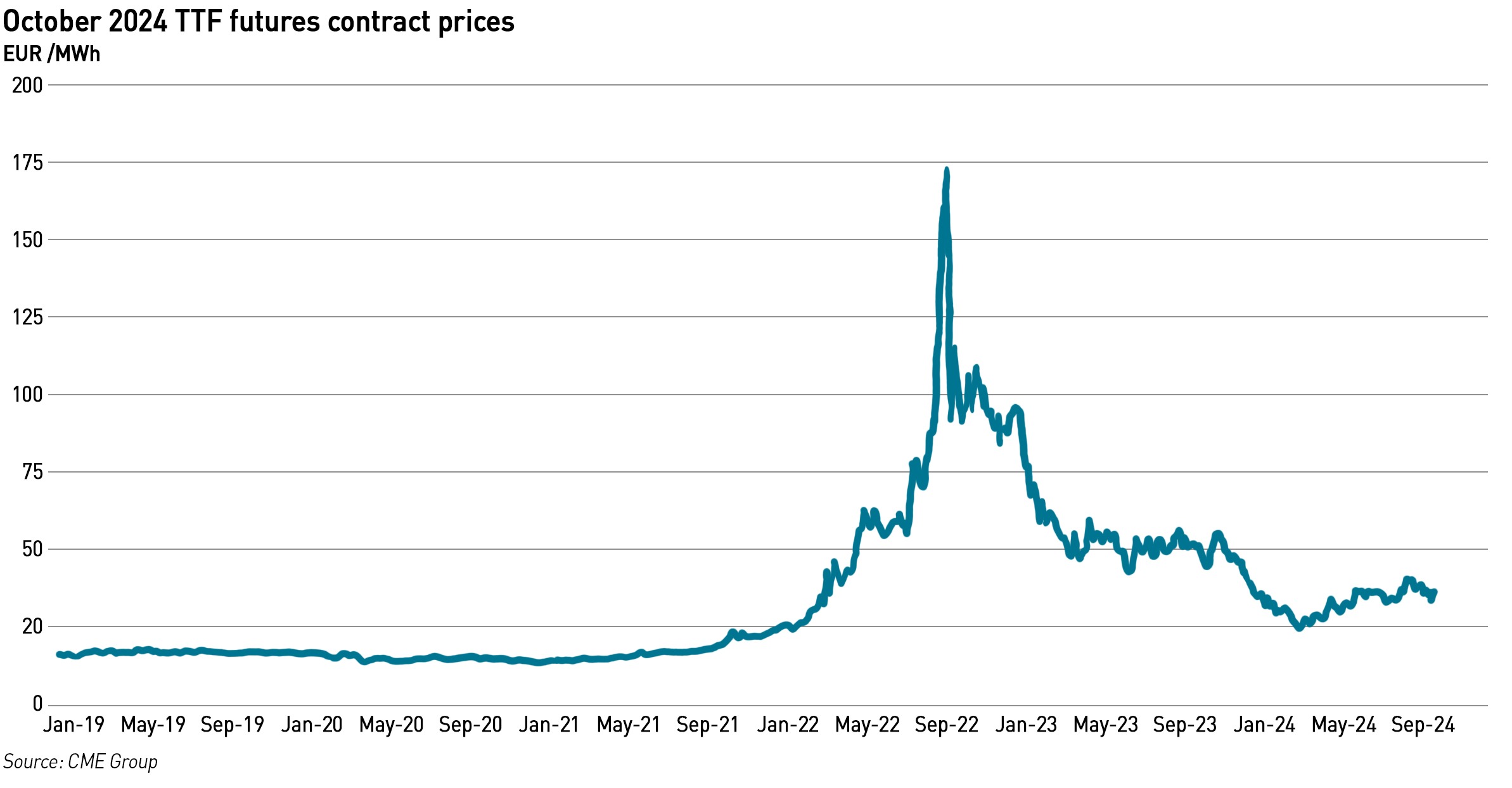

European gas prices have fallen significantly from the highs of 2022 but have yet to return to pre-crisis levels. In fact, they have become more volatile, less predictable, and arguably, less reflective of market fundamentals. In this post I will look at some of the recent factors affecting the market, and consider what we might expect next.

.

Since hitting 2-year lows back in February, gas prices have risen, slowly until the last couple of weeks at which point the increase accelerated beyond what might be expected from market fundamentals, although some of those gains have since been given up. European gas inventories are at the top end of what has been historically the case for the time of year, and the Continent has increased its access to LNG through the rapid commissioning of floating LNG terminals, to offset the reduction in pipeline gas from Russia. Gas demand also continues to drop. So what is driving the recent price increases?

