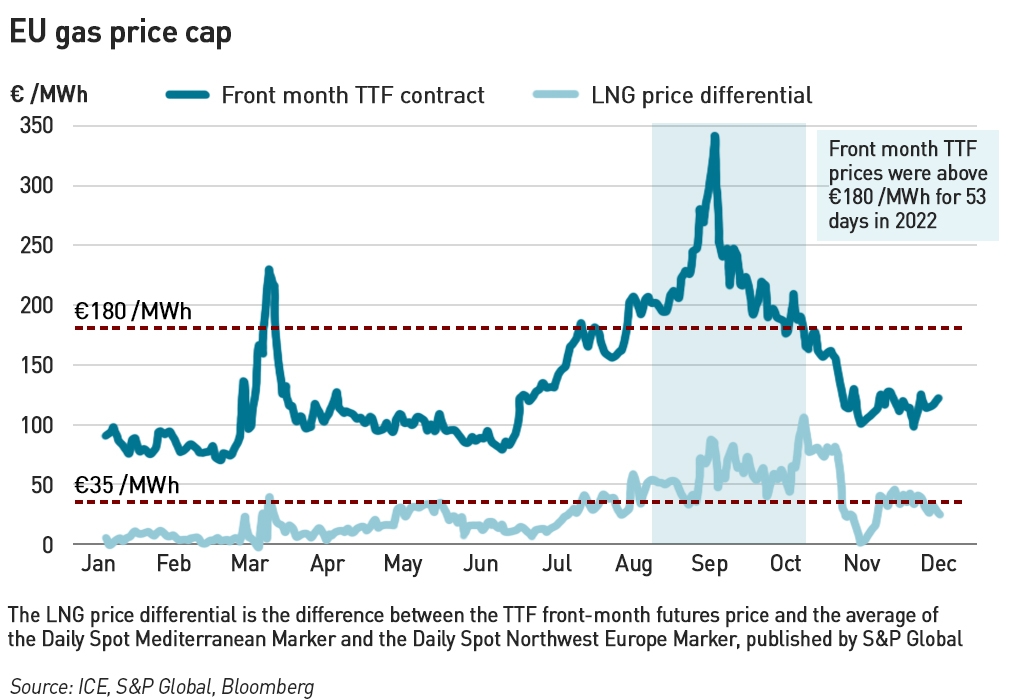

This week the EU finally acted on gas prices by agreeing a cap. Under the “market correction mechanism” which is due to come into force on 15 February 2023 and last for one year, gas contracts traded on European exchanges could see their prices capped if the TTF front month contract exceeds €180 /MWh, and is €35 /MWh above an LNG reference price, for three business days.

Once triggered, the cap would limit month-ahead, three-month and one-year TTF futures contracts to €180 /MWh for at least 20 working days. There will also be a price floor where, even if the reference price for LNG is below €145 /MWh, the price cannot fall below this plus €35 /MWh. The price limits would be automatically de-activated either by the dynamic bidding limit dropping below €180 /MWh for three consecutive working days or if an energy emergency is declared.

The cap has met with a mixed response…

The cap has been set well below the €275 /MWh trigger price originally proposed by the European Commission, and was agreed by a qualified majority of EU member states with Hungary opposing the move while Austria and the Netherlands abstained. The agreement has to be formally adopted to become binding, which is expected in the coming days.

“Despite progress the last couple of weeks, the market correction mechanism remains potentially unsafe…I remain worried about major disruptions on the European energy market, about the financial implications and, most of all, I am worried about European security of supply,”

– Rob Jetten, Minister for Climate and Energy Policy, Government of the Netherlands

The Dutch energy minister also voiced doubts as to whether the measure will succeed in lowering gas prices for consumers while also guaranteeing security of gas supplies.

Although Germany had long opposed many of the proposals for gas caps that have been made throughout the year, it was able to support this scheme after the inclusion of safeguards to reduce the negative impact on competition for international LNG cargoes. Part of the cap mechanism relates to global LNG prices in the hope that it will not inhibit the ability of European buyers to compete with their Asian counterparts.

Several countries welcomed the news with Polish Prime Minister Mateusz Morawiecki saying the agreement “spells the end of Russia and Gazprom’s ability to manipulate the market”. Some would like to go further, suggesting the measure does not go far enough and should be considered temporary since the level of €180 /MWh is still unaffordable.

