Canada and Iceland are revealing tree stumps 7000 and 3000 years old respectively.

Have a look at

https://www.co2meter.com/en-uk/blogs/news/high-carbon-dioxide-co2-levels-indoors?srsltid=AfmBOorjJOjjS8inkM6vLNCNZlJ4BP1hLj2M-KHpisfPHmDmRvCNl43x

and

https://earth.org/data_visualization/a-brief-history-of-co2/

1,000 to 2,000 ppm – common complaints of drowsiness poor air quality.

2,000 to 5,000 ppm – headaches, fatigue, stagnant stuffiness, poor concentration, increased heart rate, nausea.

>5,000ppm – 8hr workplace exposure limit

We”ll be dead before it gets there, but it’ll kill off the unhealthy people, and require CO2 scrubbers for some people. It depends how much you want to spend on dealing with the impact on the less healthy, the overweight, the older people / new born babies in the population, with lung disease, COPD, poor circulation, blood diseases, premature birth etc etc……

If apes have only been around for the last 90m years, do you really want to look further back, then over the last 400m years it’s only been up to 2,000 ppm maximum.

It was last over 500ppm……20m years ago

How far do you want to push it?

It isn’t just about the ratio of O2:CO2 that’s important, the absolute level of CO2 is critical in physiology/biochemistry.

Yes we could have higher CO2 levels, but just watch the life-expectancy drop by a couple of decades, and we’ll be back to increased infant mortality rates. Yes we can survive as a race, but at what cost?

TS :

Thanks for your post and links. I don‘t think there is any problem at all up to 1500/2000 ppm. Packed halls and lecture theatres etc regularly reach 1000 ppm and greenhouses have CO2 added up to 1500 ppm to aid growth. As your first link says even 5000 ppm is considered safe for an 8 hour shift (link to OHSA).

Since CO2 is clearly of paramount importance to submariners I searched and found a Swedish submarine report on maximum CO2 levels which said:

“The main contaminant of submarine air is CO2. In ordinary buildings 1000 ppm is usually considered as a maximum concentration. This value is not based on health effects but on the rate of ventilation. In submarines, higher CO2 concentrations are permitted, usually 5000-7000 ppm.”

https://www.irbnet.de/daten/iconda/CIB7571.pdf

Anyway, at an increase of CO2 of 3ppm/year it will take 186 years to reach 1000ppm and 520 years to reach 2000ppm so I think there is no emergency.

The graph in your second link (Earth.org) is very interesting in that it shows that 9 times over the last 800,000 years CO2 has dropped to 180ppm only 30ppm above the minimum 150ppm level needed for plants, and hence all life on Earth, to survive. So life on the planet has come very close 9 times in the last 800,000 years to extinction. CO2 has been on a steady decline for the past 120m years. Patrick Moore, the Canadian co-founder of Greenpeace, believes that this is due to shelled marine animals using up the CO2 in the sea and then the atmosphere to make their shells (there are 100 million billion tonnes of carbonaceous rocks) and that if we do not start to return CO2 into the atmosphere we will eventually run out of plant food, CO2. There is a dearth of CO2 not an excess. There has been 4000ppm or more at times in the last 500m years. Interestingly looking at the last 500m years since the beginning of the Cambrian explosion there is no correlation between CO2 and temperature and no ice at the poles for longer than there has been ice.

BTW, the Antarctic Vostok ice core data shows CO2 following temperature for the last 450,000 years when both have been exceptionally low. Shula and Ott have shown, theoretically and experimentally, that the IPCC radiative model is invalid and that there is no greenhouse gas effect at all at the Earth’s surface because of the thermalisation of all the greenhouse gas molecules. Heat loss from the planet’s surface is through convection and latent heat. Only at the top of the atmosphere do the greenhouse gases, actually mainly water vapour, finally radiate to space to cool the planet.

Reply to John Brown, yes, it does look like it’s OK for many more decades, I don’t see it as an emergency either, it’s just that the rate of change of CO2 level has been increasing, with the economies of China and India, powering up, which have the potential to be far bigger than ours, with their greater populations……just imagine the rate of change of CO2 levels if those two nations had the energy inefficiencies of America!!

You’re certainly right on the problem of too little CO2, and you are right to point out that water vapour is a significant greenhouse gas. It might not be just the CO2 that we have to think about with methane and nitrogen oxides contributing. We were about to be starting on the change heading into another ice age, which would be very inconvenient this far north, so again I don’t see a few extra degrees as a problem.

We might have many concerns about immigration for now, but if we were to have another ice age, we would be the ones emigrating to sunny Africa.

It does make you wonder why so many people this far north complain about global warming, when it could reduce the impact of the next ice age. Does Greta Thunberg have a long-term view of anything?