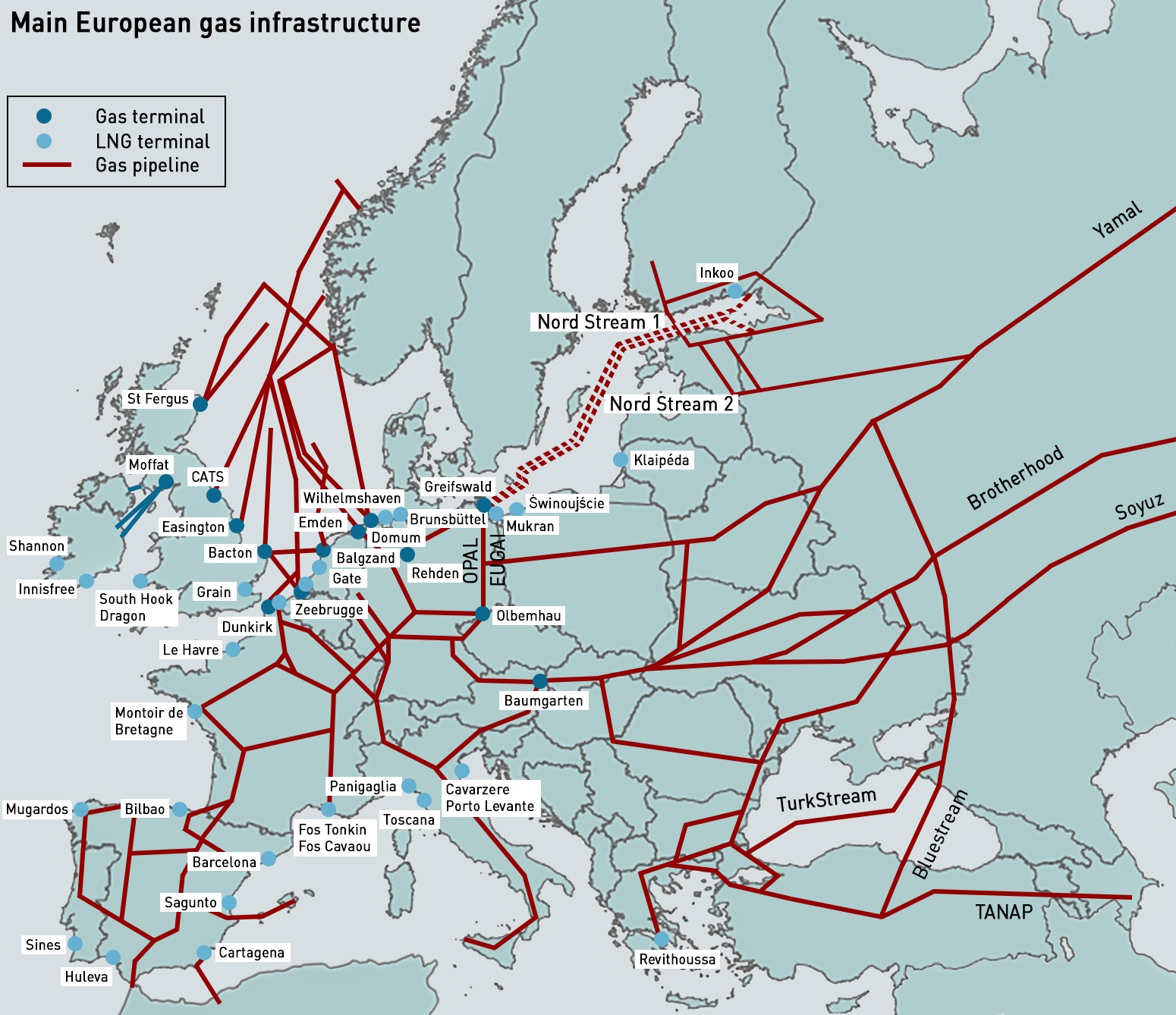

There are essentially two theories, which could both be true. From a fundamentals perspective, the military incursion by Ukrainian forces into Russia in the Kursk region is creating additional uncertainty since this province contains infrastructure important to the flow of gas through Ukraine which has been consistently under threat since the start of the war (see below). Westward flows through the Yamal pipeline through Poland have long since ended, and with the demise of the Nord Stream pipelines, Ukraine and Turk Stream remain the only transit routes for Russian pipeline gas to reach Europe. Flows through Ukraine are below historic levels but have not actually stopped. The risk that these flows would stop is rising, but the market should have largely priced this in already.

The other source of geopolitical risk relates to the escalation of conflict in the Middle East. Israel’s military response to the 7 October terrorist attacks continues, and the risk of contagion involving Iran and Lebanon is growing. The Middle East is both an important source or hydrocarbons and an important transit route, so any spread of military actions in the region tends to cause energy markets to react with higher prices. However, oil markets are not following the same pattern as gas markets so it’s difficult to attribute too much of the movement in European gas prices to conflict risks in the Middle East.

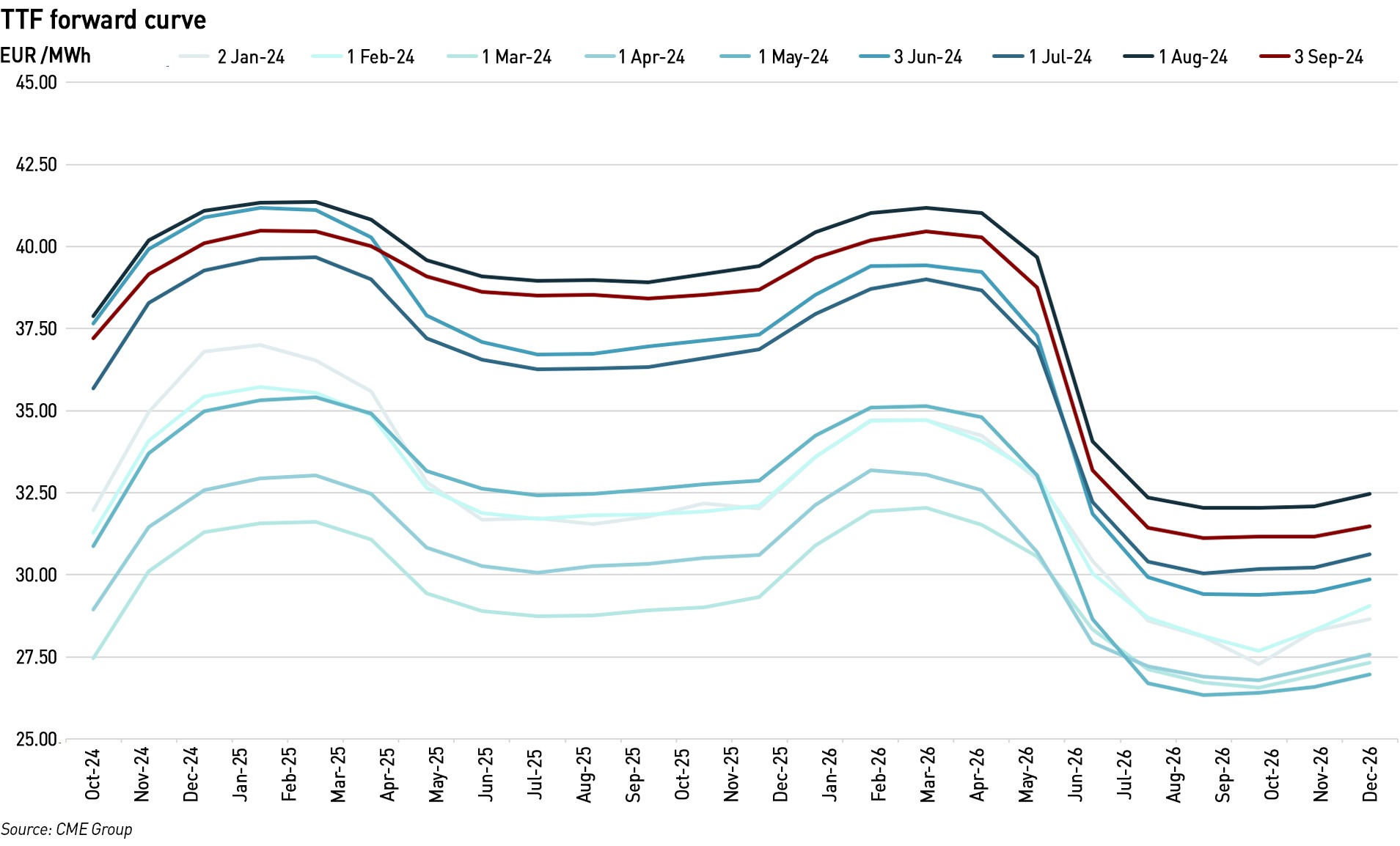

Whichever, if any, of these theories is correct, the TTF forward curve has moved significantly over the course of this year. The snapshot from the beginning of January is in the middle of the range for the year, with snapshots in H1 being generally lower than in H2 so far, however at the beginning of September it began to head down again. The other striking feature of these snapshots is that in the past few months the curve has reflected a larger relative reduction in prices from Summer-26 than was expected earlier in the year.

Threatened disruption to residual Russian pipeline gas flows

The Urengoy-Pomary-Uzhgorod (Brotherhood) pipeline brings gas from western Siberia via Sudzha in Russia’s Kursk region, and then through Ukraine to Slovakia. In Slovakia, the pipeline divides with one branch going to the Czech Republic, and the other to Austria. The main buyers of the gas from this pipeline are Hungary, Slovakia and Austria. About 14.65 bcm of gas was supplied via Sudzha in 2023, or about half of Russian natural gas exports to Europe. Overall, EU gas consumption fell to 295 bcm in 2023.

Sudzha, is now the focus of intense battles between Ukrainian and Russian forces, following Ukraine’s surprise incursion into Russian territory. Gazprom’s Sudzha gas metering point is located a few miles out of the town, closer to Russian-Ukrainian border.

Before the invasion of Ukraine in 2022, Russia used to supply just under half of EU gas demand, but much of this has been replaced by LNG (some of which is also from Russia). About half of gas which Russia now exports to Europe transits through Ukraine (the rest through Turk Stream). These flows have been at risk consistently since the start of the war, both directly through the risk of physical damage and through issues relating to the contractual arrangements.