…and is leading to uncertainty in the gas markets

There is some uncertainty around the application of the cap, since the European Commission may suspend its activation if a forthcoming report by the European Securities Markets Authority (“ESMA”) and the Agency for Co-operation of Energy Regulators (“ACER”) as well as analysis by the European Central Bank indicate the risks outweigh the benefits. Earlier in December, the ECB warned about the risks associated with the cap proposals at the time.

“The ECB acknowledges that mechanisms aimed at moderating extreme price levels and volatility in wholesale gas markets may, in principle, alleviate a number of risks to financial stability, including the risks exposed during periods of elevated and volatile gas prices in 2022…However, the ECB considers that the current design of the proposed market correction mechanism may, in some circumstances, jeopardise financial stability in the euro area,”

– European Central Bank

Even if the cap is activated, it could be suspended by the Commission if it is believed to be increasing gas demand or reducing LNG imports – the Iberian cap on the price of gas for electricity generation saw gas demand increase. Other reasons for suspension include an adverse impact on market stability, a reduction in the volume of gas traded at the TTF, or a reduction in volumes of gas being delivered to Europe. These safeguards make it difficult to understand what the impact of the cap might be – while they are designed to re-assure sceptical countries such as Germany, the mere existence of the cap may negatively impact Europe’s ability to secure LNG cargoes since it signals that the EU is willing to interfere with market prices and normal market arrangements.