“Ofgem has said that once GB becomes a net exporter of electricity, there will be a consumer dis-benefit and as a result it has rejected almost all of the proposed new interconnector projects with Continental Europe in Window 3 of the Cap and Floor regime. ”

They announced that they were minded to accept only one out of seven but then at IPA stage that’s gone up to three out of seven.

“It’s particularly interesting to look at the values for IFA and IFA2 which are virtually identical despite IFA being many decades older than its newer cousin, and being actually available a lot less. It’s reasonable to assume that the spare generation parameters for both are the same since they originate in the exact same place in France, so the difference in de-rating factors should reflect the difference in physical availability, but this does not appear to be the case.”

Yes and no. There is obviously logic in long term assuming that any physical asset will deteriorate, however slowly. However as you note, interconnector availability is mostly about ad-hoc failures such as anchor damage to cables or the IFA fire. There’s also a cyclical factor as there will be longer planned outages at certain points to do larger replacement works. In theory there would be a long term age-related reliability decrease due to component ageing but when I’ve modelled this before for clients, the effect ends up completely lost in the noise of over-running planned outages and cable strikes.

I haven’t looked at how the capacity market de-rating factors were actually calculated but I can tell right away that the longer I/Cs are slightly more de-rated which will reflect an availability estimate driven by cable failures calculated as a risk per unit length.

Thanks for a very informative article.

One small quibble wrt to load factors..”So if a 10 MW wind turbine produces electricity 35% of the time it would have a load factor of 35% and generate, on average, 3.5 MWh/h.”

While it might generate for 35% of the time, the output will depend on the wind speeds when it runs. It would only achieve an average of 3.5 MW if it ran at full output for the whole operating time.

Something that does not get much visibility is the best-ever wind output compared to the installed capacity. We have approx 30 GW yet the record to date is close to 22 GW: 73%. Presumably that reflects the fact that conditions will never be optimal across the whole fleet and some turbines will be out of service.

It probably reflects the fact that at higher levels of output there is maybe as much as 4GW being curtailed. Also, you have to be careful to ensure that the number you are looking at for generation includes embedded wind output, since the capacity number does.

Bear in mind that the generation figure you are looking might not include embedded wind, and also that at higher levels of output there is likely to be several GW of curtailment.

Small note: it’s Eleclink that runs parallel to IFA1 to Sellindge and both are normally supplied by the Gravelines nuclear complex near Dunkerque, although the lines submerge at the Coquelles/Les Mandarins HVDC converters just by the Chunnel through which Eleclink runs, avoiding trawler anchors. IFA2 runs from near Caen in Normandy to Chilling near Portsmouth.

It seems there is a general problem with interconnector trade across Europe, despite the supposed single market. Perverse flows (i.e. against the direction suggested by prices at each end) are apparently quite common. Some of this is simply because electricity actually flows in accordance with the laws of physics rather than the laws of commerce. Some of it is probably because markets for interconnector use are being manipulated. I have certainly seen this in the past, with capacity being bought up to prevent natural flows e.g. between Germany and the Netherlands. Some of it is probably that markets lack sufficient information to be able to trade to arbitrage away the price differentials.

With wind, the nature of contracts has a big part to play in the actual output. Older farms on ROCs will require conpensation for loss of subsidy if they are to curtail. That means that lower subsidy onshore curtails first, which the floating offshore wind farms on 3.5ROC/MWh never curtail. Likewise their is a heirarchy for CFD subsidised wind farms. The most costly get to carry on uncurtailed to extract their full subsidies. The next tranche are almost the same, save that if prices remain negative for 6 contiguous hours they lose all subsidy for the duration. Then they curtail voluntarily rather than pay to generate. Mostly, they manage to ensure that only 5 hours of contiguous negative price occur, so they retain their subsidy. All later wind farms, and those who have yet to exercise a CFD (and thus are on market prices) get no subsidy whenever day ahead market prices are negative. That puts them first in line to curtail, even ahead of onshore ROC funded wind farms. The result is that Seagreen, which has been fully operational since October 2023 but has not commenced its CFD has curtailed about 60% of its potential output: they do get paid for much of their curtailment, but the payments are lower.

Should we clap? I’d rather see wind farms getting over £200/MWh curtailed without compensation than one that only gets market price. We don’t pay diesel generators to curtail, even though they can charge handsomely when they are called on and have much higher cost that say CCGT.

If DESNZ has not understood this (and plainly they haven’t) then they are always going to be a long way wrong on wind economics, where LCOE is irrelevant as a metric of financial cost. Of course, they are busy being a long way wrong on the economics of hydrogen and H2P and CCUS and anything else they get involved with. I get the impression they don’t understand how the new Clean Inudustry Bonus for AR7 will work. At least, there is nothing setting out what they will pay out: the draft CFD terms say “whatever LCCC decide, but by the 4th anniversary of the Start Date”.