In 2022, the Ukrainian state gas company, Naftogaz, and Gas Transmission System Operator of Ukraine (“GTSOU”) declared force majeure on gas flows entering the Sokhranivka entry point in the occupied territories of eastern Ukraine amid concerns Russian occupants were stealing transit gas. In light of the fact that Sokhranivka was under the control of the Russian armed forces, and therefore not under the control of the Ukrainian gas authorities, Naftogaz offered transit through the Sudzha entry point at no additional cost. Not only did Gazprom refuse this exchange, it also reduced the volumes it was already delivering at Sudzha.

Naftogaz considered that it had provided the required transit services, and that Gazprom had refused to make use of them, and so could not rely on force majeure to escape its payment obligation. It therefore initiated arbitration proceedings against Gazprom stating that “funds were not paid by Gazprom, neither on time nor in full” for gas transit. Gazprom said that Naftogaz had no “appropriate reasons” to reject its obligations to transit gas via the Sokhranivka entry point. This dispute remains unresolved, with arbitration rulings expected later this year. Meanwhile, Naftogaz has taken additional legal action, including efforts to enforce a US$ 5 billion arbitration award relating to the seizure of its assets in Crimea flowing annexation in 2014.

The other challenge is simple contract expiry. The existing transit agreement was signed in December 2019, with a five-year term for the transit of 45 bcm of Russian in 2020 and 40 bcm per year for 2021-2024. This agreement expires in 2024, and Ukraine has said will neither extend it nor sign a new deal. Russia is apparently ready to continue to supply gas to Europe via Ukraine after this contract expires.

Asian LNG demand has been growing…

Beyond geopolitical risks, the supply and demand balance is shifting. According to the International Gas Union Global Gas Report 2024 Edition gas demand in Asia saw continued growth in 2023, rising 32 bcm (3.3%) from 2022 to reach 995 bcm. At the continent-level, this was mainly driven by industrial, residential, and commercial growth outpacing a 3 bcm (-1.1%) decline in power sector demand for gas in the year. At the country-level, China and India were the main contributors to the region’s growth. China’s gas demand increased by 25 bcm (6.9%) in 2023 y-o-y, while India’s gas consumption grew by 7 bcm (12.7%).

China’s gas demand rebounded in 2023, after being suppressed by high global gas prices in 2022. 9 bcm of the increase was driven by a recovery in industrial activity, mirroring the country’s economic recovery, and fuel switching from coal to gas as global prices fell during the year. Cold weather at the end of last year helped to drive demand growth in the residential and commercial sectors to meet heating needs.

Indian gas demand growth of 16.3% or 6 bcm in 2023 was driven by industry. The fertiliser sector in particular was a key gas consumer with increasing urea production leading to a 20% reduction in imports, and therefore higher demand for gas as a feedstock. There was also growth in gas demand for transport of 1 bcm, with the number of compressed natural gas vehicles, including three-wheelers and cars, growing by 53% to 180,000 between 2022 and 2023. There was another increase of 1 bcm for the residential and commercial sectors.

In 2024, Asian gas demand is expected to continue to grow, with a forecast increase of around 43 bcm (4.3%) from 2023. China is expected to be the main source of this growth, at around 34 bcm (8.6%) by the end of 2024, with India following with an increase of around 5 bcm (7.1%).

Increased gas demand in Asia drives increased imports of LNG to the region, which are forecast to reach a total of 25.03 MT (million metric tonnes) in August 2024, according to Kpler, an increase from 23.86 MT in July, and higher than the 23.32 MT in August last year. Much of the increase has been driven by China, the world’s largest LNG buyer, which imported an estimated 6.94 MT in August, the highest monthly total since January and up from 5.91 MT in July. While China has seen higher electricity demand due to hot weather, very little LNG is used in the Chinese power sector. The growing use of LNG for trucking is boosting LNG demand in China.

Japan, the second-largest LNG importer in the world, bought 5.83 MT of LNG in August, up from 5.45 MT in July, with demand driven by a heatwave and higher air-conditioning demand. The situation is similar in South Korea, the third largest importer, which also saw higher volumes in August, to an estimated 3.86 MT, up from 3.16 MT in July.

According to energy intelligence firm Vortexa, India’s monthly LNG imports in May, June and July 2024 reached a four year record, averaging 2.57 MT. India is the fourth largest LNG importer, and has been experiencing a record heatwave with electricity demand spiking to meet cooling needs. While the bulk of this additional demand was met by hydropower, the share of gas-fired power generation doubled from level in the first quarter. Capacity utilisation and electricity generation by gas-based power plants was the second highest on record during April-June 2024. Power demand in India has been rising at around 7-9% on an annual basis, driven by expanding industrial and commercial activity as well as growing household consumption.

However, India is more price sensitive than the north Asian markets, and saw a reduction in LNG imports in August, with volumes expected to be 2.09 MT, the lowest since April and down 18% from July’s 2.56 MT, likely as a result of rising prices. Thailand also saw lower LNG imports in August with market sources observing that utilities in both countries have failed to award spot tenders in recent weeks.

It’s also likely that demand in North Asia may return to its normal seasonal pattern, which typically sees a peak in summer, usually August, followed by declining imports until October before arrivals kick up again to meet winter demand.