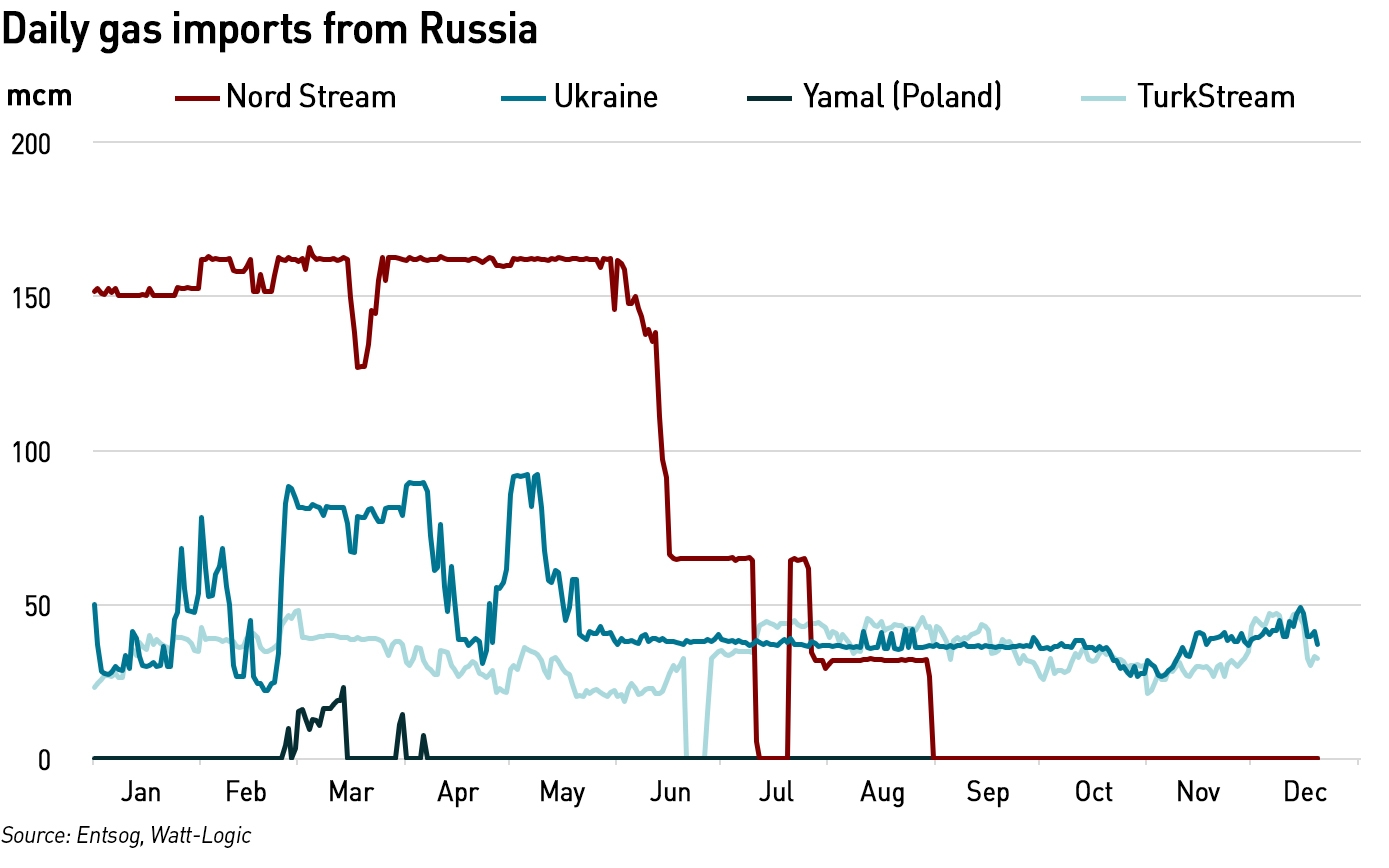

Any measure which reduces the ability of European buyers to secure LNG cargoes could be devastating for the bloc since it is far from clear where the gas will come from to fill storage facilities next summer ahead of next winter. This year, although imports from Russia were greatly reduced, it was primarily gas arriving through Nord Stream which allowed the EU to more or less fill its storage facilities by the start of this winter. However, with Nord Stream physically out of use, and the route through Poland (Yamal) closed due to sanctions imposed by Russia on the Polish pipeline operator, Russian gas has only been flowing through Ukraine, albeit at reduced volumes, and through Turk Stream.

In addition to reduced imports from Russia, competition for LNG is likely to be higher next year as China exits its zero covid policy and resumes a higher level of economic activity. There is still uncertainty around this – covid deaths are growing rapidly in the country, so the recent lifting of restrictions might yet be reversed should a public outcry at the levels of fatalities arise.

There may also be an impact on pipeline gas markets. Although Norway’s Equinor, the largest single gas supplier to Europe, has said the cap is unlikely to affect its exports, Algerian energy minister Mohamed Arkab said that capping prices “destabilises the market” and that “open, transparent, unrestricted and non-discriminatory gas markets are more than a necessity”. Algeria is Europe’s third largest gas supplier. Russia has described the measure as “a violation of the market pricing process” and said it would “thoroughly weigh the pros and cons” while preparing its response to the EU move.

The application of the cap to exchange traded gas contracts might also result in a migration of liquidity from recognised exchanges back to the OTC (over-the-counter) bilateral markets. A reduction in liquidity would cause the prices of exchange-traded contracts to become more volatile, increasing the risk that the cap would be breached. Analysts at Eurasia Group suggested that gas traders would liquidate short positions and stop selling futures if they thought the cap could be activated imminently, for fear of the resulting losses.

The Association of European Energy Exchanges has warned that a cap might have “potentially irrevocable negative effects” on the functioning of European energy markets and that if traders move their activities off-exchange this will lower liquidity (and income) for the exchanges and may also impact spot trading which is outside the scope of the cap.

“We have consistently voiced our concerns about the destabilising impact a TTF price cap will have on the market . . . We are reviewing the details of the announced market correction mechanism, its technical feasibility, the impact on financial stability, and whether ICE can continue to operate fair and orderly markets for TTF from the Netherlands as per our European regulatory obligations,”

– ICE

Intercontinental Exchange Inc, which operates Europe’s largest gas exchange ICE and which hosts TTF on its Amsterdam exchange, has said it will assess the technical feasibility of the cap and its likely impact on financial stability, as well as whether the market can operate in a “fair and orderly” way under a cap. It had previously said it could move TTF trading outside the EU (eg to London) if the EU imposed a price cap – presumably this is still an option.

.

While the introduction of a cap is big news, there are doubts as to its implementation given the Commission has reserved the right to cancel it at any time. But even so, it might dent the willingness of gas sellers to engage with EU buyers, encourage traders to move activities away from recognised exchanges and encourage those exchanges to defend their interests by moving trading outside the EU. And even if the cap did come into force, a limit on gas prices might encourage increased gas use and restrict the natural demand destruction that comes with higher prices.

Market interventions are always tricky. They should be handled with caution if unintended consequences are to be avoided. The outcomes for the European gas markets could well be other than those policymakers intend…

The first effect would surely be to shift trading volume to ICE NBP, perhaps accompanied by some inter market spread CFD or basis physical trade (I.e. physical supply on the Continent priced at a differential to NBP). Experience of Limit up/down trading on e.g. NYMEX shows that back months get some of the pressure that would normally apply to the prompt, distorting the forward curve, but mainly trading volume craters as alternative markets take over.

Concentrating liquidity back to the UK market will lead to distortions here of course. Nimble traders who understand the influences will make super profits.

Happy Christmas to you and the readership.

In my opinion, you would liquidate your physical shorts (as the paper length cease to protect you above 180)