If the government’s strategy is for growth, they will see an expanding industry such as the renewable industry as an excellent first class example of the improving economics of the country. Unfortunately, if they are replacing the expenditure on fuel with even greater expenditure on grid upgrades, subsidies, curtailment etc, even more CAPEX and OPEX (far greater than the avoided cost of fuel) they will be making the power industry less economic for all businesses. Their holy grail of economic growth of the power industry will be making every other industry less competitive in an international market.

For the power industry to become more efficient, more competitive, like making central government more efficient, it needs to shrink, in terms of the power it is delivering, replaced by local, distributed generation. Does this mean that for local substations, from where local distribution would normally have occurred, have to become a grid stabilization centre, with battery storage and synchronous condensers, to stabilize the frequency and provide inertia, and to absorb excess power when there is local over-supply? If there isn’t local storage, then energy flows would have to be reversed on the national grid.

https://www.siemens-energy.com/global/en/home/press-releases/two-become-one-siemens-energy-combines-two-technologies-to-stab.html

Should we as a country really be investing, not in SMART meters (hackable system) and centralised power generation, but allowing end-users to efficiently add renewables in when it really is economic for us to do so.

If we get localised excess power, isn’t that exported power going to have to be priced at 0p per kwh to allow the investment in the localized surplus storage and grid stabilization?

The long-term economic model will have to change over time, and power trading will have to become far more localised (distributed) if there are going to be some local substations that have battery storage and power stored that cannot be distributed more widely than say a 10-20 mile radius. What area does each local substation cover? Can substations be reengineered to reverse the energy flows from local areas back onto the National Grid?

With distributed generation, the government should recognise that it should be ensuring that the production of wind turbines, solar panels, inverters and battery storage are critical industries, and they should be expanding at the expense of the total turnover of the centralized power industry. If they aren’t or haven’t been doing so, it wouldn’t be surprising that the economics of the whole country is getting worse.

If the surplus power supplies of end users is the cause of the need for the investment in grid stabilization, shouldn’t it value the exports from those sources as lower, and thus those exports pay for the necessary grid stabilization and grid upgrades……..who is currently paying for the grid upgrades?

This could be financially managed in a different way, where poor people are not put at a disadvantage, like they have the horrendous cost of the daily standing charge for what little electricity that they use.

Renewable power generation can be done economically, but are we achieving that currently?

It may be possible to support temporary export prices up to 20p/kwh, but as more end-user distributed power generation is added, those export prices are going to have to reduce significantly.

With the UK having to compete against countries like China, the UK is going to have to work a lot smarter than it is currently doing to find efficiency gains in other ways that are different to how things are being done in China. China may have the land (deserts) and cheap labour (some slave labour/prison labour) but the UK needs to find a technological strategy that doesn’t bake in much higher energy costs.

If the car parks of all factories and businesses get solar PV added to charge their worker’s cars and for factory power, there’s going to be plentiful surplus power at weekends, especially in the summer. We need to allow it to occur and work out the best way to utilize it.

The National Grid, government and DESNZ surely must be able to see these structural changes necessary in the electricity supply.

The standing charge should be added as a % tax to electricity and gas bills, not as a fixed amount for all users. The political choices that could benefit poor pensioners who have lost their WFA and low income families. The government could do something about this, but either they aren’t bothered, are being pressurised by other actors or haven’t got the wherewithal to sort out the system to make it equitable.

A fixed standing charge per user, where every household pays the same – is equivalent to electricity and gas poll taxes, at least Council Tax is banded – so too could the standing charges for gas and electricity as an alternative.

64p a day electric standing charge is £233.60 per annum.

25p a day gas standing charge is £91.25 per annum.

……..how much was the WFA?

If the government and local authorities own considerable areas of land and buildings, where solar PV can be installed on schools and council buildings, NHS hospitals, etc, etc, and if there is enough land, where helicopters are not landing at hospitals, where a wind turbine could be sited, why do we need to site so many wind turbines off-shore, miles from where they are needed?

The grid supplied electricity should become the defacto back-up electricity supply, where we shouldn’t be talking about having to get back-up for the wind or solar centralized power, the National Grid should be THE BACK-UP power supply, or the redistribution network of local surpluses.

The UK can supply all it’s power from solar PV for about 6 months of the year, if enough is installed, with batteries as well for overnight and cloudy periods, but a paradigm shift in perceptions of what the centralized power is there for needs to be made.