…while European LNG demand has been falling…

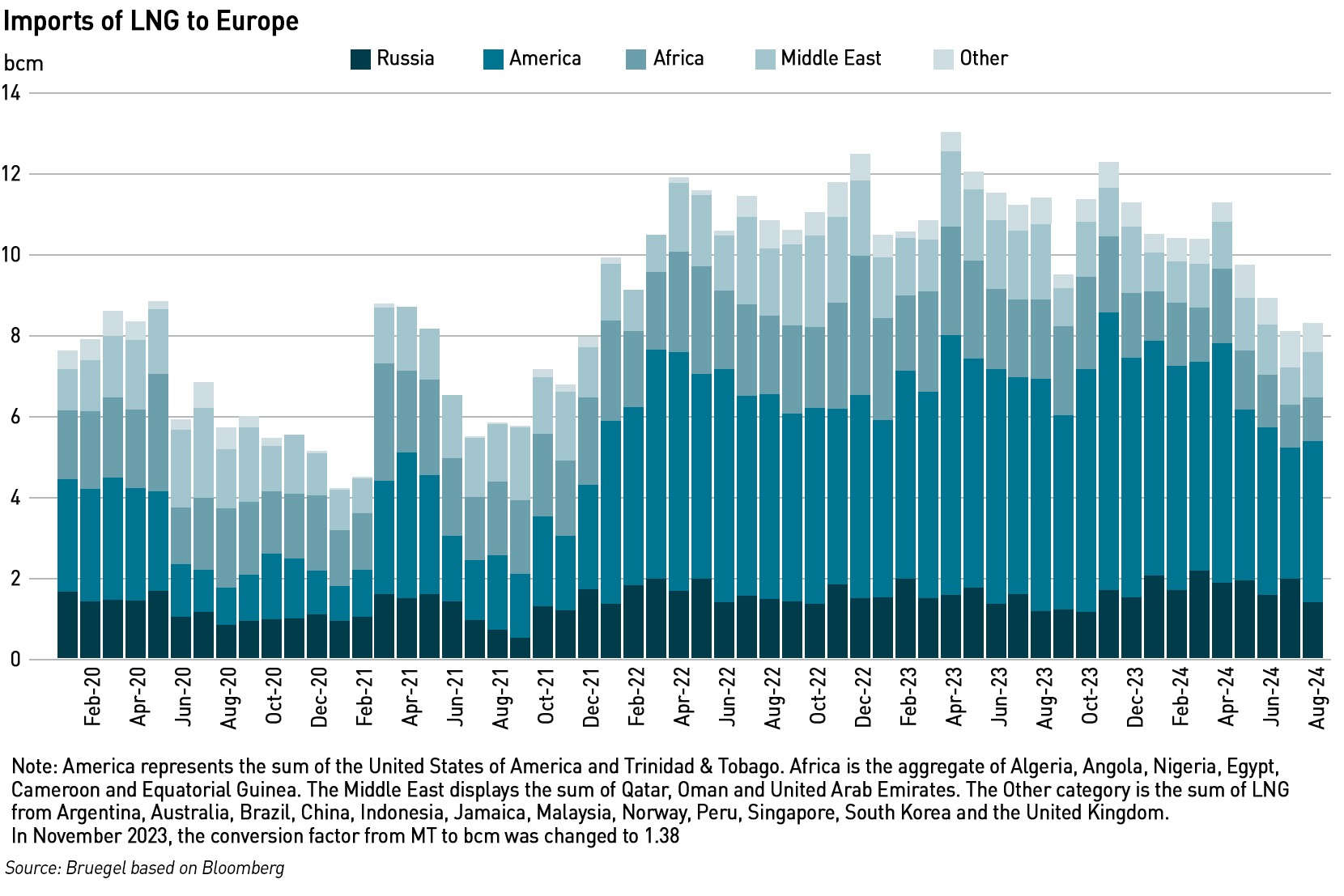

In contrast to the increase in Asian LNG demand, European LNG imports continue to be weak, with August imports on track to reach 6.25 MT tons in August, the lowest monthly total in three years, and down from 6.52 MT in July and 8.58 MT in August last year. LNG demand is falling as natural gas inventories reached 90% full 10 weeks ahead of the target date.

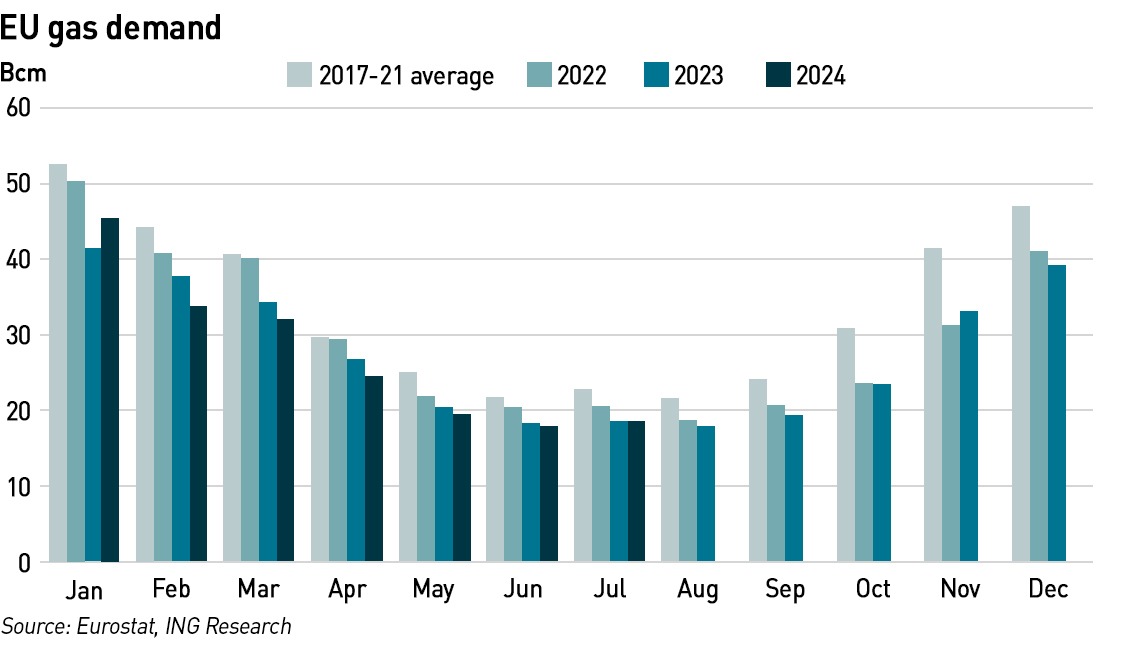

Investment bank ING reports that EU gas demand was down just over 3% year-on-year for the first seven months of 2024. The EU reports that it exceeded its voluntary target of reducing gas demand by 15% as established by the emergency Regulation on EU Coordinated Gas Demand Reduction Measures. Overall, EU reduced gas demand by 18% from August 2022 to May 2024 with 138 bcm of gas saved.

Gas demand in the power sector was reduced as a result of negative spark spreads, and higher renewable and nuclear generation. This, combined with lower heating demand over winter 2023/24 more than offset the recovery in industrial demand. ING expects overall EU gas demand will be largely flat for 2024 compared with 2023, growing less than 1%, meaning gas demand is still around 19% below 2021 levels.

Over half of Europe’s gas demand reduction was in the power sector, alongside a combined decline of 9 bcm (-5.0%) in the residential and commercial sectors, driven by a milder winter, and a 5 bcm (-4.0%) fall in industrial gas demand. Europe is expected to surpass 50% of power generation from renewables for the first time this year.

Industrial demand in Europe declined by 25 bcm (-17.8%) from 2021 to 2023. While some of this demand was due to temporary curbs and fuel-switching – estimated by Rystad Energy to be around 5% or 6 bcm, in 2024, but as much as two-thirds of the decline in industrial gas demand could be structural, from permanent efficiency optimisation, relocation of production outside Europe, and a structural shift in European gas markets. Some manufacturers have invested in alternative technologies, such as BASF which built the world’s largest heat pump at its Ludwigshafen site in June 2022, switching away from direct use of gas.

Increased gas price volatility attracts hedge funds

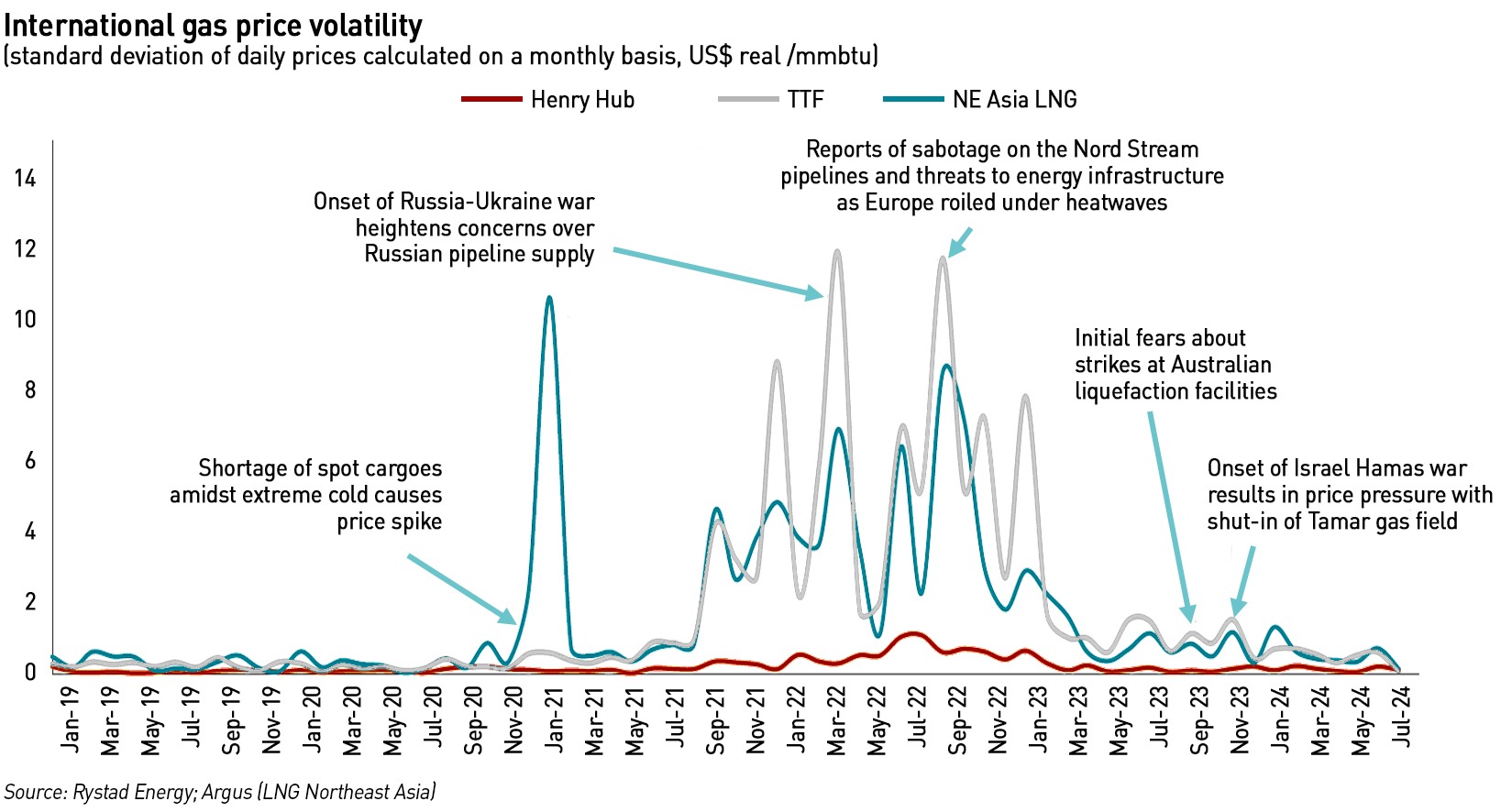

While global gas markets have calmed down from record volatility in 2022, they remain fragile as energy security concerns persist. Volatility levels remain above the pre-pandemic era – according to analysis by Rystad Energy quoted by the IGU, TTF price volatility was 1.7x higher in the first half of 2024 compared with the whole of 2019 levels. Although gas prices have fallen, as no major new supply additions are expected to come online in 2024, there is a risk that any disruption to existing supplies will strongly impact prices.

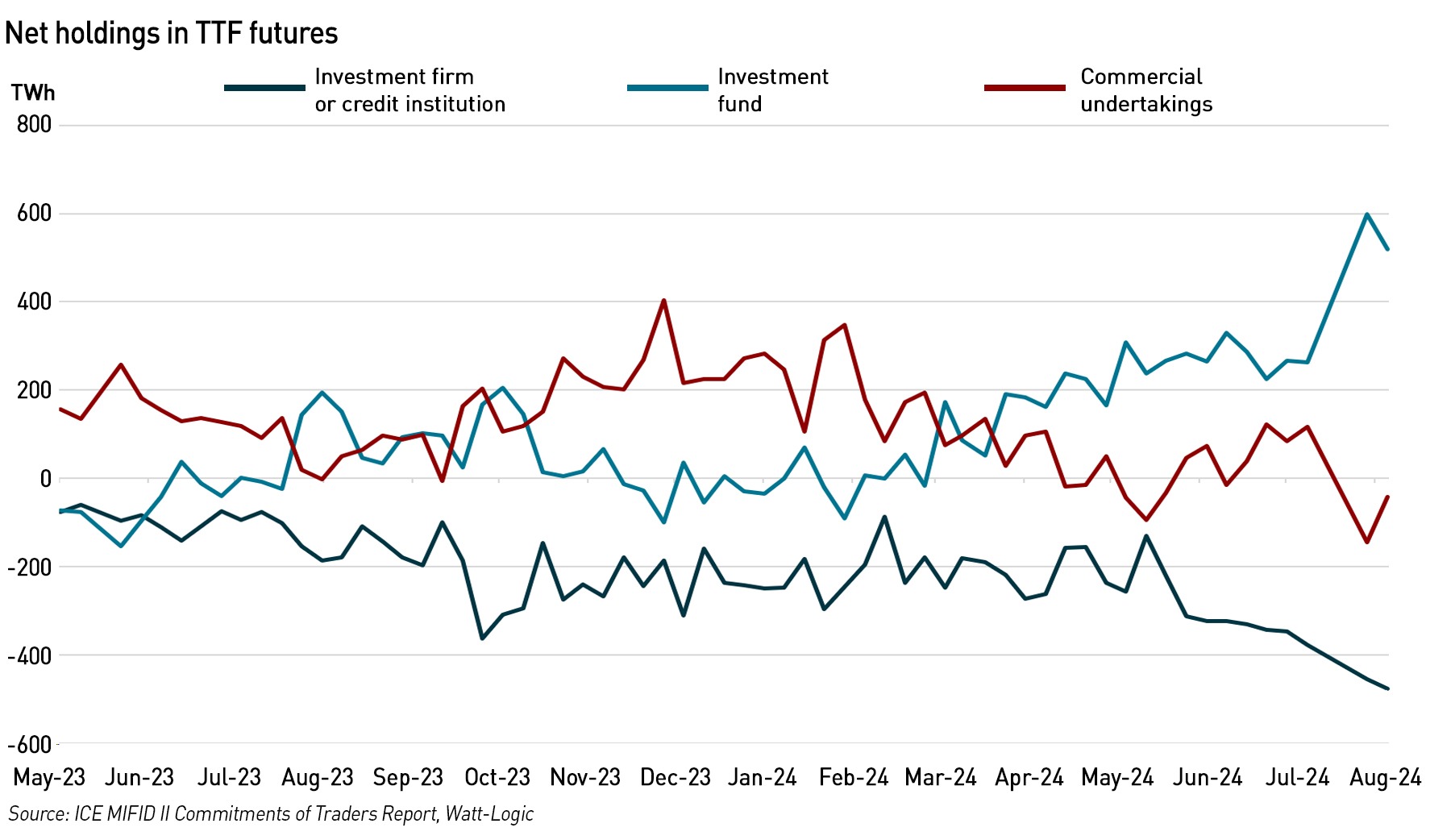

There are also non-fundamental factors in play. When prices dipped in February, many financial investors, particularly hedge funds, believed prices should fall and opened short positions. However over the subsequent months, prices rose fairly consistently and have not since approached to February lows. In early August it seems that these institutions began to close out their short positions (by buying gas) and began to build long positions (by buying more gas). This has inflated prices, beyond what might be justified by the fundamentals.