Electricity should become almost too cheap to meter in the summer, but more expensive in the winter, possibly more expensive than now, but overall electricity should be cheaper over the whole year. But the work and running the centralised power plants should become almost seasonal, from autumn through winter to spring, just like we put our central heating on in our homes for 6-8 months now. It is understanding this paradigm shift that can help to formulate the contracts and the types of power plants that are needed centrally. Nuclear that only runs for 6 months of the year, when maintenance and refuelling can be done over the summer.

If the government concentrated on installing solar PV on it’s buildings, reducing it’s electricity bills, that should lower the tax it requires to run itself, if that electricity is available cheaply at the weekends, the population will get a further economic benefit. Isn’t it time that the government started thinking more like a user, trying to reduce its electricity bills, rather than as a power company trying to expand its portfolio of centralized power plants?

Can the government co-locate it’s offices at some power plants, to get the benefit of wasted heat, to reduce its own heating bills?…….if we are paying for the electricity to be produced, shouldn’t the government be thinking where it is siting it’s offices to make the most of all that wasted heat from burning methane or hydrogen……if it happens………22GW of electricity gives 22GW of wasted heat in a CCGT plant……….ideal to co-locate government offices……..free building heating, just need a bit of plumbing, and stop the nonsense of government/local authority offices being buildings located elsewhere.

Has the government and all NHS hospitals and council offices/buildings installed LED lighting to reduce their electricity bills? When £200M is spent on a bat shelter for HS2, £100M is equivalent to 7.5 million LED strip lights, 22w, instead of the 50w flourescent lights. That would save 210MW of electricity demand……… 0.2GW, saving £50,000 per hour……..£0.5M per day saved if 10 hours per day usage…….£100M per annum saved. We know that there are some stupid priorities that governments and their quangoes start to set, or PFI, which increased the costs of running hospitals and schools. Is it that our governments have forgotten, or really don’t know how an economy works, or know how to run an efficient business?

Government by big gesture, rather than honing each bit of it’s workings for maximum efficiency?

If a government wants to act as a power company, at least they could organise it such that their offices are co-located where the power is generated and the waste heat is being produced. Isn’t this why we need CHP for all government/local authority buildings and NHS hospitals? To also be the back-up electricity supply for the local area?

I think I could shave a few billion off the government and local authority running costs, and now is the time to consider it as the electricity industry is being restructured.

What if, instead of CCGT plants wasting 50% of the energy, we have something like wartsila 10MW engines spread liberally around various buidings, government, local authority, factories, NHS sites, schools such that CCGT plants get scrapped, separate frequency response providers get scrapped, separate synchronous condensers get scrapped and we get the benefit of the NHS with lower electricity bills and heating bills, local government with lower electricity bills and heating bills, schools with lower electricity bills and heating bills, and factories with lower electricity bills and heating bills, because they’ll be the ones getting the benefit of CHP and getting paid for the electricity that they generate.

Do we need to rationalize the power industry and absorb it into other buildings and companies, such that whilst we have centralised renewables, the back-up power is distributed more widely, instead of about 30 CCGT plants of about 1GW output each, say 3,000 10MW generators, or could we do 30,000 1MW generators?……spread the wasted heat around more liberally.

There are many ways to achieve a few synergies in the power industry, and different ways to optimise and reduce running costs and waste. I think in a few years time the power industry will be ripe for a bit of condensing of it’s own to remove the inefficiencies that are building up in the system with the piecemeal addition of different technologies.

With focus on local generation and local networks we are in danger of forgetting the main reason for all this upheaval and investment. The sole purpose is to reduce to near zero CO2 emissions.

The narrative presented to the public focuses on cheap, clean and UK produced electricity. Most people are attracted by the low cost lure but some also by the home grown element. Home grown to the extent of spiralling down to local community or domestic production. A sort of “The Good Life” self sufficiency model. If honest most people are not that interested in the confusing concept of clean or net zero.

It is difficult enough technically and politically to reduce CO2 emissions without also introducing another philosophical self sufficiency element.

Looking at the historical development of electricity we have been here before. At its inception it was entirely local. Power stations and electricity networks were entirely independent, owned and run by local corporations or wealthy individuals. There were no common standard. Voltage and frequency varied some AC some DC. Economic forces drove their integration and standardisation not a political desire for centralisation. Resilience was increased, manpower per MW reduced and expensive back up shared. Fuel burn (the main cost and in todays context CO2 emissions) could be optimised across the whole nation.

We must not waste time and money going back through this iteration again.

Other than some minor transmission issues, the issues with intermittent renewables are identical whether driving local networks or an integrated national system. The local argument is irrelevant.

The NESO “Clean Power 2030” report, without NESO recognising it although they are puzzled, actually demonstrates that their recommended solution is not a pathway to net zero.