European gas has become increasingly interesting for investors since the Russian invasion of Ukraine because the loss of stable pipeline gas flows from Russia has made the markets fundamentally more volatile. Volatility provides opportunities for returns, attracting new interest from financial players who had not previously seen European gas as an interesting asset class. This opens the markets to price variations driven by investor actions rather than simply the fundamentals (and opens the door to technical price analysis which is not something I generally have much time for, but traders are people and people are not always rational when making trading decisions, despite that being one of the founding assumptions of almost all valuation models!)

Global supply and demand balance

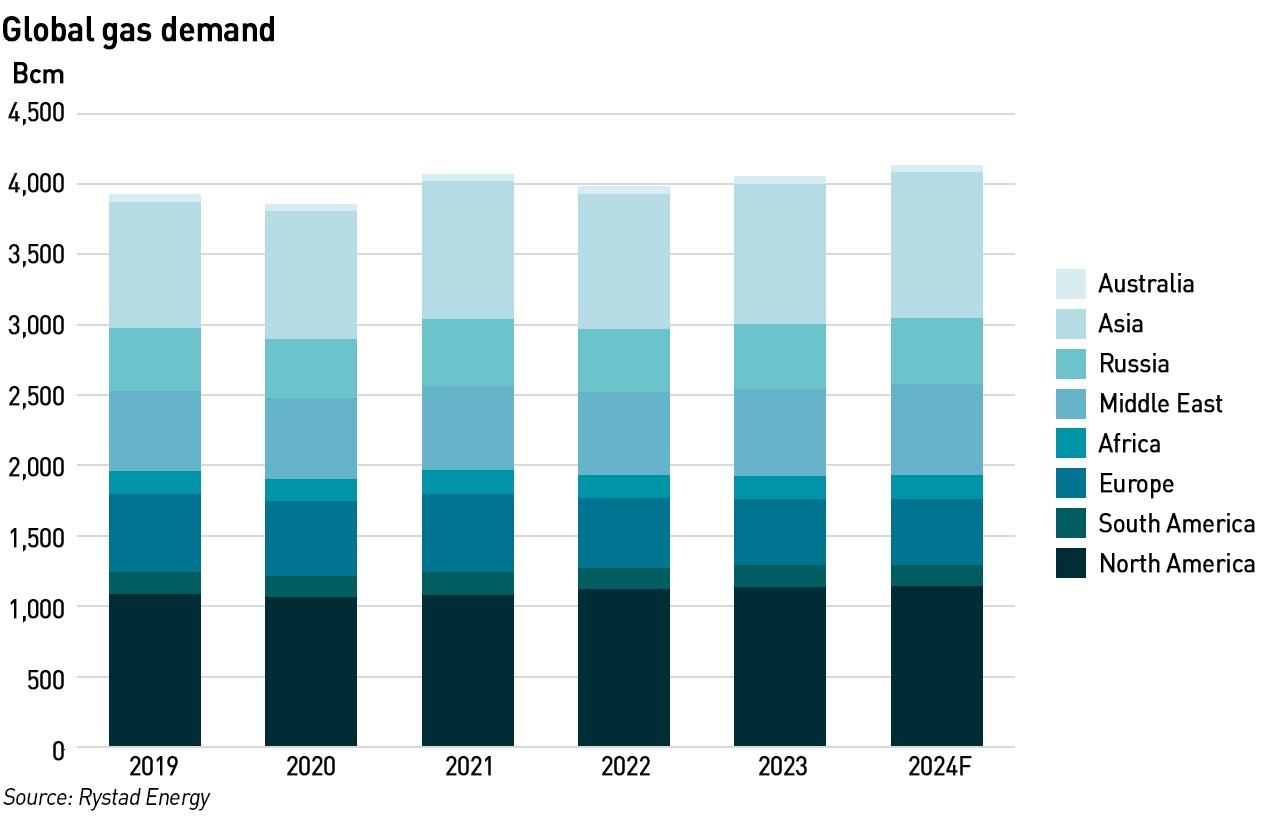

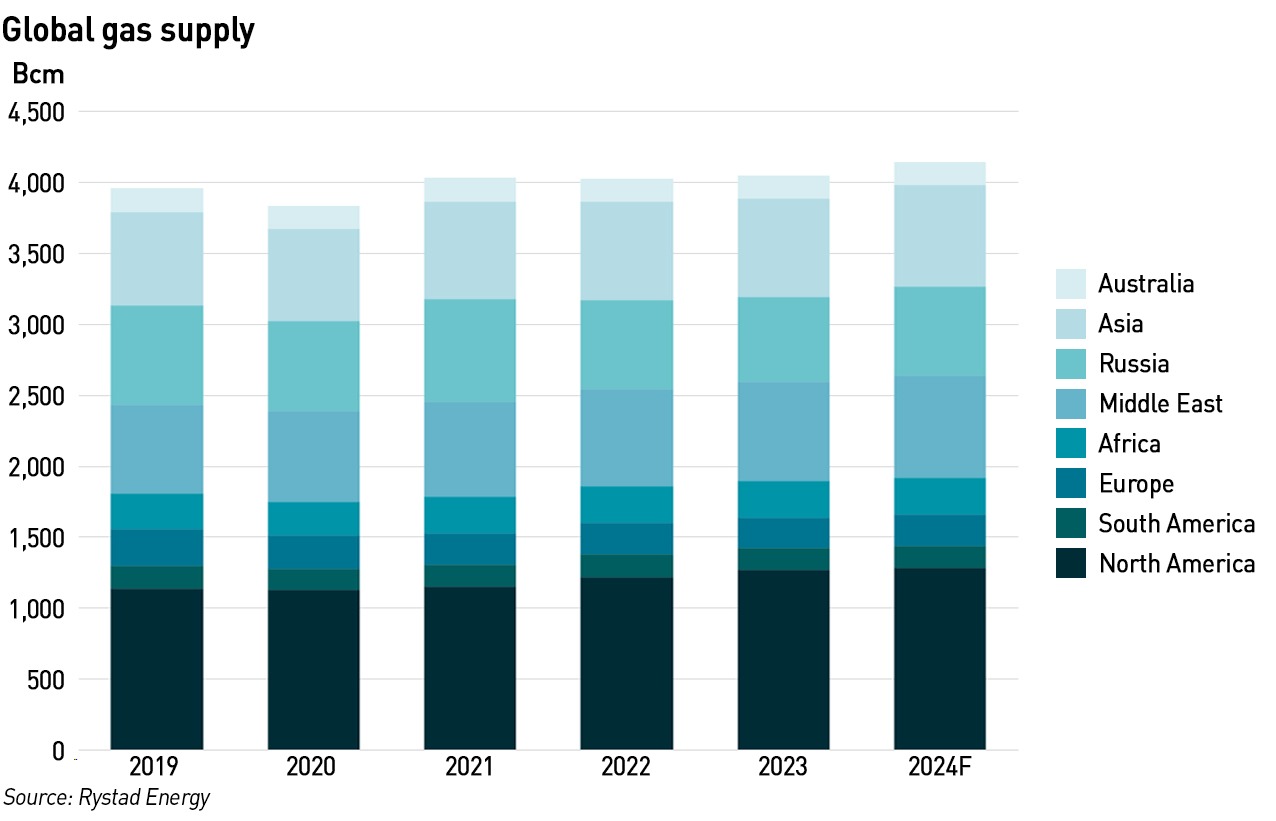

According to the International Gas Union Global Gas Report 2024 Edition, global gas demand increased by 59 bcm (1.5%) in 2023, and is expected to grow by a further 87 bcm (2.1%) in 2024. In 2023, demand increased in several regions, with Asia up by 32 bcm (3.3%), the Middle East by 28 bcm (4.7%), and North America by 14 bcm (1.2%), outpacing a fall in consumption in Europe by 31 Bcm (-6.3%) and in Australia by 2 Bcm (-3.7%). Demand growth in 2024 is expected to be driven by Asia, up by around 43 bcm (4.3%), the Middle East, up by around 29 bcm (4.7%), and North America, up by roughly 8 bcm (0.7%).

Global gas production has also risen, increasing by 19 bcm (0.5%) in 2023 relative to 2022 and is forecast to increase by around 96 bcm (2.4%) in 2024. Growth last year was largely due to higher production in North America, which increased by 52 bcm (4.3%), and the Middle East which increased 16 bcm (1.9%). Asian production grew by 3 bcm (0.8%). Collectively these increases offset a supply decline in Europe of 18 bcm (-7.8%).

Supply growth in 2024 is expected to be driven by the Middle East with an increase of around 26 bcm (3.7%), Asia with around 17 bcm (2.4%) and North America with around 12 bcm (1.0%). Modest growth is also expected from South America with additional production of roughly 4 bcm (2.6%) forecast, Europe with around 2 bcm (0.9%), and Australia and with around 1 bcm each. North American LNG export potential jumped by 37 Bcm, as shale gas production boomed in the Permian, Haynesville and Eagle Ford areas, outpacing consumption, although this trend is expected to soften in 2024.

Global regas capacity has seen a rapid expansion since 2022, growing with a Compound Annual Growth Rate of 7.7% from 2022-2024F, on top of the 4.8% CAGR in 2019-2021. The largest European additions were in Germany (25 bcm), and the Netherlands (12 bcm).

According to the IGU, current levels of investment in natural gas supply are not going to be enough to meet the demand expectations to 2030 – production capacity and infrastructure investment are not keeping pace with demand growth the developing world and new consumption trends and continued growth in energy use in the developed world. While the market is expecting a major expansion of LNG capacity to materialise in the next few years – the International Energy Agency says that global LNG supply will expand by 25% (or 130 bcm /year) between 2022 and 2026, with 70% of the supply increase concentrated in 2025-26.

There is some debate within the market about whether forward prices are genuinely reflective of fundamentals. Some analysts believe the markets are not correctly pricing in the addition of new capacity, and that the TTF forward curve is over-priced. This may be a result of the market expecting some new capacity to be delayed, strong Asian demand supporting prices, or the lack of liquidity in the curve more than one year ahead. In fact all three of these could be true.

However, others believe that demand for gas will be stronger than many forecasts suggest, and indeed when global energy consumption forecasts are analysed, there appears to be a bias in favour of under-stating demand in order to demonstrate net zero compliance. While energy demand may be forced down in developed markets as a result of aggressive policy drives towards net zero, it seems unlikely that developing world energy demand growth will be constrained to any great extent.

For example, the IGU believes that if the more conservative expectations of gas demand growth between 2021-2024F continue to 2030, and no new producing capacity is added, there will be a supply gap of around 927 bcm in 2030, increasing to around 1300 bcm in more ambitious forecasts. It also points out that global energy demand has consistently out-stripped energy transition scenario assumptions in both the developed and developing worlds with gas demand out-turn being higher than expected.

Even in Europe, overall energy demand has increased over the past five years, despite policy incentives to increase efficiency and the ongoing industrial decline driven by higher prices, although this trend may accelerate as evidenced by the recent announcement by Volkswagen that it is considering closing factories in Germany. For a national champion such as Volkswagen to consider closing operations in Germany is highly significant.

North American energy demand has exceeded 2019 levels, driven by the transport sector and new demand from data centres and AI. Asia has seen robust energy demand growth, particularly in India and China. African energy demand has grown faster than most regions, led by urban development, albeit still from low levels, but growth still remains below the rate needed to achieve full energy access for its people. In both South America and Africa, equitable access to electricity remains a significant challenge.

In addition to demand growth pressures, production challenges are emerging as mature fields are come of age. New conventional gas fields take 5-8 years to develop, meaning that it could be difficult to maintain supply and demand balances in the 5-10 year timeframe.

Russia’s hidden LNG exports

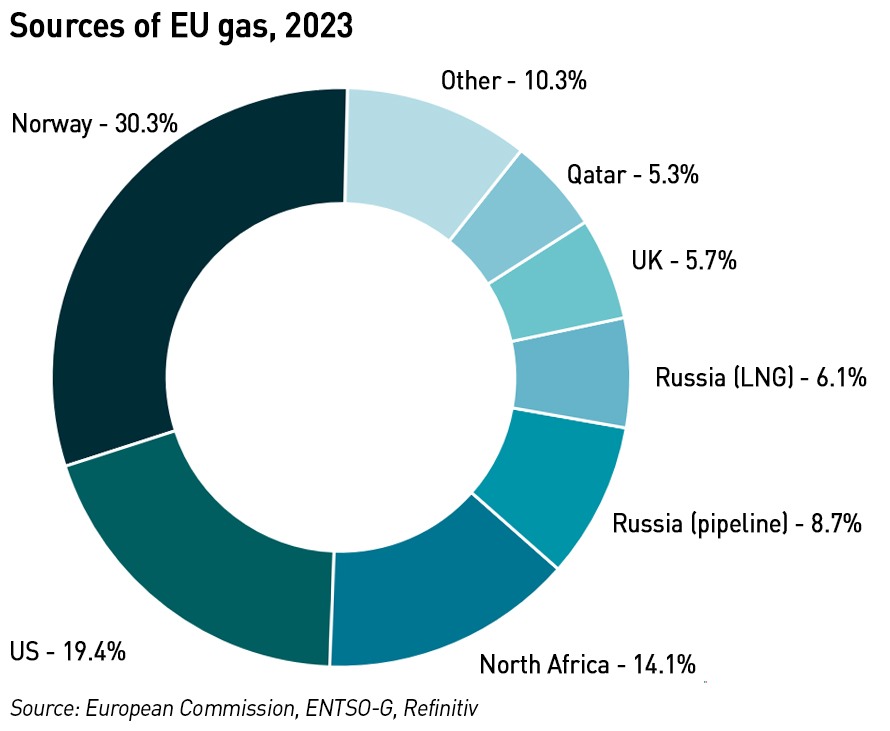

No discussion of global gas markets in the wake of the Ukraine war would be complete without a discussion of the role of Russian LNG. While Europe has almost entirely stopped buying pipeline gas directly from Russia (although piped gas is effectively being “laundered” through Azerbaijan and Turkey), its imports of Russian LNG have not fallen to the same extent, According to Kpler, the EU’s LNG imports from Russia increased by 37.7% between 2021 and 2023. The European Commission has called for a voluntary phaseout of all Russian fuel imports, including LNG, by 2027. The largest importers of Russian LNG in 2023 were Belgium (32%), Spain (32%) and France (23%).

According to the EU, 6.1% of gas sold to the EU in 2023 was Russian LNG and 8.7% was Russian pipeline gas (ie just under 15% of the total). The recently published State of the EU Energy Union Report says that Russian gas (pipeline & LNG) dropped from a 45% share of overall EU gas imports in 2021 to only 18% in the first half of 2024 (from 150.2 to 25.4 bcm) which implies an increase since FY 2023.

Until February 2022, most of the gas Russia supplied to Europe was delivered through the Nord Stream pipeline to Germany, however since the invasion of Ukraine, most Russian gas deliveries to Europe arrive in the very western-most parts of the Continent, and then travels inland, reversing the previous east-west flows. The 3.6 MT of Russian LNG imported by France in 2023 represented 41% of its net exports, and when adding volumes transiting from Iberia, all the gas piped from France to Belgium and Germany and almost half the gas sent to Switzerland and Italy could be attributed to Russian LNG.

Belgium imported some 4.8 MT of Russian LNG – almost double the volume it piped to the Netherlands, and about 0.7 MT came in through Dutch terminals. (Those calculations exclude transhipments, when LNG in loaded onto a different ship in an EU port before sailing on.) Germany – which no longer directly imports Russian gas – is the ultimate destination – in 2023, Germany imported 48.6% of its gas via pipeline from Belgium, France and the Netherlands, so as much as 13.7% of gas in the German grid could be of Russian origin, although it’s impossible to say how much is used within the transit countries.

The influence of Russian LNG is also seen in southern Europe. For example, Greece reduced its imports of Russian pipeline gas by 20% after 2022, but since Gazprom LNG deliveries more than quadrupled, the share of Russian gas in Greece reached 47% in 2023, up from 36% in 2022.

It remains to be seen how committed the EU will be to further reducing reliance on Russian gas, given the potential impact on prices and industrial activity within the bloc.

What next for European gas?

There’s an old reading saying that you “buy the rumour and sell the fact”. Last week TTF prices suddenly dropped in response to rumours that Ukraine had agreed a transit deal for Azerbaijani gas to take effect once its Russian transit contract expires. But these drops were largely reversed as the rumours were denied by “well-placed sources”, and it seems that no such deal exists, although one may well be under negotiation.

The European gas market looks well supplied by any measure. Storage levels are close to full and demand continues to fall. But the new reliance on LNG rather than pipeline gas means that the market is much more vulnerable to supply disruptions, and so any new, real or otherwise, which could impact supplies, tends to generate a price response. This increased volatility has attracted increased hedge fund attention, adding another source of price variation as their market expectations increasingly impact prices.

We also see the market react to real news which does not have an impact on the fundamentals – for example the August 2021 closure of Nord Stream caused September NBP prices to spike despite the closure having next to no impact on the GB gas balance for that month.

The single biggest factor that will drive a genuine change to gas fundamentals as winter approaches is an early cold snap. Any cold weather through the winter will see prices rise as storage withdrawals accelerate. The next most important factor would be news affecting gas supplies from Norway, the US or North Africa, or news relating to supply disruptions affecting the Asian market which could see LNG cargoes diverted away from Europe. Demand spikes in Asia would have a similar effect.

Absent these factors, and in particular if the winter is mild (again), prices might look higher than the fundamentals justify, in which case there could be a correction. Lower prices could themselves trigger fundamental changes for example higher industrial demand, but prices may have to fall more than the fundamentals might justify for that to happen. In reality, European energy prices were already getting un-competitive before 2021, and the subsequent crisis has triggered many industrial consumers to think hard about whether they should re-locate production elsewhere. It would probably require more significant price reductions to derail those plans at this stage, particularly with further environmental legislation expected which could further reduce competitiveness. Rules about buying Russian gas could be further tightened which would also be bullish for prices.

My sense is that current prices are on the high side given the actual market balance, but I don’t see a market correction heading into the winter. Any correction would be more likely after a mild winter, while a cold winter would adjust the balance, and then it would depend on whether the resulting price adjustment was reasonable or not. But in any case, I would not expect prices to fall to pre-crisis levels in the next year, so the wider questions about energy affordability both for households and businesses will persist.

After many years of low volatility, which makes it hard to make money if you are speculating on price changes, there was the sudden rapid increase in price, which attracted traders, not investors. Short-term significant, and consistent price trends up and down really helps to attract the (speculative) traders, who have no longer term view, and are just looking for price action. It will be interesting to see if the volatility subsides or becomes consistent with a larger eco-system of speculative (non-investor) traders. It is the cost for normal product purchasers in any market that the speculative traders do not care if the price represents “good value” and their actions may well push the price above what it is “worth” or “expected market value” making it relatively expensive, but again can also push it down to make it cheaper for some periods too. It’s just one of the costs (effects) of a capitalist system that allows speculation, where there are considerable volumes traded, but there is no intention to actually have the commodity delivered.

Of course, if you want to protect yourself from price swings, you can trade in gas yourself, and make money from those price swings. If you make enough money, it then matters little what the price actually is when you have to pay your gas bill. This was what the utility companies were supposed to be doing, but went bust because they were either under capitalised, and therefore didn’t, or had no ability or interest to do so. Perhaps we all have to do it ourselves to protect ourselves from the a) the lack of ability of others to do so, and b) the effect of market price changes.

Theres a fair amount of new LNG liquification plant coming on line over next few years albeit that needs the feedgas in the first place but FID wouldn’t have been taken without certainty of supply. So LNG looks to be well provided as does the marine vessels to ship it around the world so its seems plausible with continuing gas substitution by renewables happening globally there could be plenty of gas in the market so prices will fall back..

A very useful summary of many of the physical underpinnings of gas market fundamentals, with a lot more detail than Timera’s brief summaries (which none the less do have an interesting focus)

https://timera-energy.com/blog/gas-market-winter-outlook-5-key-risks/

https://timera-energy.com/blog/key-gas-market-sd-drivers-for-2025/

I think they and you are in broad agreement. One factor neither of you mention is the sharp reduction in LNG movements via Suez in the light of ongoing Houthi action. Until that is dispelled, the extra voyage time and cost in going Cape laden and ballast (even picking up a Bonny or other African Cargo) will help to isolate the Asian and Atlantic markets, especially once the Arctic route closes for the winter in a few weeks. It also means that there is no quick fix with cargoes diverted from Qatar to come to Europe via Suez in the event of a cold snap. The Spark30s freight rates were low in September, but they could easily take a very big jump if ships have to go around Africa to fetch incremental supply.

https://timera-energy.com/blog/atlantic-lng-charter-rates-drop-to-seasonal-low-in-september/

What happens to Russian LNG over the winter also matters: the Chinese have been taking some via the Cape in their own ships (Megrez, Merak, Dubhe, Phecda). It’s no surprise they have also been stocking up from the more direct Arctic route on Russian vessels.

Pointing up the interest of financial funds in the market is a useful insight. To some extent this is a flight of money from stock and bond markets, and to some extent it is just portfolio hedging to improve Sharpe ratios. We saw it in huge volume in 2008, when despite the atrocious economic fundamentals, oil was pushed almost to $150/bbl. It’s the old saga of the markets can stay irrational longer than you can stay solvent, especially when there is a weight of big money to throw around. Incidentally, I wouldn’t cast too many aspersions on trading on technicals: they are a very important input to algorithmic trading, and so become self-reinforcing. A reading of something like Murphy (still the tech analyst bible) has some good explanations of why trading patterns show up (and they are often capable of ambiguous interpretation to add to the fun, so you get to be retrospectively right). There’s still a lot less open interest and therefore hedging than was common before the energy crisis. That probably makes it easier for Wall St to push prices around..

The outcome of the US election will probably be important, since Trump is likely to change the landscape by being tougher on Iran while trying to secure a denouement of the Ukraine/Russia war. He would also lift the blocks on new LNG liquefaction plant start ups. Generally tending to push prices lower sooner. Harris is likely to result in them keeping high and volatile by restricting LNG supply and keeping wars hot.